|

|

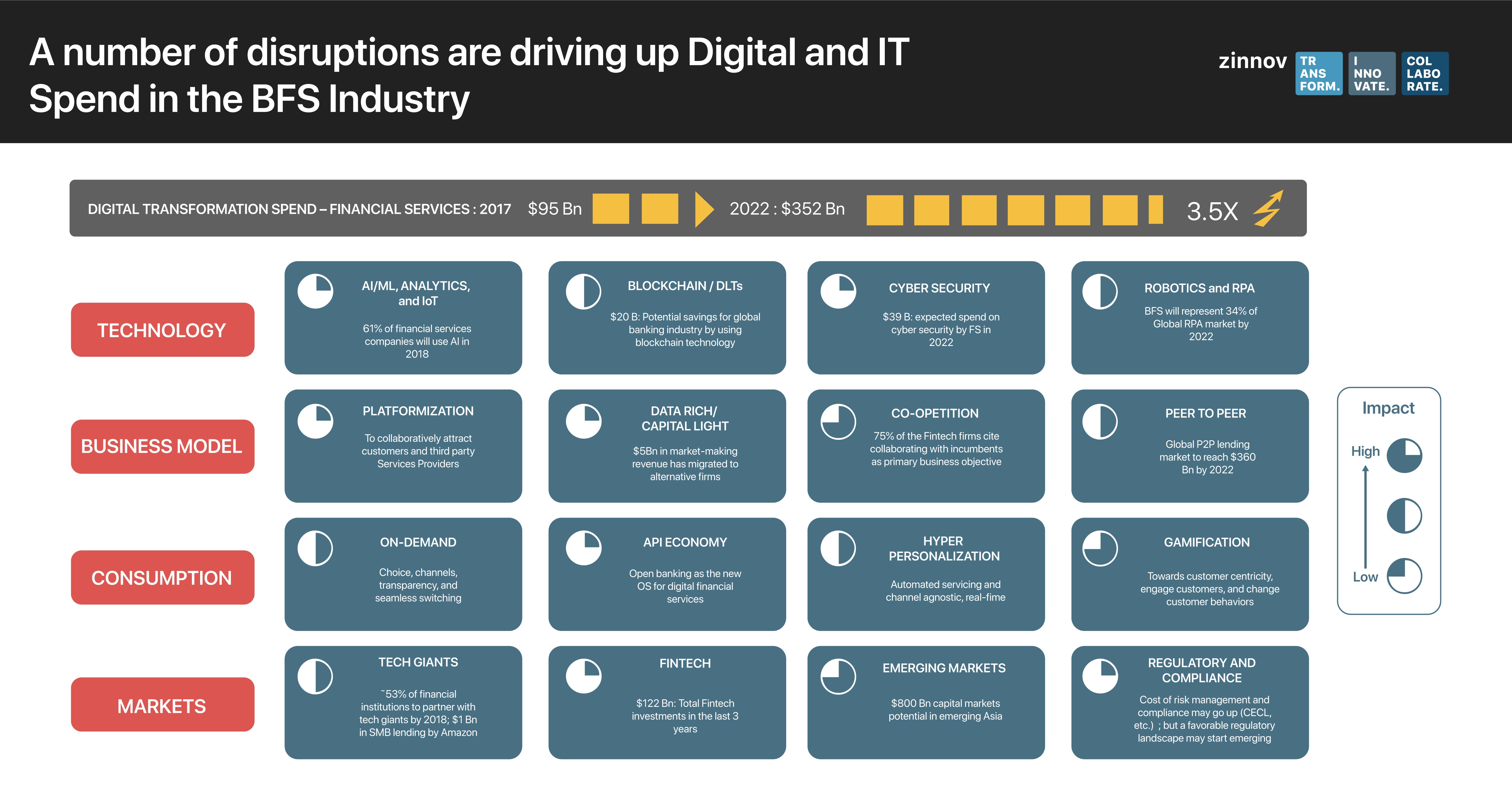

Digital disruptions have become the norm, regardless of verticals. The Banking and Financial Services (BFS) space is also in a state of flux, because of the disruptions happening in BFS companies across multiple fronts. BFS companies are being redefined across business models, technology, consumption patterns, markets, talent, etc., to keep pace with the proliferation of new-age payment methods, alternative lending mechanisms, automated solutions, capital market integration, etc. On a macro level, changes such as increasing wealth inequality, declining net worth, globalization, regulatory changes, emerging market growth, and societal and demographic changes are pushing the performance bar even higher for BFS companies.

The above-mentioned disruptions aren’t happening in isolation, but new-age digital technologies such as AI/ML, RPA, Blockchain, IOT, and Advanced Analytics are at their core. Not only are these disruptive technologies transforming the playing field for banks and financial services companies, but they are also bringing a whole new world of start-ups to compete and disrupt business as usual. This is making the BFS companies sit up and take note of the changes happening currently, while also reinforcing the need for investing in building digital capabilities within the organization.

