An excellent infographic about #WhyGICs and #WhenGICs can be downloaded here.

Resilience is imperative to business health especially when the world faces rapid, unpredictable, and unprecedented change. To combat crises and thrive in the new normal, a majority of enterprises are rethinking their existing business practices at a broader scale, and shifting focus on resource availability and innovation. This is why most HQ leaders are on the hunt to set up Centers of Excellence (also known as global capability centers) at strategic locations and develop a digitally skilled workforce that can take ownership and innovate new products.

India has the second-highest talent pool of 2.5 Mn focused on software product engineering. Additionally, it is also among the top three countries that produce the highest number of science, technology, engineering, and mathematics (STEM) graduates every year. The total headcount of STEM graduates adds up to 1.5 Mn yearly (out of which 40% are women) which is more than 3 times the size of STEM graduates per year in the U.S. This massive reservoir of relevant tech talent pool with strong English-speaking proficiency can be trained and leveraged at scale by organizations desiring to expand their team and expedite their innovation goals. From the perspective of new-age skillsets like Data Analytics, India houses 1/4th of the global talent pool.

As of 2020, India has a voluntary attrition rate of 12% which plummeted to 8.3% towards the end of the year and then peaked again to 14.1% in 2021. One of the primary reasons for the rise in attrition has been the growing market demand for technology talent especially in the ER&D (Engineering Research & Development) function, and increase in talent migration and remote working opportunities due to COVID -19.

In fact, the talent market has become fierce with a long notice period policy and multiple offers being rolled out by companies, which is accentuating the challenge of no-shows in India. We believe this could be a blip and not a permanent trend. Look out for our next article on ‘attrition management’ which deep dives into these trends.

In terms of the government contributions here — to further help reduce the labor surplus and upskill the Indian tech talent, there is an increased focus on skill building (through training programs, exhaustive research materials, etc.), affordable education, and accelerated incentives to encourage corporate growth and entrepreneurship. This has helped in making STEM education and technological research more inclusive.

It is important to know the key factors that have helped develop India’s robust innovation ecosystem — research investment, education policy, researcher density, publication output, number of patents registered, and the start-up environment. These dynamic factors have led to India’s emergence as the third-largest start-up ecosystem across the globe.

As of November 2020, India had 31 unicorns. Currently, the number of unicorns has expanded to 44. India’s mature tech ecosystem would expedite the growth of unicorns in this country, 100+ unicorns forecasted by 2025, despite being impacted by COVID-19.

Furthermore, strong partnerships between tier-1 academic institutions (IIT, NIT, IIsc, etc.) and tech giants (like Bosch, IBM, Accenture, Google, Microsoft, among others) have bolstered AI/ML research. For example:

It’s safe to conclude that the formation of these centers has helped build proof of concepts, develop expertise, accelerate innovation, and create a comprehensive go-to-market (GTM) strategy to support next-gen digital transformation.

