Over the past few years, Digital Engineering Service Providers have been attracting significant investments from Private Equity (PE) firms across the globe. The growing maturity of traditional IT outsourcing, adoption of digital use cases across multiple industries, increasing complexity and cost of R&D, and access to skilled workforce are some of the many factors that have made these companies critical to the technology ecosystem and have added to the allure of this industry for PEs. Zinnov, over the past two decades, has been strategically positioned to witness the burgeoning of Digital Engineering, which has flourished under the shadow of the larger IT services industry.

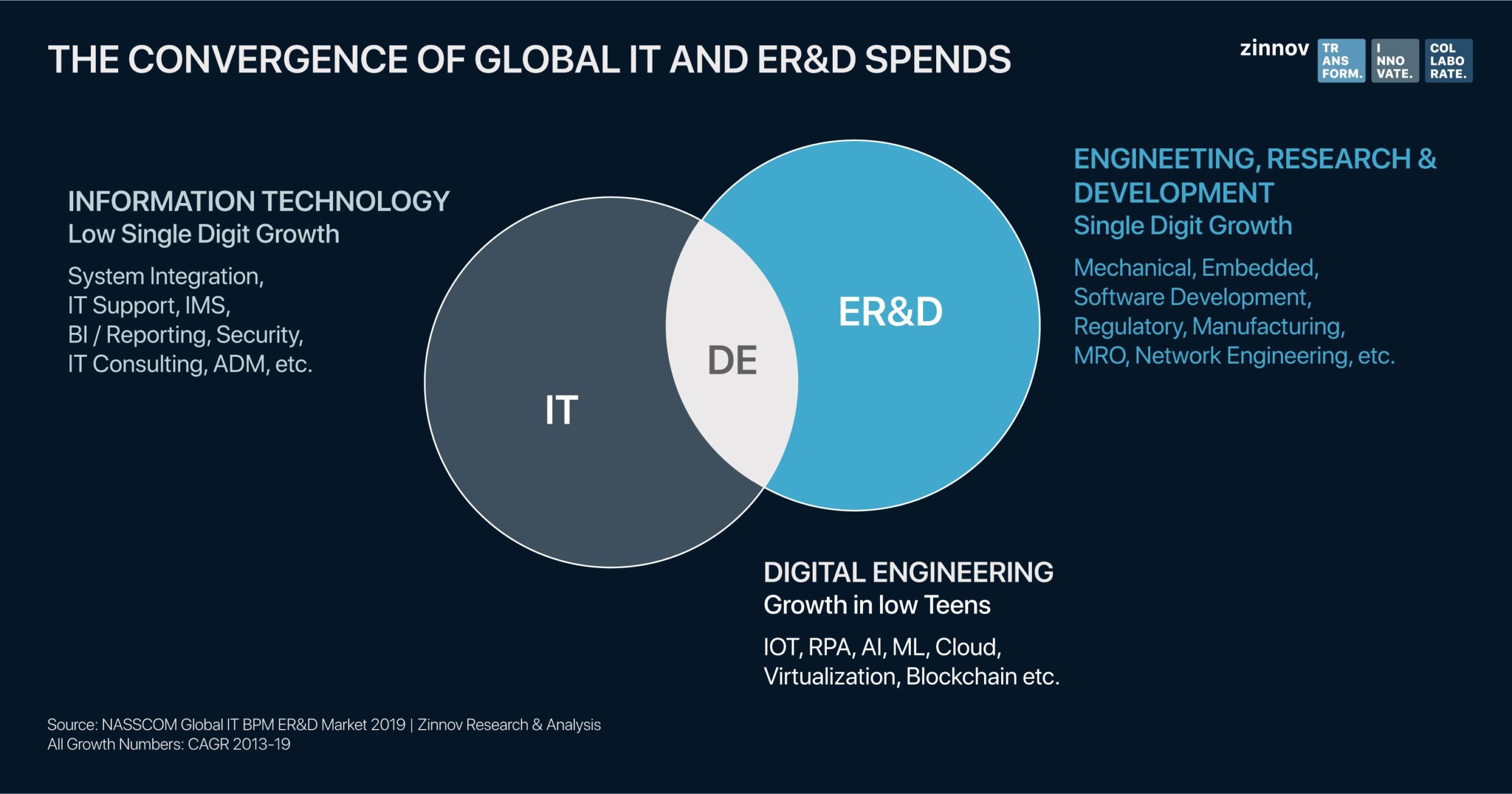

The increasing adoption and implementation of digital technologies has resulted in a convergence of IT and ER&D spends by companies, which is further driven by the race to become leaders in their digitally transformed industries. Disruption by tech giants such as GAFAM (Google, Amazon, Facebook, Apple, Microsoft) across industries has forced conventional players to increase their spend on digital initiatives to maintain a competitive advantage. The meteoric growth of Software & Internet giants (BAT – Baidu, Alibaba, Tencent, and GAFAM) has been the driving factor behind the fast-growing geographies such as the US and China. Our analysis of spend on IT, ER&D, and Digital Engineering adds further color to this evolving picture. Between 2013 and 2019 the spend on IT and ER&D across industries has grown in low single digits while during the same time, the spend on Digital Engineering has grown at over 12-13%.

