|

|

The last 3 years have been a wild roller coaster ride for the world, including the India Global Capability Centers (GCCs) ecosystem. The COVID-19 pandemic heightened tensions between the US and China, with the Western world realizing China’s strength, which the latter demonstrated by flexing its muscles considerably. This, in turn, put pressure on companies to reduce their reliance on China and explore alternatives.

Hot on the heels of the pandemic, the Russia-Ukraine war erupted. Before the war, Eastern Europe was one of the fastest-growing technology hubs in the world. The sudden onset of the war forced companies to reduce their reliance on Eastern Europe.

Post the pandemic, the economy grew at a rate faster than expected, igniting an unprecedented war for talent – the likes of which we had never seen before. And talent is at the core of companies turbocharging the growth of their Global Capability Centers (GCCs).

Now, we find ourselves amid an economic slowdown, and in some countries, even a recession. This situation requires companies to reduce costs while continuing to invest in digital technologies, especially with the advent of new technologies such as Generative AI.

But what has been consistent throughout these turbulent times, is that India has been a clutch player through and through, and continues to be one, in the future as well. For the uninitiated, the term ‘clutch player’ is a sports metaphor, which refers to a person who comes through for the team when needed the most.

The country’s vast pool of skilled talent, coupled with its cost-effectiveness and growing digital infrastructure, has made it an attractive destination for businesses worldwide.

India has undoubtedly been a clutch player for companies over the last few years. Despite employing less than 5% of the talent in India’s organized sector, over 30% of the top employers in India are GCCs. Over 60% of the top STEM graduates join GCCs.

Most of the day zero slots at IITs are reserved for GCCs. GCCs also pay over 20% higher compensation on average, compared to Tech Services companies. However, GCCs should not rest on their laurels and become complacent but continue to push the boundaries of what is possible.

