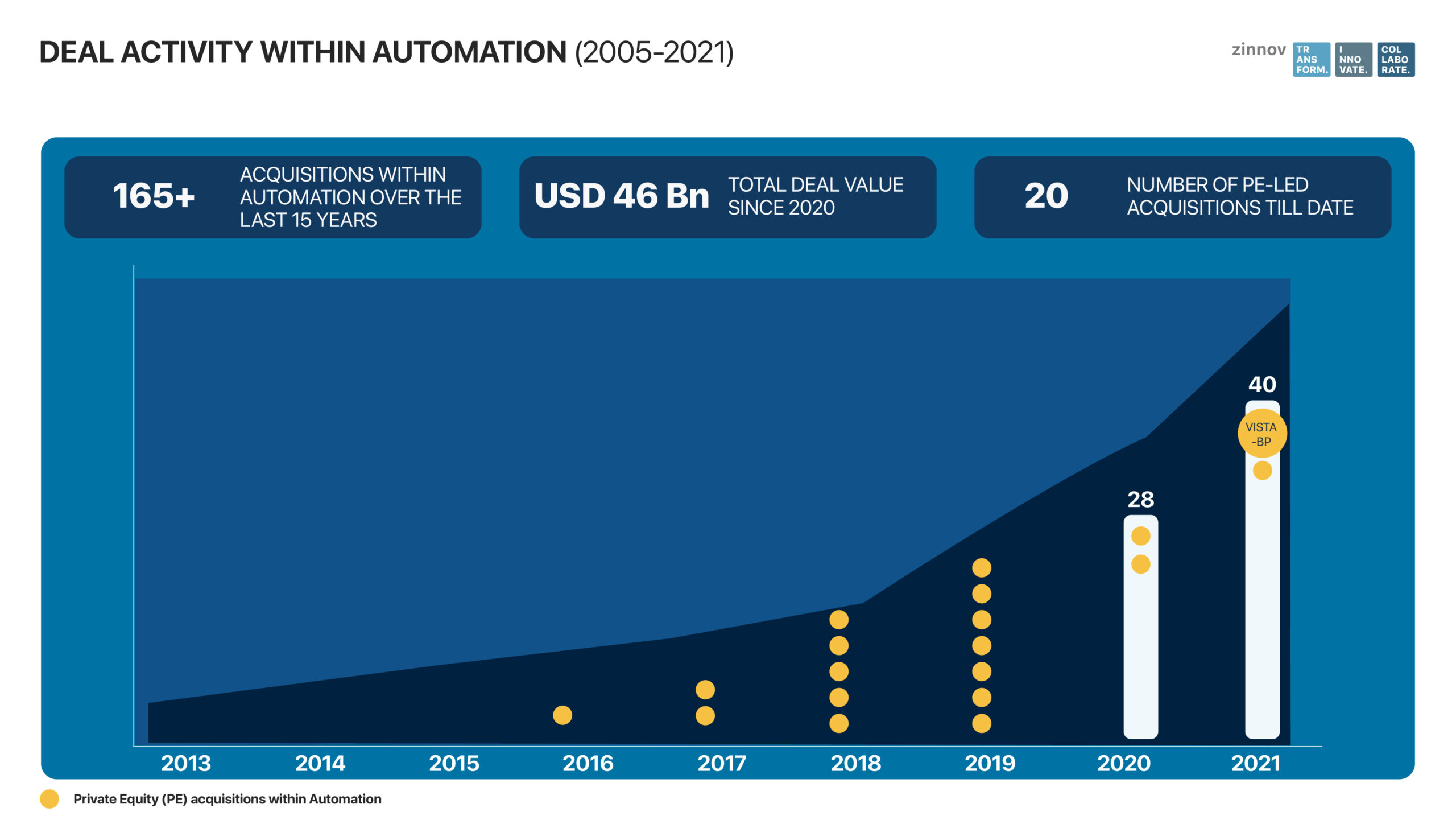

The Automation space has been abuzz with a lot of action over the past year, with flamboyant acquisitions, sizeable Venture Capital (VC)/Private Equity (PE) investments, and IPOs, among other things. UiPath going public was among the major news back in Q1 2021, with a massive valuation of USD 35 Bn. Additionally, funding in excess of USD 12 Bn has been poured into the Automation space over the past year. And given that there are 1400+ platforms within the Automation space, there has been immense consolidation with acquisitions intensifying further during the pandemic. Interestingly, Automation presents a sizeable market of more than USD 15 Bn globally, which is expected to reach more than USD 110 Bn over the next five years.

