|

|

Private Equity (PE) firms have made bold moves in Automation, completing nearly 70 strategic acquisitions as of August 2024. With Private Equity investment in Automation increasing, understanding nuanced investment and turnaround strategies becomes not just beneficial but essential. These strategies enable PE firms to pinpoint high-potential opportunities, optimize operations, and ultimately drive substantial value creation within their portfolios. Leveraging insights from past successes and industry trends, strategic guidance is crucial for navigating and capitalizing on emerging investment opportunities.

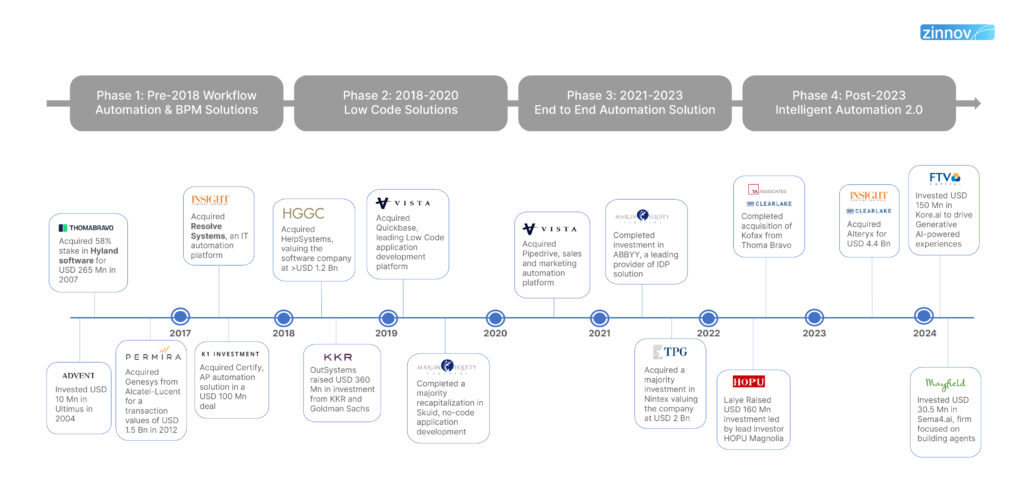

Initially, PE firms concentrated their efforts on platforms that provided Workflow Automation solutions to streamline processes. However, as new technologies like Low-Code platforms emerged, investors shifted their focus. This change highlighted how PE firms are adapting their strategies to align with tech advances, revealing an evolving investment pattern worth examining further.

Private Equity firms ventured into Automation Solutions by targeting the Workflow Automation and BPM space. These investments were driven by several compelling factors:

The next wave of Private Equity investment in Automation had been predominantly driven by Low-code/No-code (LC/NC) solutions, with ~50% of transactions in the Automation sector targeting these technologies. The key factors influencing these investments included:

As Intelligent Automation platforms continuously evolved to integrate various technologies, they positioned themselves as comprehensive end-to-end solution providers. This shift attracted significant Private Equity investments for several key reasons:

The future of Automation is being shaped by the convergence of Intelligent Automation technologies and Generative AI. This integration marks the emergence of Intelligent Automation 2.0, a new paradigm where systems are not only automated but are also capable of self-learning and evolving. Investments in companies like Kore.ai, Hebbia, Creatio, and Sema4.ai reflect PE firms’ recognition of the transformative potential of Generative AI in driving the next wave of growth.

There are various benefits organizations can reap from Intelligent Automation 2.0, that are powered by Generative AI. These benefits include:

Building on this trend, Private Equity firms are increasingly likely to invest in companies that are at the forefront of integrating Generative AI with Intelligent Automation. By channeling capital into these innovative Enterprises, Private Equity firms are positioning themselves to capitalize on the substantial efficiencies and competitive advantages that this next wave of Automation promises to deliver.

When Private Equity firms acquire a company, they often take a focused approach to turning things around. This usually means putting together an internal team dedicated to improving the company’s operations, increasing its value, and driving revenue growth. They achieve this by leveraging targeted strategies and innovations, particularly in the Automation space, to boost the company’s performance and market standing.

We conducted a detailed analysis of the turnaround strategies that Private Equity firms implemented during their acquisitions in Phase 3 and Phase 4, aiming to pinpoint and highlight the key approaches utilized by these firms over the past four years. These turnaround strategies included Legacy Modernization, Verticalization of Stack, Mid-Market Pursuit, and the Pivot to Generative AI.

The strategic focus of Private Equity investment in Automation was on guiding Automation Platforms toward modernizing older systems to meet market demands, often by migrating enterprise legacy solutions to the Cloud. This strategy was historically used because most Enterprises were relying on legacy products. Clearlake’s acquisition of Tungsten Automation (formerly Kofax) exemplifies this strategy. Following the Kofax acquisition, Clearlake strategically integrated companies like Printix and PsiGen, offering Cloud Print, Document Security, and Content Management Solutions. They then acquired Tungsten, specializing in Cloud Invoicing and AP automation, to create a fully modernized platform.

Given that most companies have now transitioned to Cloud-based operations, this strategy has lost much of its allure for Private Equity firms. As a result, it has seen diminished traction and is currently not being actively pursued by them.

This strategy centers on developing niche, vertical-specific solutions to enhance a broader platform, ensuring customized functionality for specialized industries. Vista acquired Quickbase to transform it into a vertically oriented company, further purchasing MCF Technology Solutions to infuse a variety of industry-tailored application templates into the Quickbase platform, thus increasing its adaptability and relevance to diverse sectoral requirements. Additionally, they invested in an Enablement Services program to foster co-innovation with clients, provide training and certification, and offer robust support through the Quickbase expert team.

Private Equity firms are increasingly targeting the mid-market sector, recognizing its potential for longer-term growth opportunities. By focusing on companies that provide solutions tailored to the mid-market, these firms leverage the sector’s extensive, untapped potential, aiming to unlock value in areas often overlooked by larger investors. TPG’s acquisition of Nintex is a testament to this strategy, as Nintex focuses on enhancing ROI, cost efficiency, and productivity, making it highly appealing to the mid-market. Numerous case studies demonstrate the success of this approach, explaining its strong appeal to a wide range of stakeholders

This strategy is focusing on harnessing the transformative power of Generative AI to redefine product offerings and operational capabilities within companies. FTV Capital’s investment in Kore.ai serves as a prime example of this strategic pivot. Post its acquisition, Kore.ai has launched GALE, a Generative AI application platform that facilitates the rapid development and deployment of advanced AI applications, scaling them to meet Enterprise demands.

As we advance into this era of Intelligent Automation 2.0, the Automation landscape will undergo a profound transformation:

With strategic insight, Private Equity firms are poised to lead the evolution of Intelligent Automation 2.0, capitalizing on its transformative potential to drive the next phase of innovation. By aligning with the forefront of Automation innovation, they will not only keep pace with technological progress but also actively shape the future of digital transformation.

Zinnov boasts a robust network in the intelligent automation sector and has supported numerous private equity firms in developing their investment theses and facilitating transactions. If you are a PE firm looking to invest in the space and wish to have a discussion, please reach out to us at info@zinnov.com to connect with our experts!