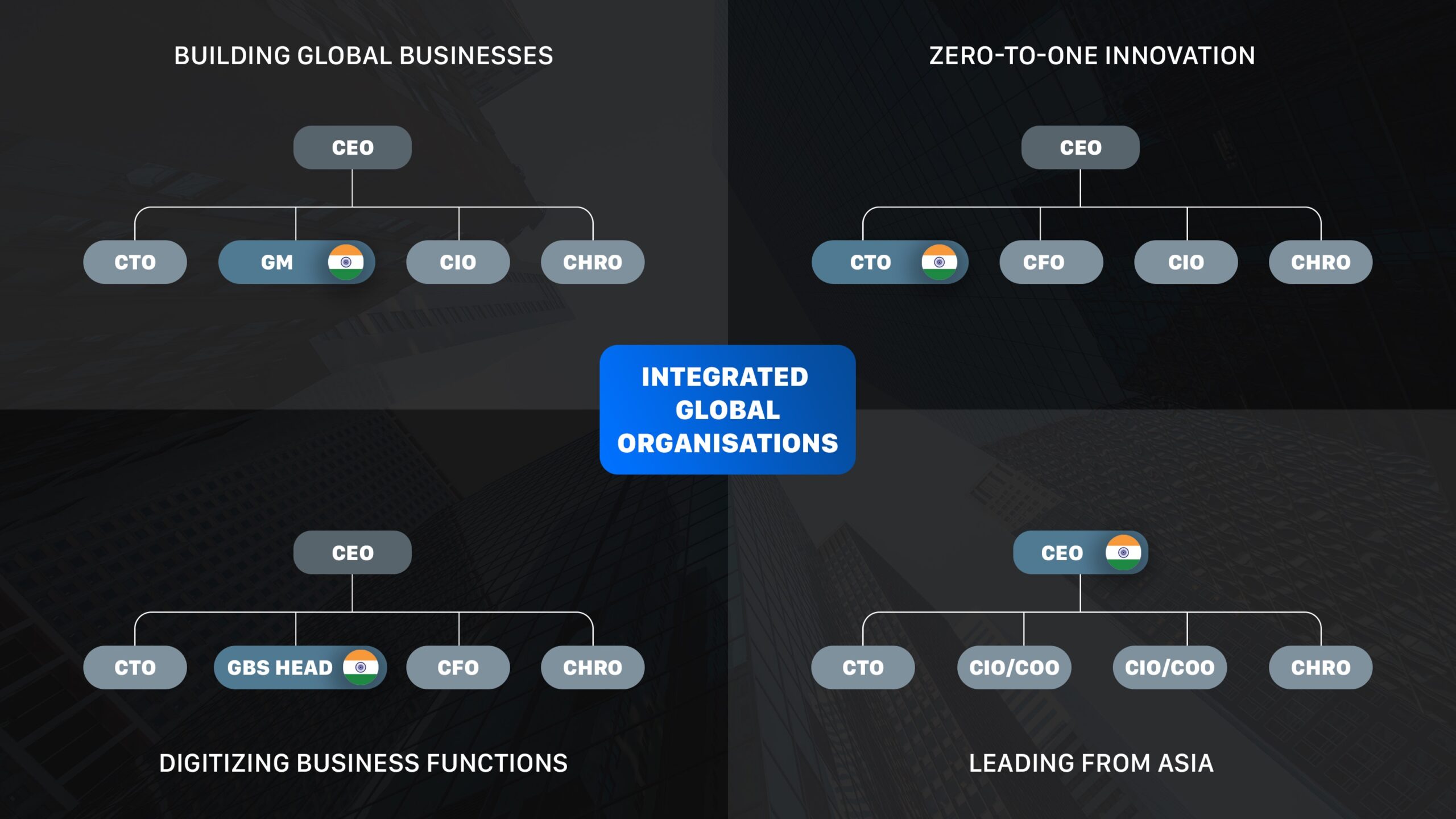

We believe that by 2030, India Global Capability Centers (GCCs) will cease to exist in their current form. Instead, India centers will become integral parts of global organizations, morphing into various models. The India centers will house General Managers of the business, with the primary focus on growing revenues.

Companies such as Citrix already have global General Managers based out of India, with clear P&L responsibilities. Similarly, one of the Automotive tier-I’s General Managers for all their electronic programs is based in India. As we move forward, such roles will become the norm rather than exceptions.

We also believe that many companies will invent their zero-to-one breakthrough innovations from India. With several companies already having strong product and engineering leaders in India, we will soon see more centers becoming hubs of breakthrough innovations. New business functions in the organization will be incubated and scaled in India, making the country a sandbox of breakthrough innovations.

Global Business Services (GBS) has been a major trend across large companies. Focus on customer experience and automation is driving companies to break organizational silos and create frictionless workflows, with GBS becoming the center of such transformations.

Since GBS leadership requires an understanding of cross-functions, the ability to build global delivery capability, and the ability to influence many stakeholders, these roles are a natural fit for leaders based in India.

When companies decide to set up GBS, India will likely become the default leadership location. Scenarios are anticipated where the CEOs of large companies will relocate to India and declare India as the headquarters as their revenues from Asia cross the 50% mark. Schneider’s CEO based out of Hong Kong for a while, and this is just the beginning – more such transitions to India are expected over the next 6-7 years.

The role of the site leader and country manager will undergo a metamorphosis, with new management roles being created. Some will be market orchestrators, helping bring the Asia customers, talent, and the rest of the ecosystem together to help their companies build and sell great products and services.

Some will incubate the next generation of GBS led by technology, where companies will transform into truly autonomous enterprises. Net-new roles will be created, with some leaders focusing purely on newer technologies and others dedicatedly leading their companies and industries to achieve net zero.

There are several key reasons why we are confident that the current GCC model will disappear to make way for an integrated model.