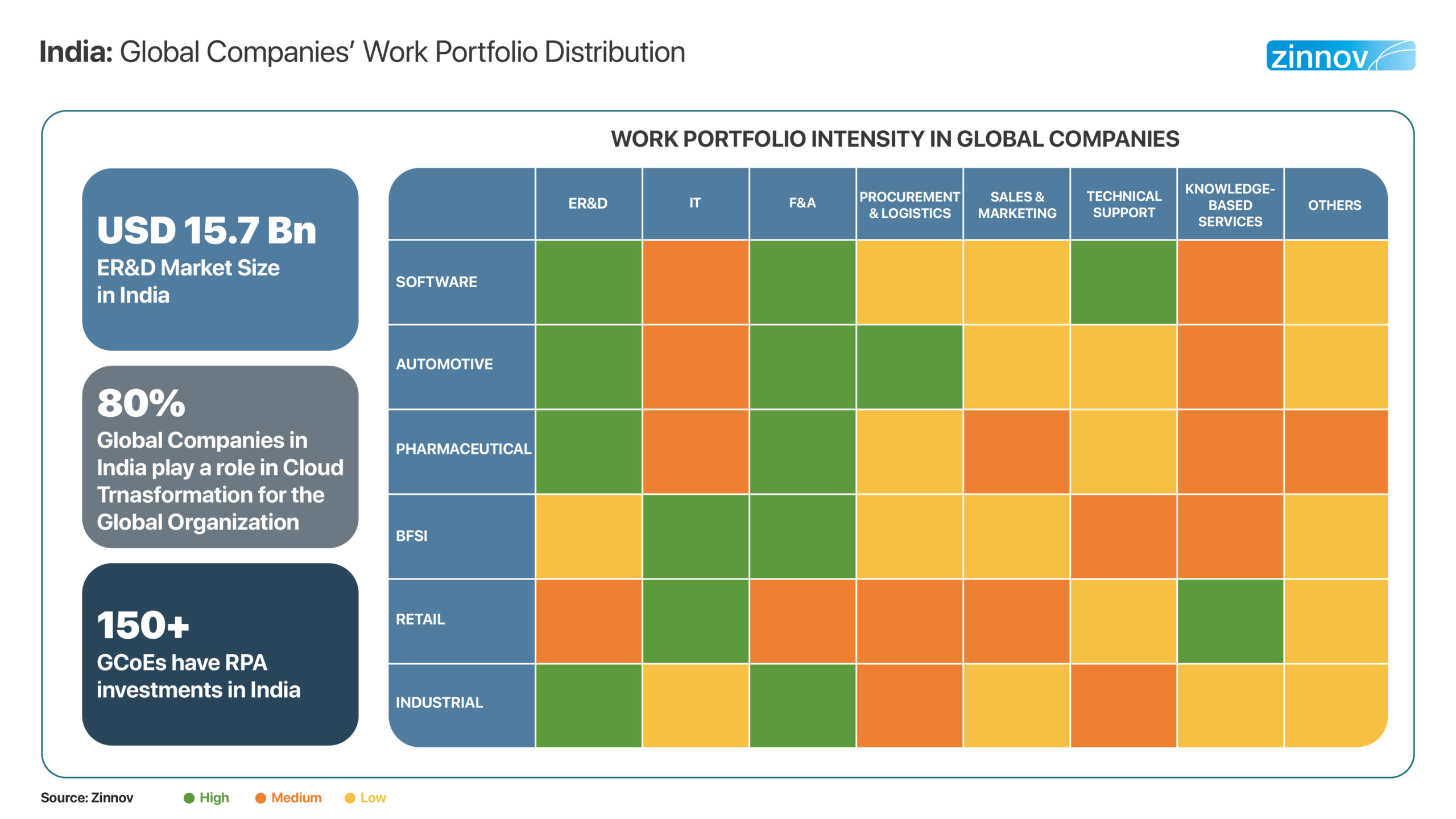

These trends reflect the confidence global leaders have in India’s vast talent pool. Additionally, the work portfolio spread in global companies is dominated by the Software, Industrial, Automotive, Pharmaceutical, BFSI, and Retail verticals. The main focus for these domains has been around AI/ML, IoT, Data Analytics, and Cloud Computing to scale innovation and enhance capabilities.

In fact, the ER&D – (Engineering Research & Development) spend has reached a whopping USD 15.7 Bn, with close to 150+ CoEs leveraging Automation investments and an estimated 80% of companies already playing a definitive role in Cloud transformation for their parent organization.

Some of the industrial highlights are — Microsoft developing a precision agriculture solution for farmers using Azure ML, Honeywell building an IIoT (Industrial Internet of Things) platform for predictive maintenance and asset management, Bosch leveraging the start-up ecosystem to drive disruptive solutions in Agritech, Meditech, etc. And this shall peak further with the Indian government deploying a massive USD 1.5 Tn for infrastructure development in tier-2 cities, including Coimbatore, Ahmedabad, Vadodara to name a few. This shall create room for substantial (talent and global center) backup, when Tier-1 cities are affected with issues beyond control (such as a pandemic).

Most enterprises are investing in Digital Engineering SPs to optimize their manufacturing and product development process and best meet three key business objectives – customer experience, operational excellence, and brand portfolio development to attract the right talent. This is due to the growing customer expectations, digital skill set requirements, and the sudden focus on digital transformation, that is bolstered by the global pandemic.

We believe by 2025, India shall account for 41% of the global Digital Engineering services market with an estimated valuation of USD 1.2 Tn.

The majority employable workforce in India is proficient in English and can indulge in multi-directional communication with stakeholders like investors, partners, customers, etc. The importance of the English language in India as a form of business and official communication holds a strong weightage and is reinforced by India’s colonial legacy, linguistic diversity, and the rapid growth of globalization.

The government has increased its support initiatives and modified its existing policies across education, funding, and infrastructure, to name a few. This is reflected in the World Bank’s Doing Business Report (DBR) of 190 Countries, where India has improved from the 142nd position in 2014 to the 63rd position as of 2020.

If an employee and an employer, have a duly signed legal contract in place the chances of disputes are minimal. In fact, most organizations in India create their own company policies (keeping in mind the country’s labor laws) which fit their business best.

Hire and termination is based mostly as a function of performance.

In case of termination, there is no such standard process. However, for people who have crossed their probation period and have been confirmed, the notice period is of 30-90 days. Generally, with mutual agreement an employee can leave earlier depending on work impact. Also, there are strong laws against sexual harassment at the workplace and companies need to comply with POSH laws.