Even PE players have been extremely active within the Automation space over the last 5 years, with more than 20 acquisitions to show for it. And Vista Equity Partners just made the biggest acquisition within the Automation space by lapping up Blue Prism (BP), one of the Big 3 RPA firms, for a staggering USD 1.5 Bn!

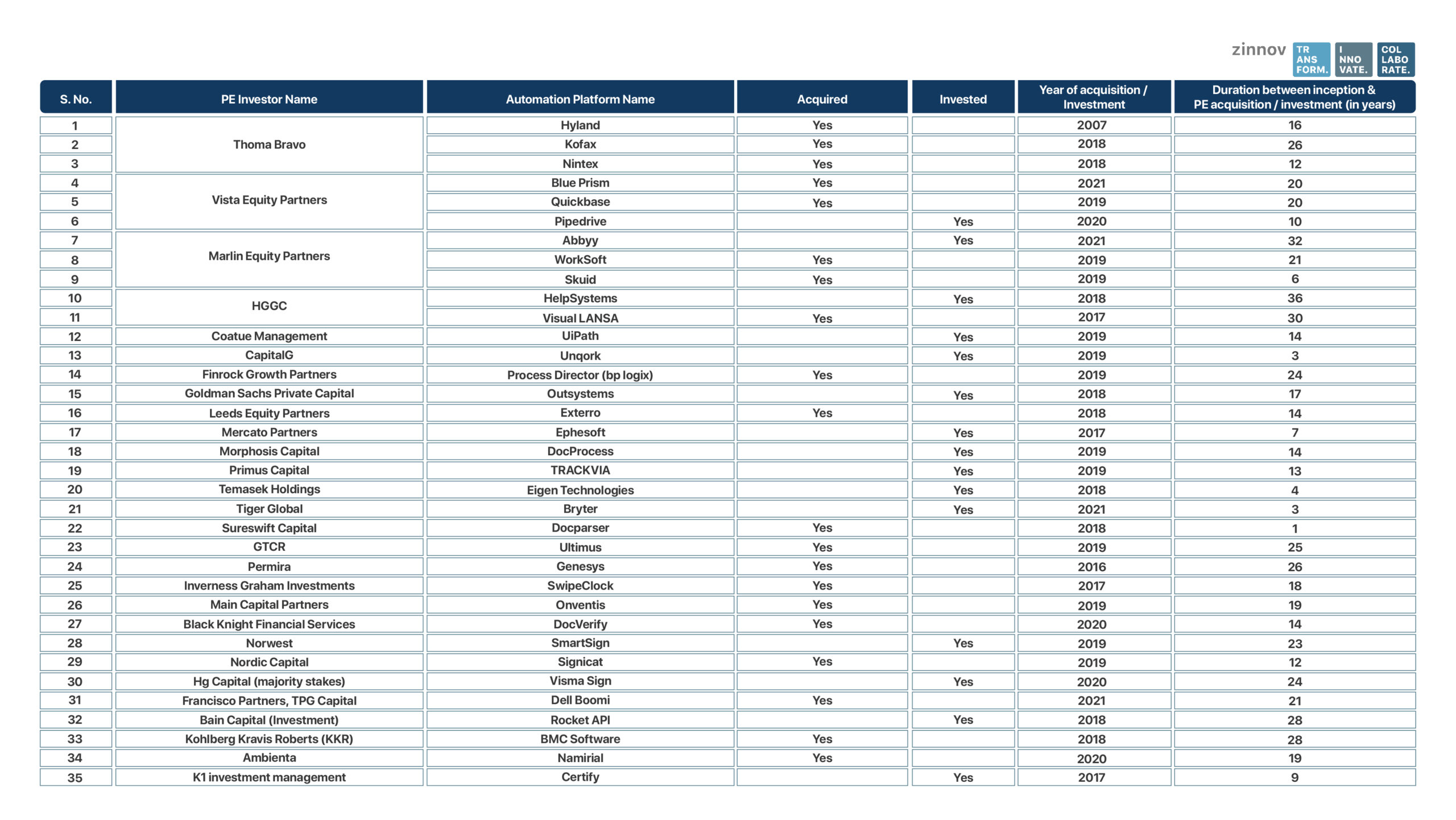

Here’s a list of all the PE-backed acquisitions within the Automation space till date.