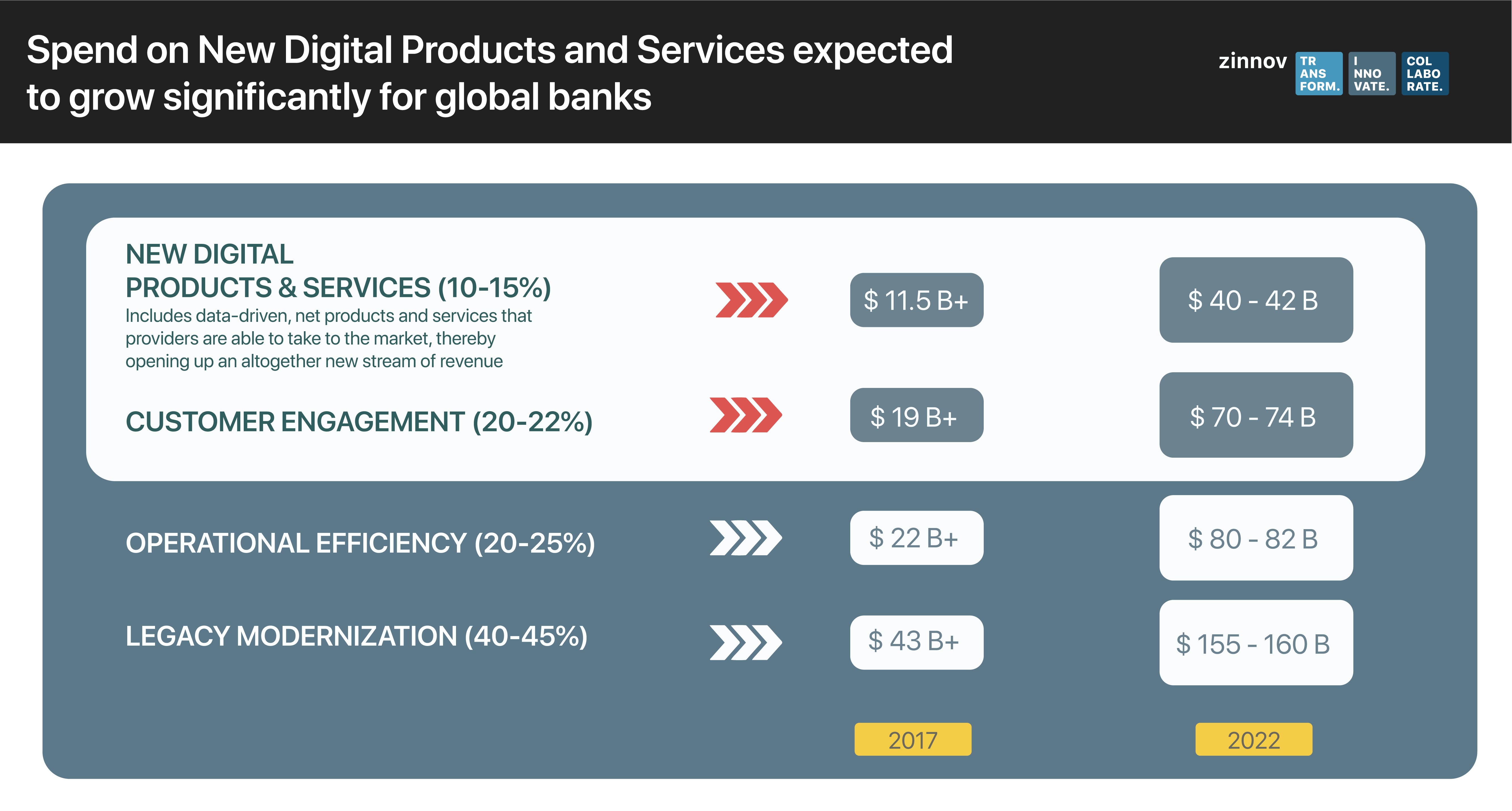

The digital and IT spend being made in BFS companies is a testament to the importance of digital transformation. In fact, a Zinnov analysis pegs the digital transformation spend in BFS companies to touch a staggering USD 352Bn by 2022, witnessing a massive 3x increase from 2018.

Banking majors are leveraging digital technologies to create differentiation through newer products and solutions. These newer products and services are expected to generate newer revenue streams besides Opex and Capex advantages. The Zinnov study revealed that 10-15% of the digital spend in banks and financial services companies is being deployed towards developing newer products and services, while 20-22% is being invested in enhancing customer service. For this, BFS companies building digital capabilities in IOT, AI/ML, RPA, Blockchain/DLTs, Analytics, etc.

The traditional business models adopted by BFS companies no longer suffice if they are to compete with newer players in the space like fintech start-ups and tech giants. The BFS space is increasingly witnessing the blurring of lines between industry verticals with every kind of company trying to partake in the pie that is BFS. Hence, companies are exploring newer business models and strategies like platformization, strategic M&A, co-optition, peer-to-peer lending, etc., to differentiate themselves to the increasingly demanding customer of today.

Customer experience is at the core of any innovation – be it a product or a service – in BFS companies. Banking majors are exploring multiple customer-centric digital strategies focusing on mobile-first, digital everything, and multi-channel delivery of products and services geared towards enhancing customer experience. Further, hyper-personalization through automated servicing and real-time, channel-agnostic services, as well as on-demand services across channels with seamless switching is helping BFS companies to provide differentiated customer experience. Some companies are even exploring gamification to engage with customers and change customer behaviors.

On the regulatory front, banks are being forced to spend heavily on technology to stay compliant. This includes the regulations that bubbled up in the aftermath of the 2008 global financial crisis to newer regulatory changes like European Union’s GDPR (General Data Protection Regulation), CECL (Current Expected Credit Losses) by FASB, CCAR (Capital and Comprehensive Capital Analysis and Review), MiFID II, etc.

In fact, Regulatory Technology – RegTech as it is popularly known as – is used to be a minor expense item for banks. However, due to the newer regulatory changes and compliance issues, RegTech spend has become a significant component of banks’ overall spend. It has a critical role to play with evolving applications such as Surveillance and Monitoring, Customer Identification, AML Compliance, Reporting, and Risk Management. BFS companies are reimagining their technology spending in favor of RegTech to stay compliant.

