As the Intelligent Automation (IA) sector experiences rapid growth, the Private Equity (PE) landscape is ripe for investment, offering a unique blend of technological innovation and market potential. With significant advancements in Automation technologies and a shift towards more favorable investment conditions, Private Equity (PE) firms are well-positioned to capitalize on this emerging opportunity. This strategic moment presents an unparalleled chance for PE to drive value creation and redefine industry standards.

Specifically, Intelligent Automation, a convergence of Automation technologies comprising Robotic Process Automation (RPA), Low Code/No Code, Intelligent Document Processing (IDP), Intelligent Virtual Assistance (IVA), Process Mining, and Intelligent Content Generation, serves as a transformative force in contemporary industries. This innovative methodology incorporates Advanced Intelligence through Computer Vision, Natural Language Processing (NLP), and Generative AI.

Shift from VC to PE in Automation Investments

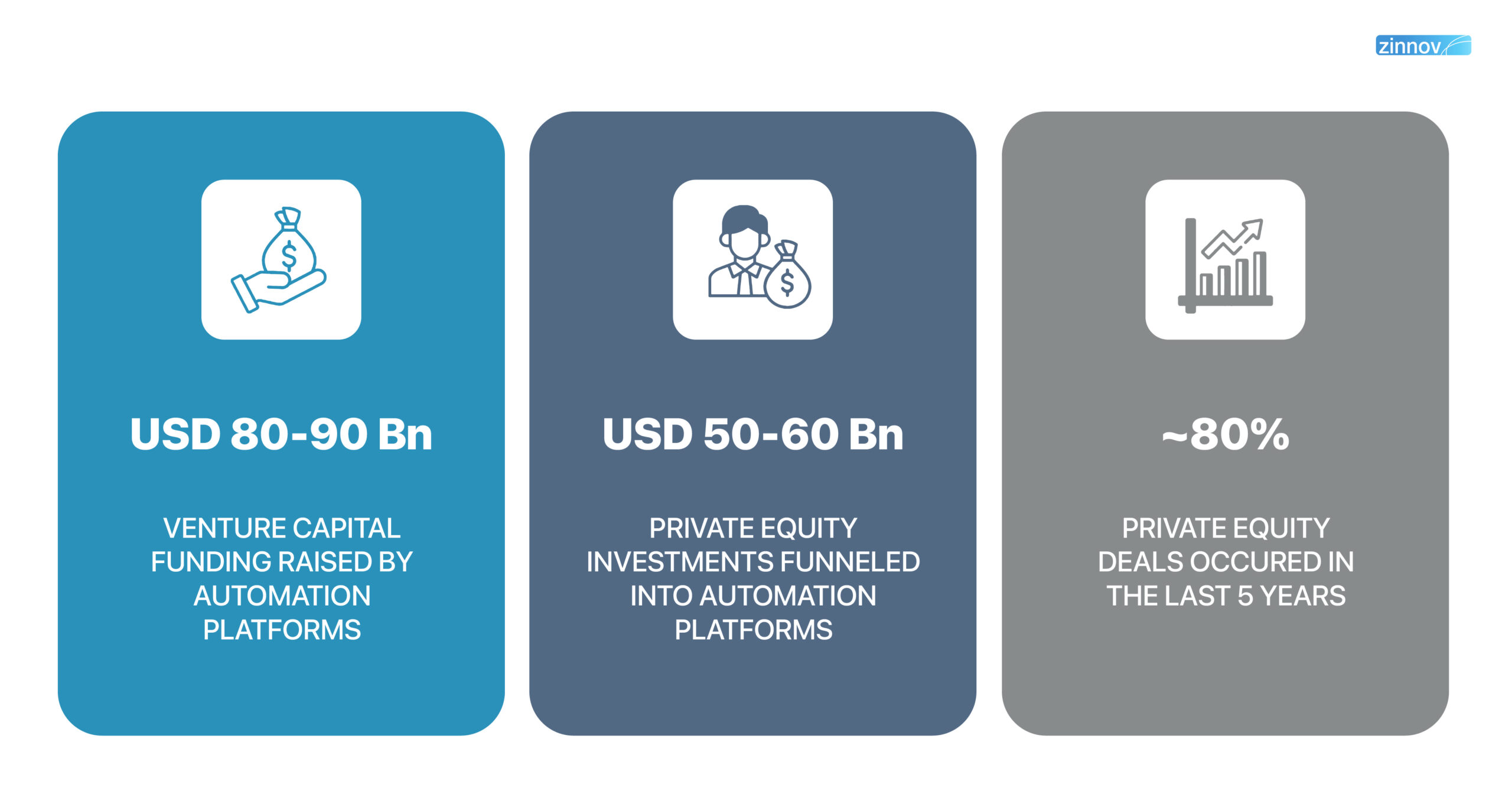

Fueled by immense potential, the Automation platforms underpinning Intelligent Automation have attracted significant funding interest. In fact, over USD 80-90 Bn has been invested, primarily led by Venture Capital (VC) firms. VCs have benefited from investing in Intelligent Automation due to its value delivery through technological innovation.