Vista’s Automation Play

The table above makes it clear that both larger and mid-sector PE firms have had their eye on the red-hot Automation space, over the past few years. Even Vista has been an active investor within Automation, with acquisition of assets such as Olive in June 2021 (a HealthTech start-up focused on RPA and AI), Quickbase in April 2019 (No Code platform for app development), and Tibco back in 2014. Vista plans to merge BP within Tibco, which focuses on API-led integration, data management, and analytics, and currently serves more than 10,000 blue-chip enterprise customers. While combining Intelligent Automation from BP with the API and analytics prowess of Tibco is a good move, it would have been far more exciting if there was a plan to merge BP with Quickbase to augment Intelligent Automation with much needed No Code capabilities. Even the addition of Olive would have been good and added more healthcare-related capabilities to BP (which is predominantly focused on the BFSI sector, accounting for ~50% of its revenue share).

Unlocking Investment Potential

Private Equity Riding the Wave of Intelligent Automation

The Tibco-BP merger seems more like Vista preparing Tibco for a potential sale in the next 12 months. A closer look at some of Vista’s exits over the past several years reveals that a majority of them have been in the 2-5 years range since acquisition. In fact, Vista portfolio companies such as Applied Systems, Aspect, BigMachines, Wrike, and Main Street Hub were all sold off within the 2-3 years of being acquired. The most notable has been Vista’s Marketo acquisition for USD 1.8 Bn back in May 2016, which was later sold off to Adobe within 2 years, for an impressive USD 4.75 Bn.

Tibco has been a part of Vista’s portfolio for the last 7 years and was acquired for a massive USD 4.3 Bn back then. Since then, there have been several bolt-on acquisitions that Vista has undertaken to strengthen Tibco – the most noteworthy ones being Nanoscale in 2017 (API), Scribe Software in 2018 (data automation), SnappyData in 2019 (analytics), and Information Builders in 2020 (analytics). There were reports back in July 2021 about Vista considering a potential sale of Tibco, which was being touted at upwards of USD 7 Bn; but it never materialized. This is definitely a concrete step by Vista to bolster the Tibco arsenal further with Intelligent Automation, to fetch it a higher price. Vista is not looking to be in the Intelligent Automation space in the long run. In fact, it is exploring it as a short-term strategy to sell Tibco-BP combined entity at a massive premium!