With higher outsourcing growth, more resilient spending, and the fragmented structure of the ER&D space, traditional IT firms like Capgemini (which acquired Altran) and Accenture (Industry X.0) are actively pursuing Digital Engineering. Other forward-looking Service Providers too have been quick to identify the opportunities in Digital Engineering services and have ramped up their capabilities and offerings, and built business models that cater to the evolving needs of their customers. The focus has been on deploying new offerings that enable their customers in building new technology infrastructure, accelerating product development, enhancing ownership experience, creating new revenue streams, and/or facilitating efficient processes and quality control.

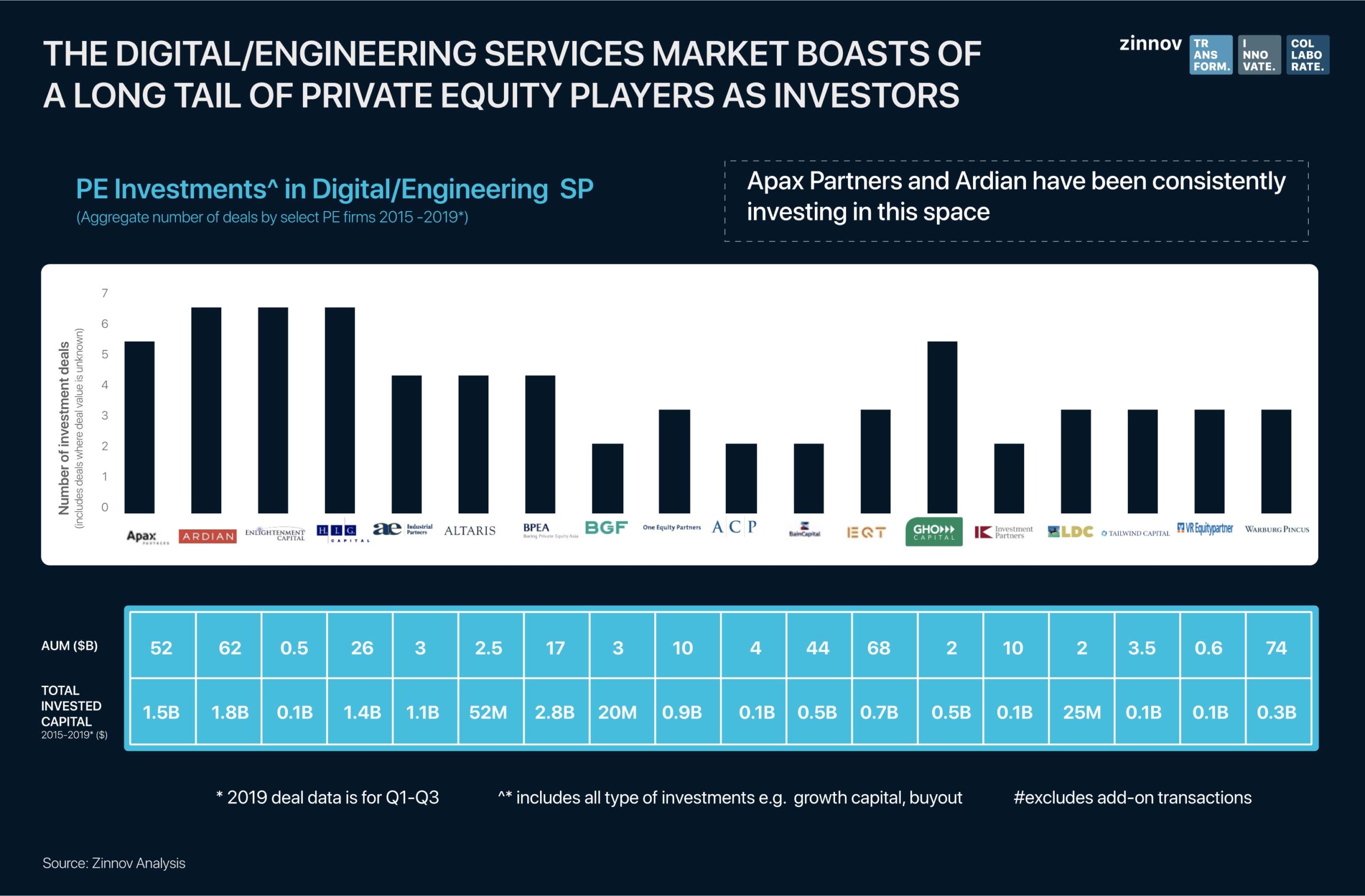

Competition has also increased M&A activity to consolidate the market, with the fast-growing Digital Engineering space accounting for 40% of all M&A transactions in 2019. The market, still in a high-growth phase, presents a considerable headroom for growth with a long tail of large and mid-sized Service Providers ripe to take the plunge into Digital Engineering over the next few years, making this a lucrative sector for investors. However, the recent economic slowdown, accelerated by COVID-19, has created an air of uncertainty within the industry and has significantly impacted the revenue forecasts and growth thesis of all Service Providers.