For instance, Earlybird Ventures led a seed round in UiPath in 2015, alongside Seedcamp and Credo Ventures, when the company was valued at USD 7.5 Mn. Upon UiPath’s IPO in 2021, valued at USD 35 Bn, Earlybird Ventures realized an investment multiple of ~4,500x.

Now, this surge of Intelligent Automation as a key driver of technology progress is capturing the attention of PE firms. These investors are starting to dive into the IA space, joining hands with VC firms to back this technology. It’s a recognition of IA’s potential to redefine the marketplace, driving PE firms to strategically invest in companies at the forefront of IA innovation. Their goal?

To unlock new opportunities, fuel growth, and enhance the value they deliver to stakeholders. It’s a strategic play to refine operations and lead the charge in tech evolution, ensuring their portfolios not only thrive today but are well-positioned for the future technological landscape.

Private Equity Investment in Automation

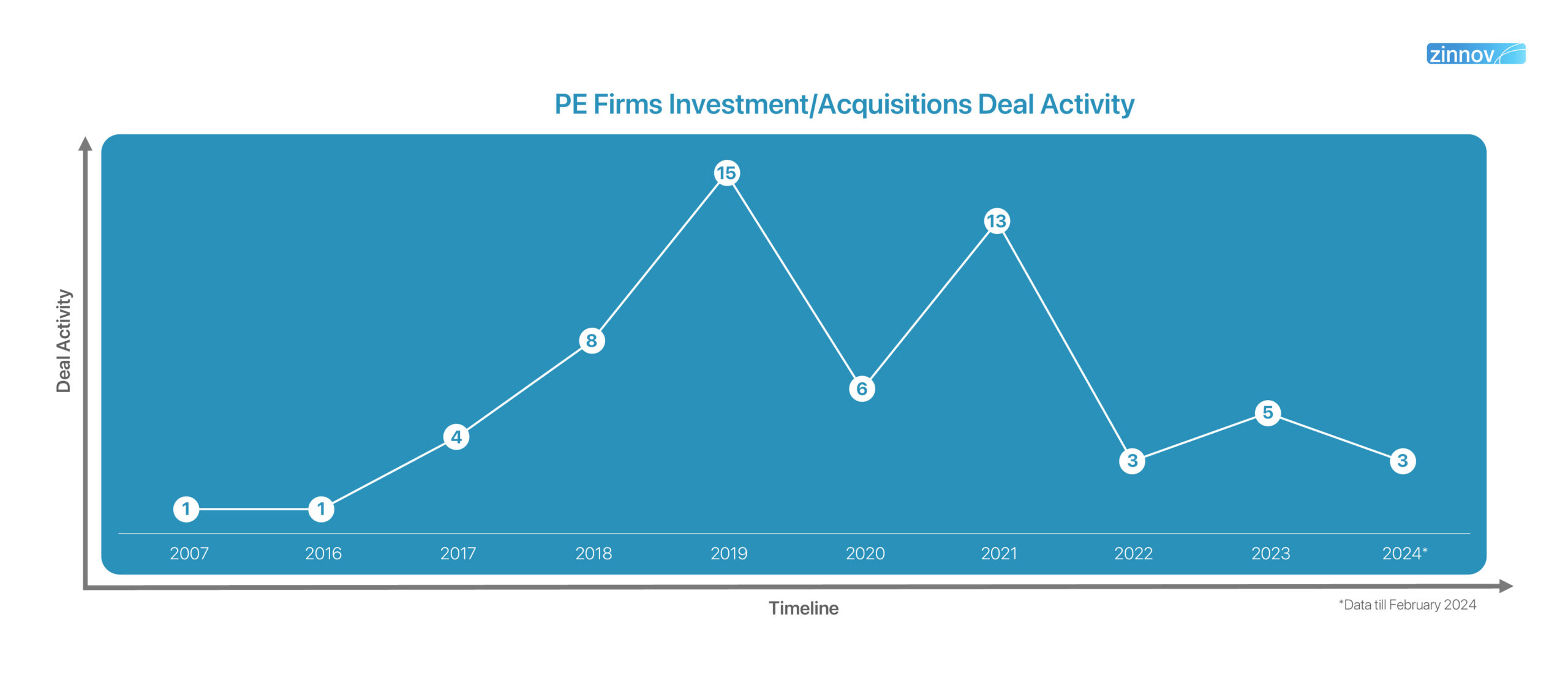

The surge in interest from PE firms underscores a strategic convergence between Finance and cutting-edge technology. Over 60 transactions have already taken place within the Automation sector, combining financial acumen with technology innovation – a partnership primed to shape the future business landscape.