Vista’s Blue Prism Gambit

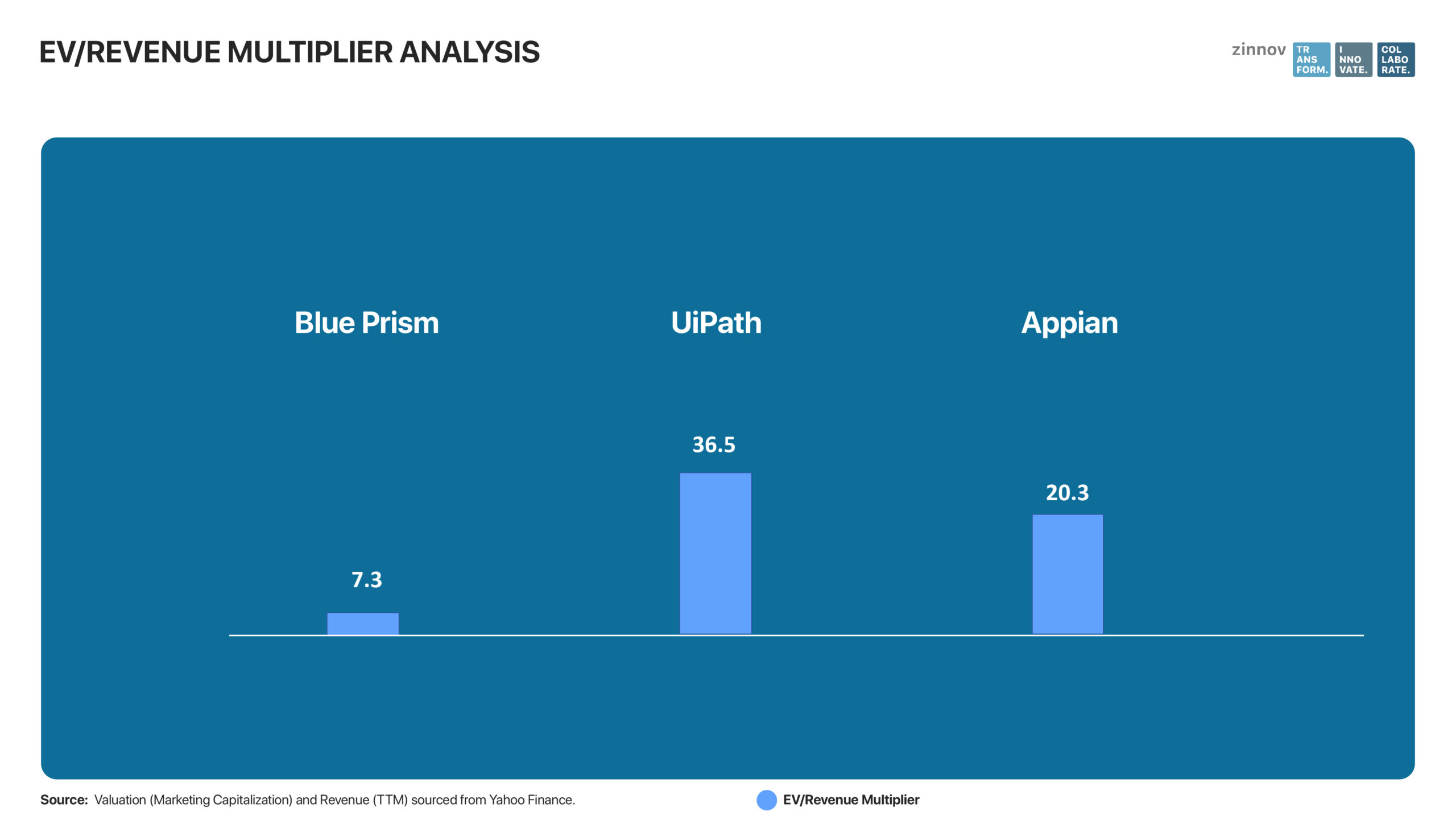

Vista has lapped up BP at very favorable multiples. A deeper analysis of the EV/Revenue multiples vis-à-vis its peers such as UiPath and Appian presented some interesting analysis. It is evident that the EV/Revenue multiples for BP are way below its peers – as much as 5 times lower than UiPath, for instance. This points towards the challenges that BP was facing in its revenue-generating ability.

As per the official filing, BP admitted to facing tough times since its last annual general meeting, with questions being raised on its continuing losses, protests over its leadership, and intensifying competition from the likes of UiPath, Microsoft, and other prominent players. Interestingly, only 65% of investors voted in favor of Jason Kingdon to be re-elected as the CEO, and a significant percentage of leading shareholders proposed a potential sale of the company. BP explored multiple strategic options over the past 4 months, and finally agreed to the acquisition bid from Vista. Kingdon had come to the helm at BP as its Chairman and CEO in April 2020, but the Board has now commenced the search for a new CEO.

Blue Prism, interestingly has been the category creator for RPA, founded back in 2001 by Alastair Bathgate and David Moss. BP is also credited with coining the term “Robotic Process Automation” in 2003, which eventually gave birth to the RPA space and saw the mushrooming of other players such as Automation Anywhere and UiPath (then DeskOver). BP was also among the first Automation platforms to go public in 2016 on the London Stock Exchange, but has been struggling ever since.

Blue Prism’s Lackluster Showing so far

When we conducted a detailed assessment of BP’s product innovations across the years, and augmented them with their latest annual filings, we found the below key areas of improvement that we identified for Blue Prism.

Lack of holistic focus on Automation: Though Blue Prism was very strong in RPA, especially the unattended (or back-office) automation, there was resistance in accelerating its focus on attended (or front-office) automation for the longest time. BP was also slow to augment its RPA product with complimentary technology areas such as Intelligent Document Processing (IDP), Process Mining, Low Code capabilities, API Integration, Intelligent Virtual Agents, and so on.

Weak market positioning and perception: Combined with the lack of holistic focus on Automation, BP continued to be perceived predominantly as an RPA-only player in the market and did nothing to evolve its positioning as a more holistic, end-to-end Intelligent Automation player. A simple keyword search of its annual report (FY20) pointed out 20+ mentions of RPA, while only 2 mentions of No Code, and 1 mention of IDP, and there was absolutely no mention of Low Code, Process Mining, Task Mining, iBPMS, API, Intelligent Virtual Agents, and so on.