COVID-19 has had a multifold impact on the Services industry. While enabling remote working for millions of employees, access to infrastructure and hiring have been challenging for companies; loss of key accounts, delays and cancellations in upcoming projects, and widespread layoffs have severely impacted top-line growth and cash flow projections. This has negatively impacted valuation multiples of services assets across the board, making them a lot more palatable for investors. This may present a rare opportunity for the intrepid investors who believe they possess the necessary ammunition to help these assets weather the current storm and outdo the competition in the post-pandemic world. However, a deeper look needs to be taken into the DNA of these Digital Engineering assets, taking into consideration the several complexities that might impact the company performance going forward.

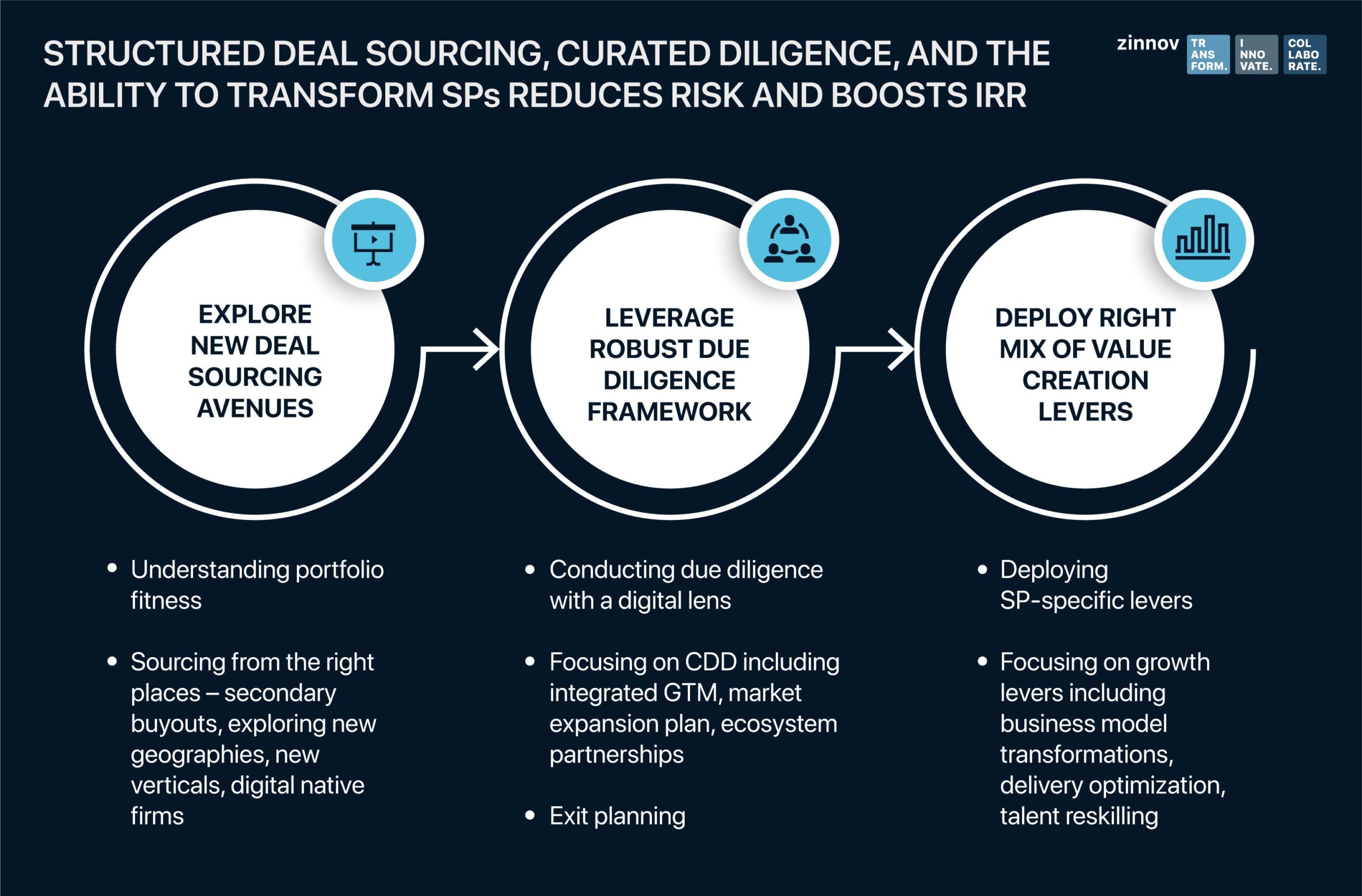

Over the past decade, Zinnov has worked with numerous PE firms and Strategic Investors on some of the marquee transactions in this space, and unsurprisingly, the fundamentals that have been critical in driving valuations of assets have predominantly remained the same.