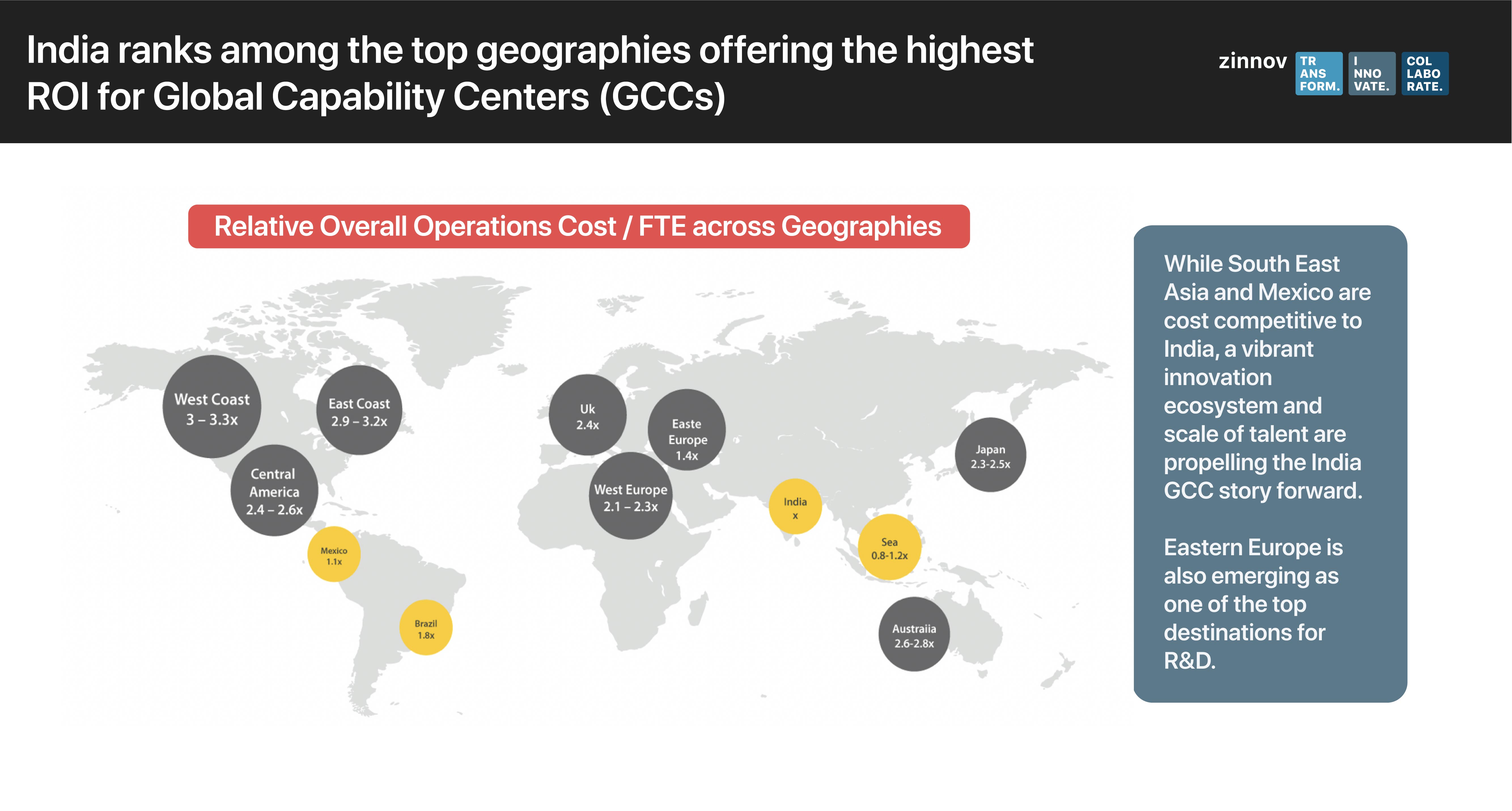

One of the biggest hindrances for global banks to successfully drive their digital transformation agendas is the scarcity of skilled digital talent. In fact, talent scarcity has been a consistent thorn in the side for tech giants and start-ups alike. This is evidenced by the fact that Google, Microsoft, Amazon have large Global Capability Centers (GCCs) in geographies like India and have been doubling down on these GCCs to tap into the available large talent pool in new emerging digital tech.