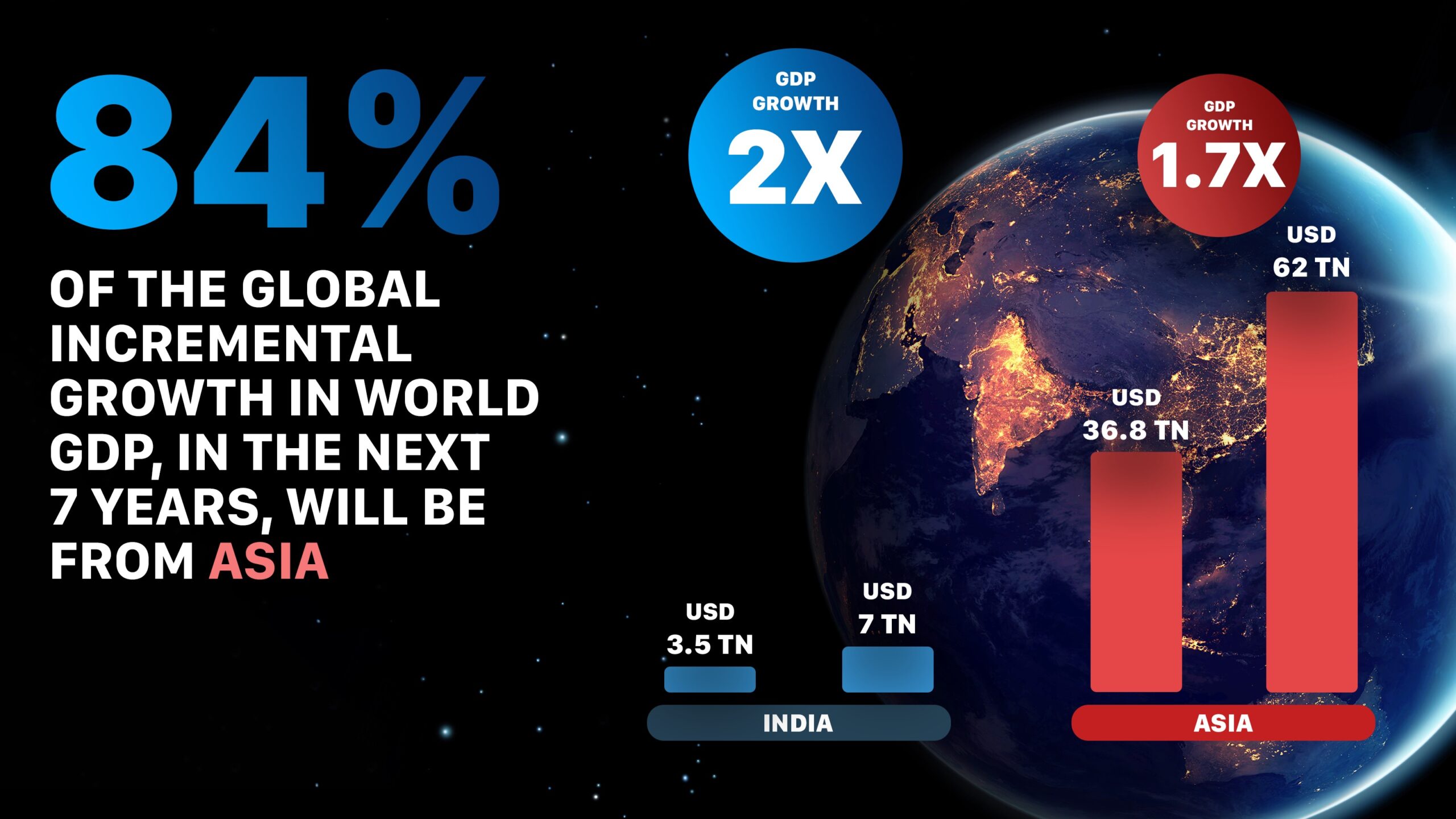

By 2030, Asia will contribute to over 50% of the global GDP, with 84% of the overall net addition to the global GDP coming from Asia. Companies have no choice but to double down on India and China over the next few years.