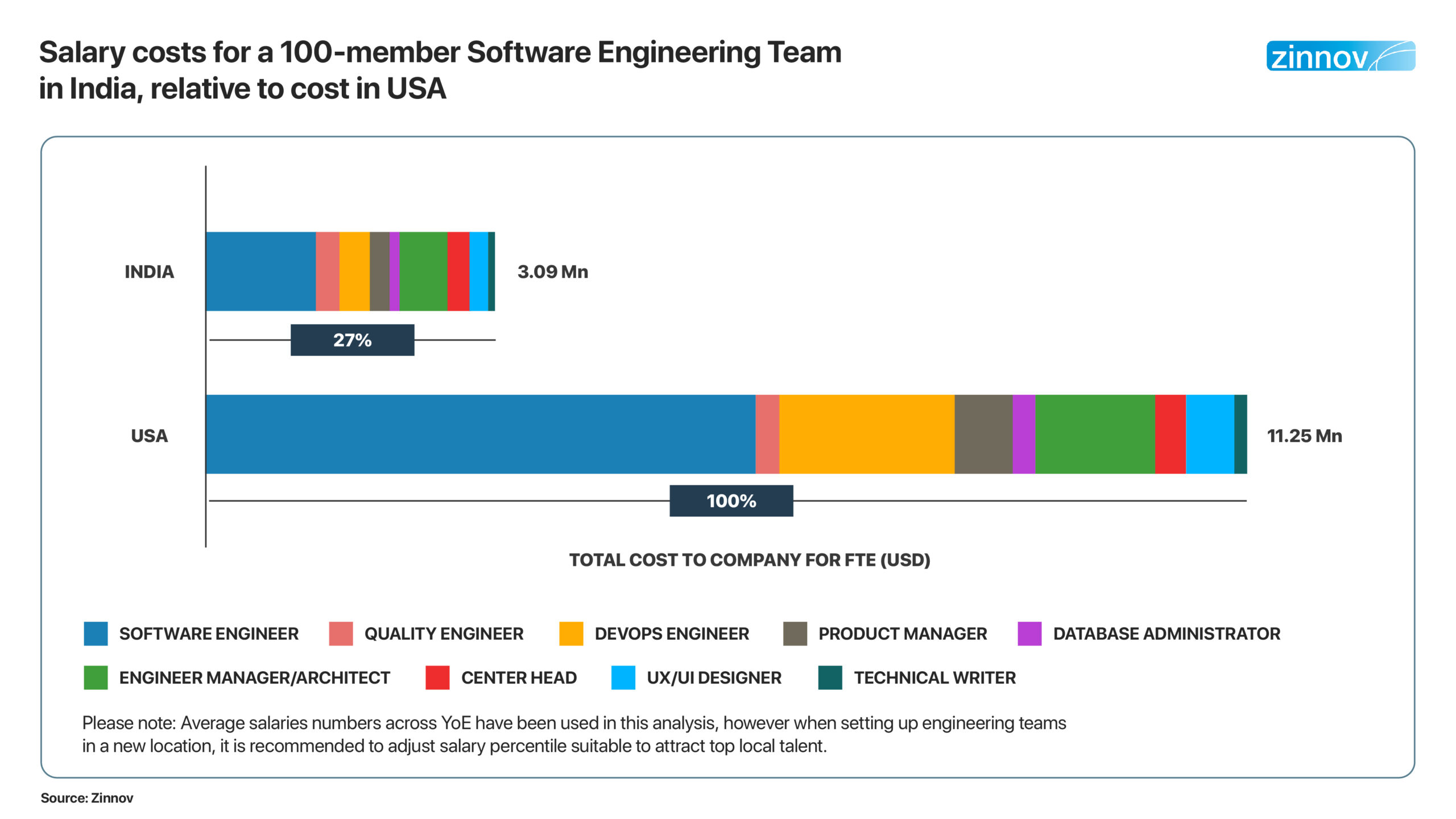

One of the main reasons for most HQ leaders to consider India as their global center location is talent affordability.

While the above illustration is a sample size of 100 members, it reflects the cost-per-hire component when sustaining a team, which is the least compared to the U.S. This affordability quotient makes room for a large digitally skilled core team, with enhanced employee motivation levels throughout the year.

India has the cheapest tariff for Internet data (USD 0.26/GB) compared to the world average of USD 8/GB, enabling an uninterrupted workflow and internet connectivity with the headquarters, and offshore locations.

Even though the real-estate rates keep fluctuating, the build-out cost of offices in India is at an all-time low, with an estimated USD 50/ sq. foot, followed by the Philippines and Mexico.

If an organization desires to have a plug-and-play option, memberships with coworking spaces, like WeWork would cost an average of USD 250/month for 1 person compared to the US that has an average cost of USD 918/month, depending on the location.

Arriving at a specific location is an important exercise, which depends on having access to a mature ecosystem and a large talent pool that is affordable while ranking higher on the Ease of Doing Business index.

As businesses evolve to stay relevant, innovative, and competitive, it is crucial for organizations to quickly and efficiently optimize their resources to help sustain any future disruptions. GCCs are typically set up to drive innovation, establish expertise, and expand to get access to global markets and talent.

Global Innovation Centers, also known as Global In-house Centers, are offshore facilities owned and operated by the enterprise for sourcing IT and business services that support the business. In general, GICs are used to foster innovation, develop expertise, and expand globally to gain access to talent and markets.

India’s knowledge-driven workforce, booming infrastructure, conducive government initiatives, academic capabilities, and talent availability have put the subcontinent on the global radar. These, along with vibrant start-up and Service Provider ecosystems, have helped it remain one of the most attractive destinations for Global Capability Centers.