Lack of focus on M&A for rapid product innovation: BP was slow to respond to the market trends, with low focus on R&D and product innovation, and even lower focus on its inorganic strategy. On the other hand, the other two players among the Big 3 platforms – Automation Anywhere (AA) and UiPath – made rapid strides to either build or acquire capabilities to bolster their holistic focus on Automation. For instance, BP embarked on a journey to build Decipher – its IDP product back in 2019. It spent 15 months building this product grounds up, and while it’s a good addition, it is not the most preferred IDP product out there. Instead, BP would have rather benefitted from acquiring a specialist IDP platform to gain far superior technology.

Relatively low focus on R&D and Globalization: Research and Development is another key differentiator in this competitive space, and BP was found to be lacking in its R&D spends as well. Though it claimed an increase in R&D spend by almost 124% since FY19, this only formed 12% of its revenue, which was way below the industry average of 25%+ for some of the leading vendors. What was even more interesting was the fact that BP also had minimal focus on optimizing its R&D talent footprint, since more than 90% of its Engineering R&D talent was found to be concentrated in high-cost locations such as UK and US which added to its cost of operations. Compared to this, most of BP’s peers such as UiPath, AA, Pega, and Kofax have at least 60% of their R&D talent present across the low-cost locations.

High spend on Sales & Marketing: Blue Prism has a very high ratio of Sales and Marketing (S&M) spending which is not a good indicator of a sustainable business. BP is spending ~60% on S&M, as a percentage of its revenue. Interestingly, the industry average for public-listed Automation platforms, the S&M spend typically hovers in the range of 40-45%. For instance, Appian has an S&M spend of 44%, while Pega is currently at less than 10%.

Lackluster Revenue Growth compared to peers: BP announced revenue of USD 191 Mn (according to its latest annual report for FY20), up 46% YoY since last year. Though the growth was impressive, it pales in comparison to UiPath, which announced FY20 revenues to the tune of USD 600 Mn+, with 80% growth YoY.

Average growth in New Customers and Retention Rates: BP has more than 2000 enterprise customers at last count, with 350 new logos added and 600+ customers upsold in FY20. However, on closer analysis, BP’s Customer Upsell percentage (as a % of the total customers) had been stagnant at 32-33% for the last three years (from FY18-FY20). Upsell as a percentage of new customers has also declined from 67% in H2 of 2017, to only 17% H2 of 2020. Also, UiPath has reached a global customer base of 9100+ at last count, with more than 600 new customers added in Q2 of 2021. Even the Net Retention Rate (NRR) for BP was 113%, which though good, was again found to be lagging its industry peers such as UiPath, with an NRR of more than 145%! Interestingly, BP also lost more than 100 enterprise customers in FY20 owing to lower scale (with less than 5 bots deployed). This is definitely cause of concern given the intense and cut-throat competition within the Automation space.

Lack of comprehensive geo coverage: BP lacks holistic coverage across geographies, with bulk of its revenue (more than 85%) coming from Europe and North America. There is minimal focus on growth markets of APAC. This is in stark contrast with its close competitor UiPath, that has a widespread focus across all major geographies, and commands more than 30% revenue from growth markets.

Hence, BP was clearly unable to keep pace with the breakneck speed at which the market around it was progressing, and it has lost the plot vis-à-vis some of its peers in the last 2-3 years.