Given the stringent regulations and the sensitive nature of data that global banks deal with on a daily basis, setting up IT GCCs in emerging geographies like India seems like their go-to strategy. India has become a favored destination for global BFS companies to set up their IT GCCs, thanks in major part to the availability of a huge talent pool. Every year, close to a million engineers graduate from campuses around the subcontinent. Additionally, India ranks among the top geographies offering the highest return on investment (ROI) for GCCs. Although Mexico and other countries in South East Asia are cost-competitive to India, the vibrant innovation ecosystem and the scale of available talent have propelled India to the top of the globalization chart.

While global BFS companies are facing a severe deficit of skilled digital talent, India could very well be their golden ticket to success. Given India’s skilled talent pocket, it is well-positioned to drive the digital strategies internally. Furthermore, nearly 60% of banking GCCs in India have a US-headquartered parent, where the talent scarcity is acute. Moreover, banking majors like JP Morgan Chase, Standard Chartered, Société Générale, Morgan Stanley, Goldman Sachs, et al not only have mature GCCs in India, but are also strengthening their presence by expanding their footprint in terms of headcount in multiple cities as well as focusing on core work involving Advanced Analytics, AI/ML, RPA, and cutting-edge research.

American banks in the Forbes Global 2000 list have been the earliest movers into India, accounting for nearly 57% of headcount in BFS technology centers. However, only 9% of global banks in the Forbes Global 2000 list have technology centers in India, indicating a massive opportunity for new center setup. With technology centers of global banks in India increasingly focused on building teams on new-age technologies such as AI, Cloud, Blockchain, etc., it is clear that BFS companies don’t want to be laggards in adopting digital technologies to enhance customer experience. Further, with fintech start-ups disrupting every function across the banking value chain, global banks are leaving no stone unturned to keep their competitive edge.

The majority of core work portfolio among BFS technology centers revolves around Payments, Securities Trading, and Post Trade Services. Some of the other lines of business (LoBs) being driven out of India include –

Retail Banking and Payments: Retail Banking has moved far ahead of other LoBs in terms of digital adoption. Further, given the high digital penetration in Retail Banking and Payments, global banks with huge retail banking presence are focusing on building digital banking products out of their India GCCs. On the Payments side, as more and more fintech start-ups disrupt Payments, banks are in a race to constantly make payments customer-friendly. Global banks such as HSBC, Citi, Deutsche Bank, etc., have large teams working on Payments.

Corporate & Investment Banking: This LoB is still playing catch up in terms of digital transformation and is slowly building analytics on top of their existing platforms. Further, electronic trading platforms are of importance for banks. And as data from non-traditional sources gains traction, regularly updating these platforms gives banks a competitive edge in market-making activity.

Cybersecurity & Risk Management: Among the enabling technology teams, Cybersecurity & Risk Management, as well as Infrastructure & IT Support teams constitute the biggest headcounts and support across LoBs. In fact, banks operating in the Investment Banking space have large teams working on Market Risk. The roughly 35% of BFS GCC budget that goes into strengthening Cybersecurity and Internal Security Platforms underscores the criticality of this LoB for global banks.

It is clear that the BFS space is in a state of flux. But BFS GCCs have the unique opportunity to showcase their capabilities by driving digital strategies from India, thanks to the exceptional combination of factors such as talent pool, mature GCCs, and a vibrant start-up ecosystem. However, BFS GCCs need to rethink their value proposition to transform themselves into true value creators instead of mere cost centers. Hence, the GCCs need to chart a robust core vs context strategy, set up digital Centers of Excellence (COEs), explore the open innovation paradigm by collaborating with universities, research labs, and start-ups, and foster a platform/product-first mindset in the organizational culture to drive this transformation ahead.