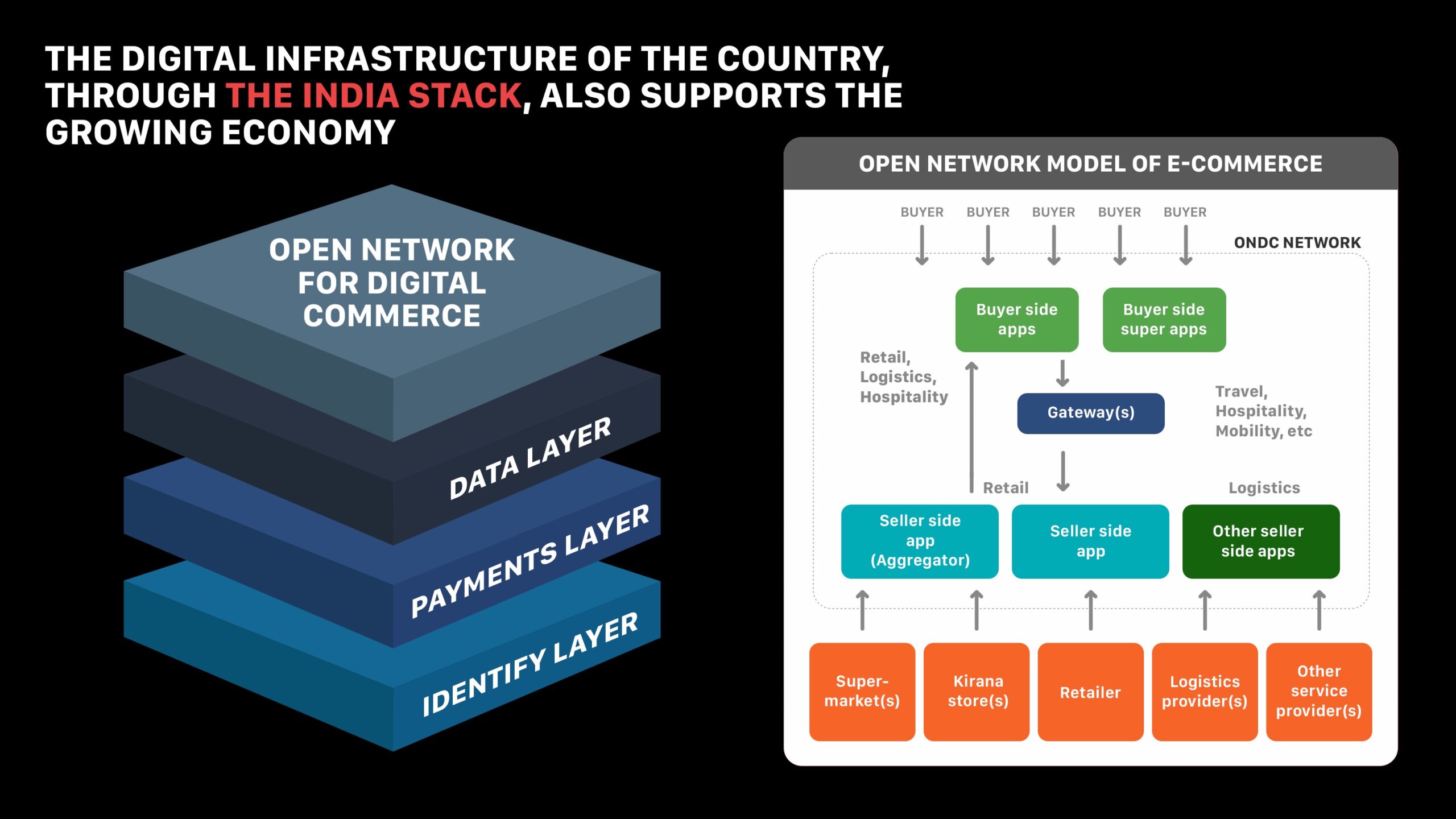

The India Stack is now being exported to other countries, with many sending their teams to India to understand and learn from our success. MOSIP, an open-source initiative by IIIT Bangalore, is allowing countries around the world to implement Aadhar-equivalent systems to provide digital identities to their citizens.

Governments across the globe are now adopting India’s digital transformation model to increase self-reliance, accelerate digital adoption, and make it inclusive.

GCCs and technology services companies have already built deep capabilities in India, across various technologies and business functions.

These are true leaders who adapt to various global cultures. Erin Meyer’s book, The Culture Map, provides a deeper look at the interplay between different cultures.

Take the first row, for example. Low context culture is when the communication doesn’t expect you to have a lot of context about the situation. In this case, the communication is explicit. In high-context communication, a lot is unsaid and you are expected to understand the context.

The communication style in Japan is a case in point. Providing direct feedback is the culture in Germany, versus indirect feedback in Japan. Japan’s decision-making is consensual, whereas in India, it is largely top-down and so on.