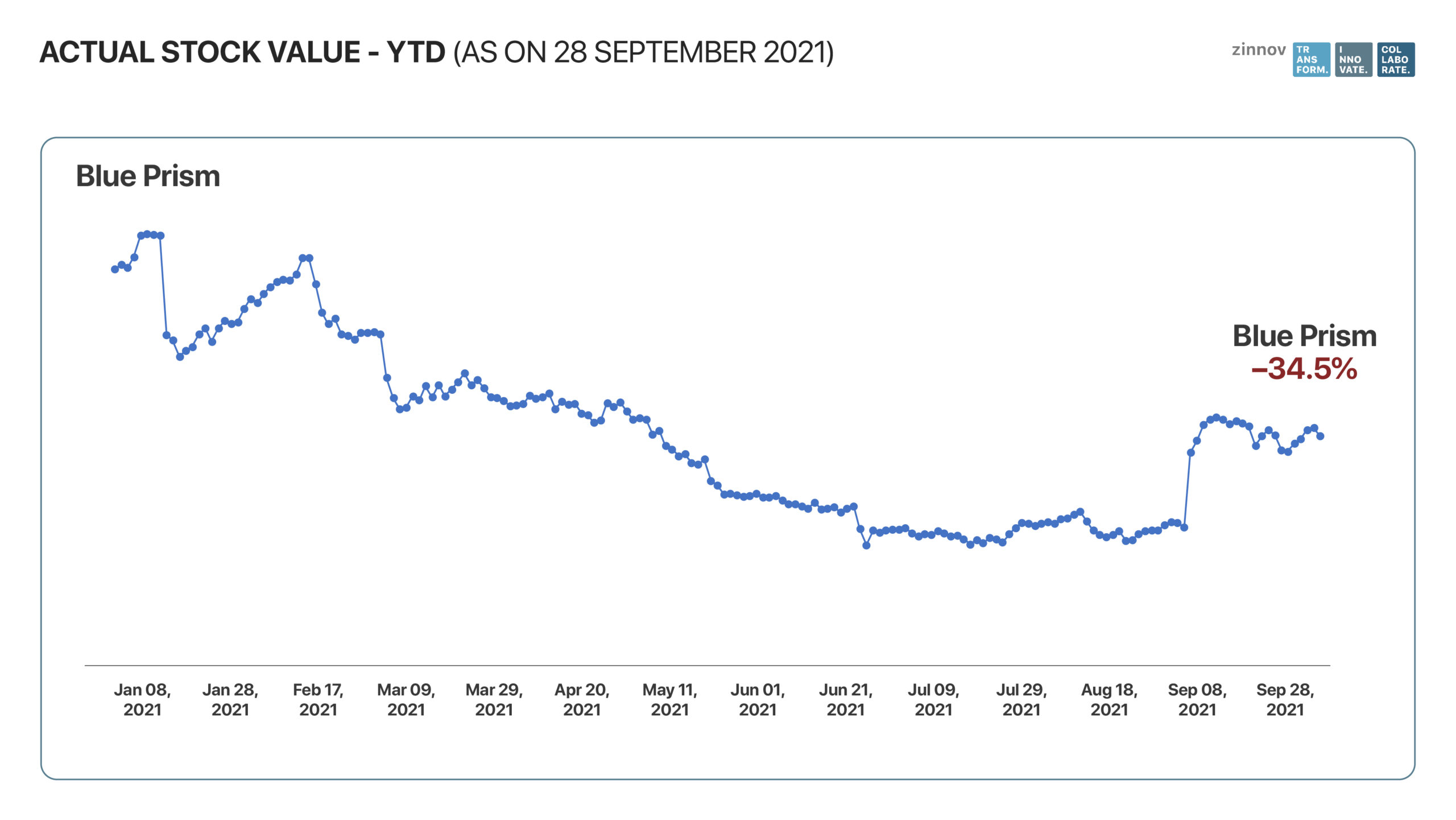

Consequently, the BP stock price has also taken a beating. The illustration below is the stock price analysis for Blue Prism YTD, which shows that the BP stock has fallen by almost 34.5% since the beginning of 2021.

Hence, owing to these challenges and the persistent decline in its stock price, Blue Prism was reeling from continued pressure from shareholders to make strategic changes. We had had multiple conversations with Jason Kingdon and had the opportunity to advise him on how he could tide past the bottlenecks and ride the growth wave of the Automation space. And one of the first pieces of advice we had provided was to take the company private or explore a potential PE acquisition. It was only a matter of time, and it is good to see that this has finally materialized.

These challenges have made Vista’s acquisition a sweet deal at extremely favorable multiples. While the BP acquisition is a great move by Vista, it has a long winding road ahead of it in order to unlock maximum value from this acquisition.