Despite the initial draw to the Automation sector, PE investments slowed down in 2022 and have remained relatively modest into 2023. This slowdown occurred due to a confluence of macroeconomic and technological factors.

PRIVATE EQUITY INVESTMENTS IN TECHNOLOGY SERVICES 2023

Reasons Behind the Decrease in Private Equity Investments in 2022 and 2023:

Rising Federal Interest Rates: The Federal Reserve raised interest rates consecutively 11 times, reaching a range of 5.25% to 5.5%, the highest level in 22 years, by October 2023. This increase made borrowing more expensive, directly affecting PE firms’ ability to finance leveraged buyouts in the Intelligent Automation sector. The higher cost of capital led to a revaluation of potential returns from investments in this technology-driven field, often resulting in a more cautious approach.

Economic Slowdown and Recession Fears: Concerns over a slowing economy made PE firms more risk-averse, particularly for Intelligent Automation companies sensitive to spending fluctuations. PE firms leaned on the Rule of 40 – that growth rate + profitability should exceed 40% – to evaluate these deals. With tempered growth estimates due to uncertainty, following the Rule of 40 was critical to avoid overpaying and upending the ratio. This made PE wary of Intelligent Automation given its lower growth potential.

Uncertainty with Generative AI Introduction: The emergence of Generative AI like DALL-E and GPT-3 introduced uncertainty despite their potential. PE firms grew cautious about long-term viability and ethical risks like misinformation from realistic “hallucinations.” The opaque inner workings also raised accountability concerns. This made PE firms hesitant to invest in Intelligent Automation integrating immature Generative AI capabilities.

Capital Shift Impact on Smaller PE Firms: The consolidation of capital in PE’s largest funds meant less funding available from specialized smaller firms that had propelled Intelligent Automation’s rise. As first-time funds and raises under USD 5 Bn decreased, essential early-stage capital for Intelligent Automation platforms diminished, exacerbating the slowdown in investment within the sector.

Challenges in PE Performance: PE experienced its first negative performance since 2008, recording a 9% return. This concluded a five-year streak as the highest-performing private asset class. Tech-focused buyout funds underperformed for the second consecutive year, and VC lagged buyout strategies for the first time since 2017. The industry narrative shifted from beta to alpha, with less alpha available.

However, green shoots have started emerging that could reinvigorate PE firm’s interest in Intelligent Automation. Amid a more favorable economic climate, marked by early indicators pointing to a potential drop in interest rates and signs of global economic revival and expansion in 2024, PE firms are increasingly turning their attention to the automation sector. This attraction is reinforced as uncertainties around Generative AI begin to clear, offering a more transparent understanding of its capabilities and limitations. The integration of Generative AI with the Intelligent Automation technology stack is poised to boost business efficiency and consumer confidence.

Furthermore, PE firms are increasingly focusing on direct investments. Forbes reports that direct investments surged to an impressive USD 200 Bn in 2024, up significantly from the USD 26 Bn recorded in 2023. This trend towards direct investment in PE observed in 2024, is expected to broaden into the Intelligent Automation sector as well. Already, in the first two months of 2024, Kore.ai, Screendragon, and Sema4.ai have secured PE deals, underscoring the sector’s growing appeal.