While these factors have been highly effective in the past and will still be important for investors going forward, evaluation of the ultimate value and growth prospects of an asset will need to go above and beyond this simplistic view. Even pre-pandemic, we have witnessed frequent instances where investors have bought into companies that have fit the aforementioned criteria but have failed to garner expected returns and/or are facing challenges in exiting their investments – significantly impacting their Internal Rate of Return (IRR).

In the past, Zinnov has conducted extensive research on identifying value creation levers for Digital Engineering services companies, helping our PE partners create an informed investment thesis. Here, we have explored a few key nuances of the industry that investors need to delve into while evaluating their next investment in the Digital Engineering services market, especially in the wake of the pandemic.

Size of the market, headroom, revenue growth, profit margins, competition, etc., are metrics and sanity checks that continue to be critical in providing adequate color on a company’s performance. However, to evaluate the stability of the business, potential for growth and the plan for a favorable exit, a deeper understanding needs to be built across multiple fronts. PE firms in the past have had challenges building the necessary deep domain expertise to evaluate these opportunities. In fact, even PE firms with decades of experience investing in services assets too, have borne some bad apples due to the underlying complexity of the businesses.

Over our two decades of experience working with numerous digital services players, we have rarely come across two companies that have been ‘similar’ to each other in this industry. Vertical mix, delivery models, geographical split, engagement models, internal R&D, and a lot of other factors differentiate these assets, and investors need to be cognizant of the challenges in evaluating them.

Here’s a definitive checklist that can guide investors in assessing the assets –

The impact of COVID-19 on the industry verticals has varied greatly. Plummeting demand and travel restrictions have had an unparalleled impact on the Aerospace and Automotive industries. Companies in the Enterprise & Consumer Software, Telecommunications, and Semiconductor industries have seen muted impact. The economic downturn has further impacted revenues for the consumer industries such as FMCG, Retail, and Consumer Electronics. Therefore, Service Providers’ revenues and deal pipelines have been impacted proportionally, according to their exposure to these verticals. A diversified vertical mix, with a presence in stable accounts, is a great sign for a healthy asset.

The current Digital Engineering spend is disproportionately split across the world, with a high concentration in North America. As the impact of the pandemic plays out across geographies, having delivery capabilities in low-cost offshore locations and customers in high spending geographies such as North America has become critical for Service Providers.

Intellectual Property, Platforms, and Vertical Solutions built in-house or through partnerships will augment traditional offerings and will put services companies in good stead to win new and higher-value business. In the midst of the pandemic, the Service Providers who have been able to win newer deals have been able to do so by leveraging solutions that have helped their customers solve key, specific problems.

A healthy onsite and offshore mix has been key to driving higher margins for Service Providers. Major retrenchments across highly impacted verticals and a hold on staffing-based deals have made an assessment of delivery capabilities critical to investment success.

In the recent past, we have seen multiple PE firms leverage this lever to achieve rapid top-line growth. The presence of senior sales personnel with expertise and industry relationships in critical geographies and close to marquee accounts go a long way in unlocking growth. Although, in the short term, as traditional sales channels become redundant due to the pandemic, Service Providers that enable effective remote sales through video conferencing, webinars, chatbots, etc., will be better off. In fact, Digital Engineering Service Providers have continued to grow and onboard new customers even in the midst of the pandemic by leveraging these channels.

The Digital Engineering services industry, over the past few years, has evidently witnessed an increasing consolidation, which is expected to accelerate in the post-pandemic era. Companies will need to build the ability to acquire and integrate companies to target key accounts, increase vertical presence, enhance capabilities, and expand delivery footprint.

Service Providers who have room to create long-term cost efficiencies and the financial agility to leverage newer models around IP monetization or outcome-based models will fare better compared to their peer group.

As the deal activity begins to resurge after a brief lull, a lot will have fundamentally changed in the services industry. If the previous economic downturns are anything to go by, a multitude of assets will swarm the markets looking for a cash injection to survive, grow, or acquire. Investors too will be itching to maximize the value for the assets they wager on or currently hold. We believe that the Service Providers who do well in the success factors outlined above and PE firms that are able to incisively maneuver these levers will be able to generate significant value over the next few years.