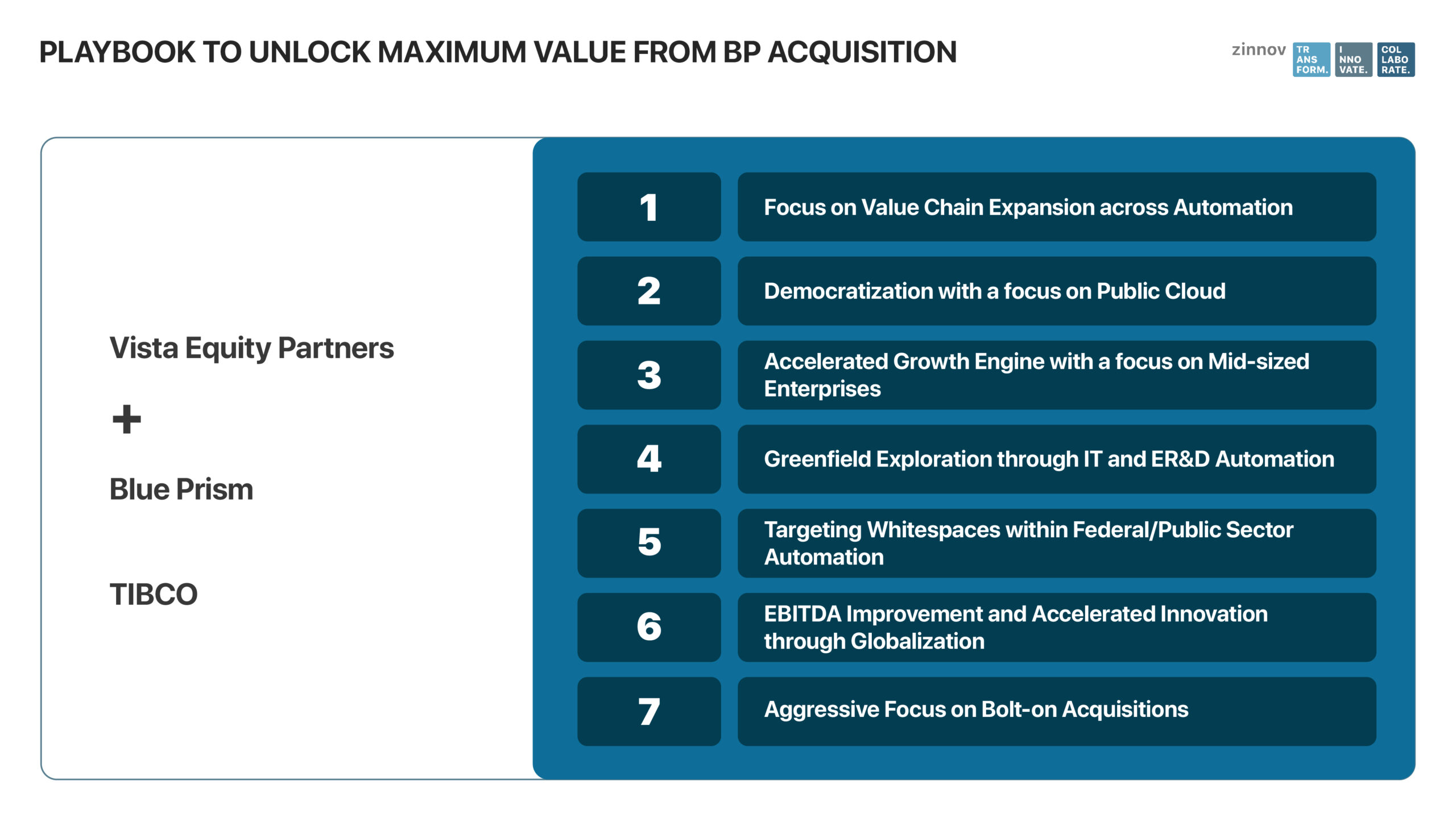

Zinnov Recommendations for Vista to unlock potential from Blue Prism

Focus on Value Chain Expansion across Automation: Enterprises today are looking for platforms that align well with the holistic Automation approach (as highlighted above). Hence, it is critical that Vista enables BP to build an end-to-end value proposition to cater to enterprise customers better. BP needs to focus on its Build-Buy-Partner strategy to become the one-stop “platform of platforms.”

Democratization through focus on Public Cloud: Cloud and web-based Automation deployments have already intensified in the COVID era. While Public Cloud accounted for not more than 10% of enterprise Automation deployments in 2020, it is expected that this trend will accelerate to 2X by the end of this year. At the same time, BP only managed a meager 8% share of revenue from its Blue Prism Cloud deployments (FY20). Hence, it is vital for Vista to enable an aggressive BP push towards Cloud and web-based deployments, which would continue to be important even as COVID-related challenges subside.