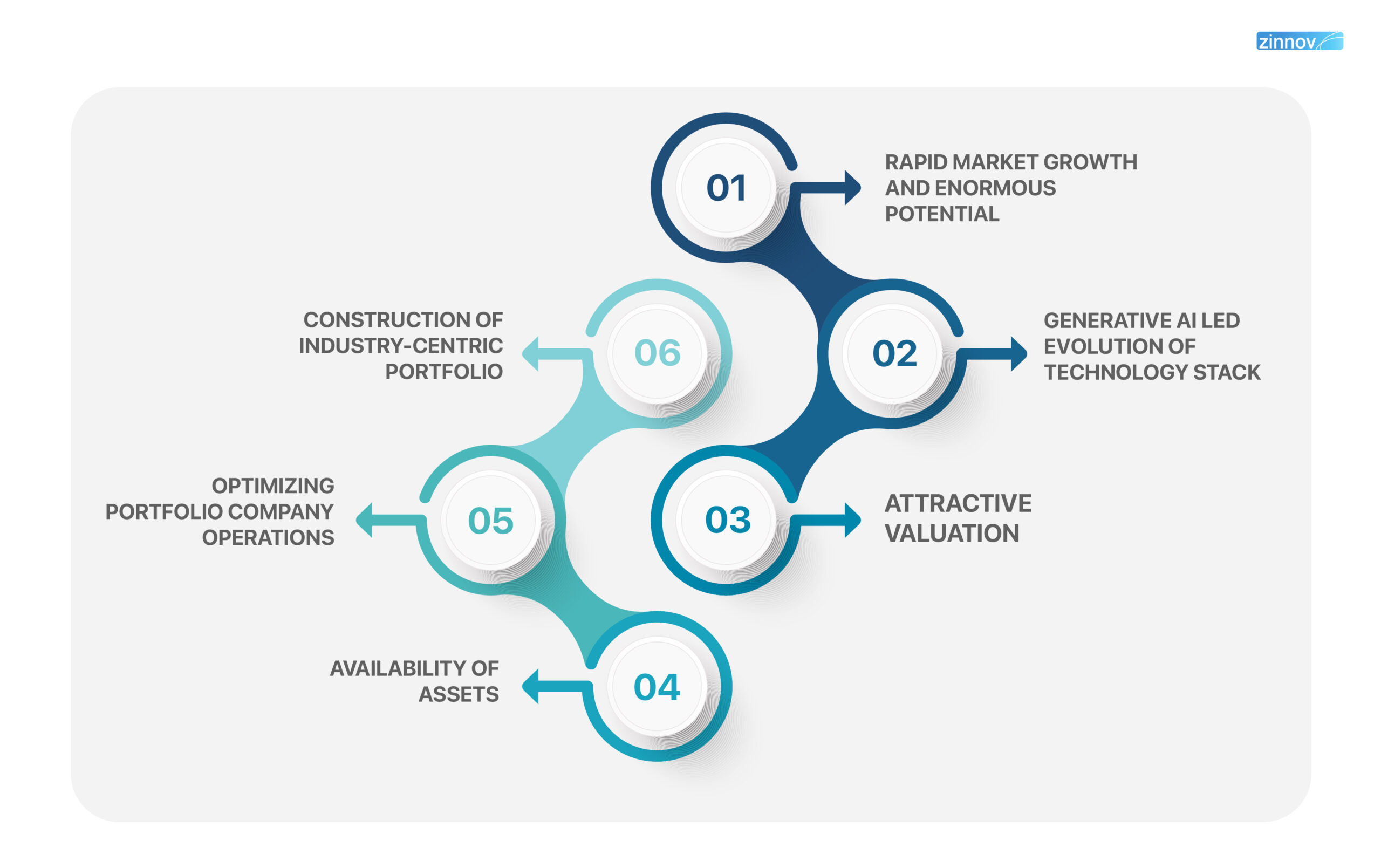

Factors Attracting Private Equity to Automation

The burgeoning interest of PE firms in Automation-focused companies stems from a variety of strategic and financial factors, all intricately aligned with their long-term objectives and aspirations. Key reasons attracting PE to Intelligent Automation include:

Rapid Market Growth and Enormous Potential: Senior executives are actively emphasizing digital transformation and prioritizing the adoption of the latest technologies to achieve this goal. Within digital transformation, Automation emerges as the top technology priority, with 64% of CXOs rating it as a key focus. The market size for Automation is currently valued at USD 50-60Bn, indicating significant growth potential. Moreover, ~95% of Fortune 250 enterprises have embarked on their automation journey, with nearly 80% still in the early stages, signaling massive growth potential as they progress toward automation maturity. Private equity firms are increasingly drawn to the vast market opportunities presented by the rising demand for Automation technologies.

Clearlake Capital acquired Tungsten Automation (formerly Kofax) with the aim of securing an asset capable of driving enterprise digital transformation. They chose Tungsten Automation for its proficiency in automating document-intensive workflows and its utilization of technologies such as RPA, IDP, process orchestration, and analytics to streamline implementations and deliver impactful outcomes.

Generative AI-Led Evolution of Technology Stack: Automation technologies are often disruptive, reshaping industries and creating new business models. The technology stack of Intelligent Automation is ever evolving with new technologies being administered in it, Generative AI is one such technology that is gaining prominence. Primarily driven by VC investors, there has been a 10 times growth in total funding received by Generative AI since 2021. Platforms are also focusing on creating comprehensive end-to-end automation solutions to capitalize on the market opportunity. PE firms with existing investments in automation can adopt a bolt-on acquisition approach to enhance the value of their current portfolio company to create synergies, expand market reach, and improve overall competitiveness by offering an end-to-end integrated automation platform.