Accelerated Growth Engine with focus on Mid-sized Enterprises: A majority of leading platforms are targeting large enterprises today. In fact, Zinnov analysis reveals that more than 90% of the Fortune 250 enterprises are already investing on Automation in a meaningful way. Given this intense competition for large enterprises, SMBs and especially mid-sized enterprises are poised to emerge as the next major customer segment within Automation. These SMBs/mid-sized enterprises are more open to Cloud-based deployments and are also exploring the up and coming open-source RPA platforms (the likes of Robocorp, Automagica, etc.). This segment will account for almost 30% of the platform revenue by 2022.

Greenfield Exploration through IT and ER&D Automation: While the first wave of Automation was led by horizontal business processes (such as Finance & Accounting, Human Resources, etc.), Zinnov anticipates a growing demand for IT and ER&D Automation use cases – aligned to IT Operations Management (ITOM), IT Service Management (ITSM), and Application Development & Maintenance (ADM), to name a few. This category is likely to contribute to 15-20% of the total platform investments by enterprises in the next 24 months, and hence, is another critical capability to be imbibed by platforms.

Targeting Whitespaces within Federal/Public Sector Automation: Federal government and public sector agencies have been significantly active in their adoption of Automation use cases, especially during COVID – both to enable citizen services and to enhance employee efficiency internally. This trend is expected to continue and amplify going forward. BP only has about 6% share from Public Sector as of now (H1 2021), and therefore needs to amplify manifold over the next 8-12 months’ time frame.

EBITDA Improvement and Accelerated Innovation through Globalization: This is a critical consideration to reap the benefits of cost-effective locations and their innovation ecosystems. As discussed above, BP has more than 90% of its Engineering R&D talent based out of high-cost locations such as UK and US. Vista needs to flip this to have at least 30-35% ER&D talent presence in low-cost, innovative locations, not only to optimize costs, but also to reap the benefits of high-quality talent.

Aggressive focus on Bolt-on Acquisitions: BP has clearly been lagging in its acquisition playbook, and Vista needs to change it. It would be vital for Vista to augment BP’s existing capabilities with critical capabilities such as Process Mining and Low Code/No Code technology. Both spaces are in high demand from enterprise customers and have also seen immense traction from platforms players. IBM-myInvenio, Appian-Lana Labs, and SAP-Signavio have all been key acquisitions this year alone, to obtain process mining capabilities. Even Low Code/No Code space has seen activity, with UiPath launching its UiPath Apps, Kofax launching TotalAgility (KTA), and multiple acquisitions including Google-AppSheet, Celonis-Integromat, and SAP-AppGyver. Even within IT automation, as discussed above, there are 50 assets out there that BP can acquire to short-circuit the time-to-market. All this would help bolster the Intelligent Automation arsenal for the combined Tibco-BP entity.

The way forward for Vista with respect to its Blue Prism acquisition remains to be seen. If Vista intends to stay invested within the Intelligent Automation space and look towards a longer-term strategy vis-à-vis its Tibco-BP combined entity, then it clearly needs to make some critical adjustments in its go-to-market strategy and make some strategic bolt-on acquisitions to help recover lost ground and momentum. This would also bring Vista head to head with other PE players such as Thoma Bravo who have been very active in the Automation space. Thoma Bravo has not only acquired prominent assets over the years, but has also nurtured them with several strategic acquisitions. For instance, Hyland acquired Another Monday in August 2020 to add Intelligent Automation capabilities and followed it up with acquisitions of Alfresco (Oct 2020) and Nuxeo (April 2021) aligned to document management and Enterprise Content Management (ECM). It would be interesting to see how the TB vs Vista battle plays out, should Vista take this longer route towards value creation.

If, on the other hand, Vista is in it for the short-haul and looking for a quick way out, it would merge Tibco and BP and bet on their mutual synergies to play out (RPA and Intelligent Automation being bolstered by API capabilities), and eventually sell all or part of the combined entity within the next 12 months. With this route, while Vista would gain in the short-term, but would not be able to unlock the full potential and value from BP.

As of now, it’s anyone’s guess as to what path Vista will eventually take. But one thing is for certain – Vista, with this big-bang acquisition, has paved the way for other PE firms to follow suit. And the PE momentum within the Intelligent Automation space is here to stay!

For more in-depth analyses on Private Equity investments in the Automation space, write to us at info@zinnov.com.