Thoma Bravo implemented a bolt-on acquisition strategy to integrate a wide range of technologies into Nintex. Thoma Bravo accelerated Nintex’s growth by facilitating the acquisition of Promapp, Enablesoft, and AssureSign to broaden their offerings in process mining, RPA, and E-sign technology. This strategic move positioned Nintex as a one-stop destination for automation solutions.

Attractive Valuation: The valuation of approximately 85% of publicly listed platforms has experienced an average decline of around 50% over the past year. Aligning with the strategic and long-term objectives of private equity firms, the practice of acquiring companies based on normalized valuations prompts them to consider including automation platforms in their portfolio.

The EV/Revenue multiples for Appian, UiPath, and Pega have all exhibited significant changes, reflecting shifts in their valuations over time. For Appian, the EV/Revenue multiple decreased from 53x in 2021 to 11x in 2022 and further dropped to 5x in 2023, indicating a notable decline in valuation. Similarly, UiPath experienced a reduction in its EV/Revenue multiple, going from 17x in 2022 to 6x in 2023, signifying a decrease in its valuation. Pega followed a similar pattern, with its EV/Revenue multiple decreasing from 11x in 2021 to 8x in 2022 and then further declining to 2x in 2023.

Availability of Assets: There are over 1,400 automation platforms, with 50% of them having less than USD 10 Mn in revenue, 28% with USD 10-50 Mn in revenue, and 23% with greater than USD 50 Mn in revenue. Apart from the availability of assets in different revenue ranges, there is a good spread across geographies: 52% of assets are based in North America, 29% in EMEA, and 17% in APAC. For private equity firms seeking promising avenues, automation emerges as a compelling choice. The multitude of platforms not only signifies a thriving demand for automated solutions but also underscores the sector’s resilience and potential for sustained growth.

Optimizing Portfolio Company Operations: Private equity firms are acquiring automation software companies to optimize their internal portfolio enterprises. This partnership offers a dual advantage to PE by enhancing the efficiency and profitability of their portfolio companies through automation, while the acquired automation platform gains access to a broader customer base and increased resources for scaling their solutions and driving innovation.

TPG Inc. which invests across various sectors including Retail & CPG, Healthcare, Services, and Real Estate, has been utilizing its acquired Intelligent Automation platform, Nintex, to optimize operations within its portfolio, including companies such as Airbnb, Cushman & Wakefield, among others.

Construction Of Industry-Centric Portfolio: Automation technologies frequently find applications across diverse industries, rendering them versatile investment opportunities. Enterprise Automation investments in Banking & Financial Services, Healthcare, and Manufacturing are projected to experience a CAGR of 40-45% from 2023 to 2028, while those in Insurance, Retail & CPG, and Telecom & Media are expected to grow at a rate of 35-40% during the same period. Emerging platforms are entering the market with a focus on addressing industry-specific bottlenecks, propelling their growth in underpenetrated sectors, and establishing dominance in their niche areas. Private equity firms are investing in these platforms to penetrate these specialized markets and develop unique solution offerings.

TCV Capital has a strong emphasis on the healthcare industry and is actively investing in companies that promote digital transformation within the healthcare sector. As part of this strategic approach, TCV Capital made an investment in Syllable, a company dedicated to enhancing the patient experience through intelligent voice solutions for health system call centers and medical practices.

The Intelligent Automation space is changing the game, and Private Equity firms have taken notice of this development. With clear eyes on the sector’s growth and tech evolution, PE firms are making their move to leverage their financial expertise and strategic insights and reshape industries with smart, automated solutions.

The future of PE’s role in shaping the Automation revolution appears to be both promising and transformative. As PE channel resources into Automation companies, they become catalysts for change, fostering innovation, enhancing operational efficiencies, and driving competitive advantage across industries. This symbiotic relationship promises to accelerate the advent of an era marked by enhanced productivity and strategic business agility.

If you are a PE firm looking to invest in the space and wish to have a discussion, please reach out to us at info@zinnov.com to connect with our experts!

AI transformation in technology services firms is being stalled by an outdated Client Partner model. Discover why triple fluency will define AI leaders.

18 Feb, 2026

AI transformation in technology services firms is being stalled by an outdated Client Partner model. Discover why triple fluency will define AI leaders.

31 Jan, 2026

Explore the Top 10 Agentic AI Trends for 2026 and what CIOs and CTOs must do as AI moves from copilots to autonomous, enterprise-scale execution.