Our India Global Capability Centers (GCCs) leaders are versatile and adaptive. When they speak to their peers, counterparts, and bosses in the US, they are explicit in their communication. But when they provide feedback to their teams in India, they sugarcoat it. This is partly cultural, and partly to avoid escalation from HR.

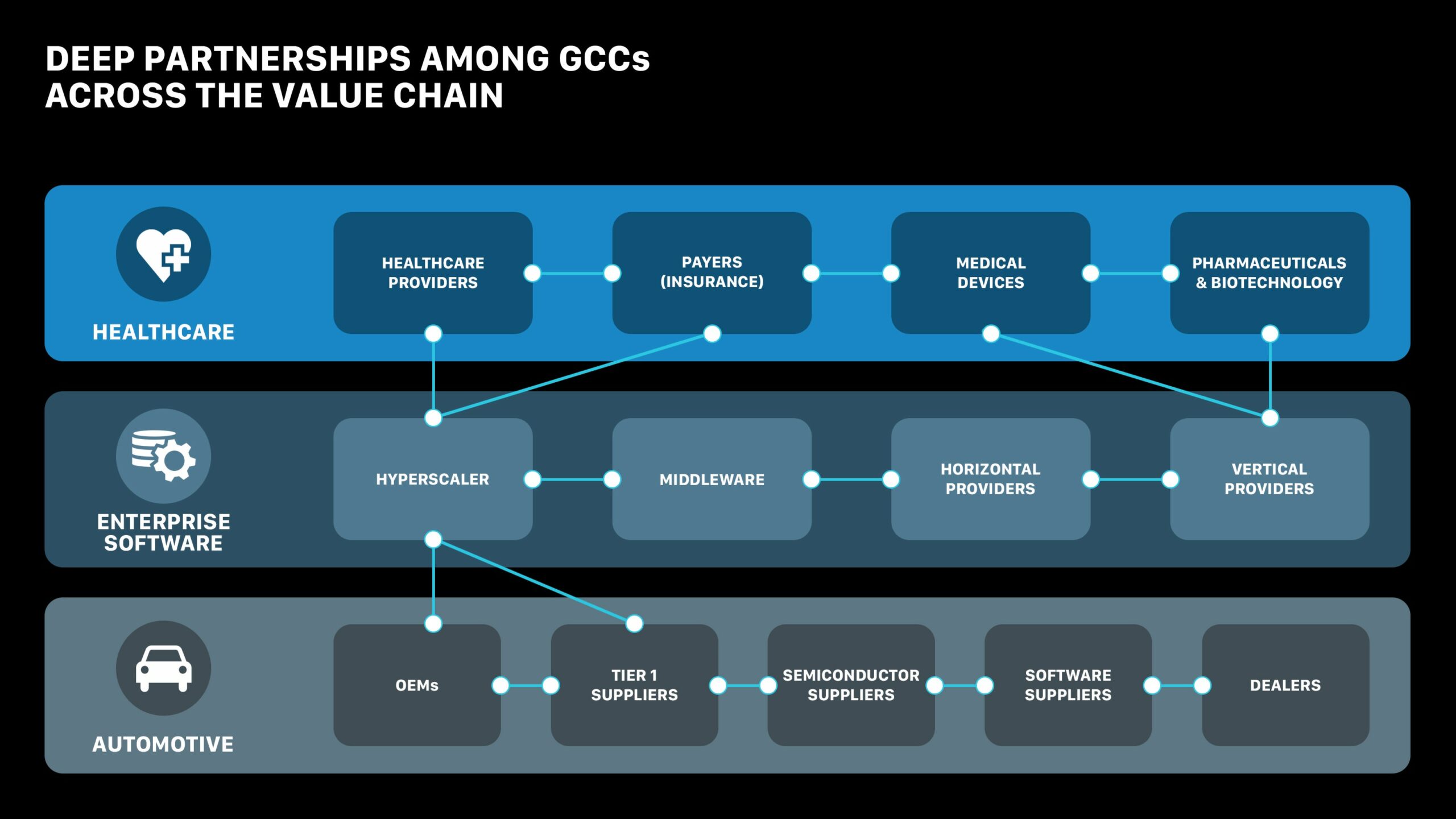

To truly transform the current GCC model, the silos between companies across verticals need to be broken. In this image, we have just plotted three value chains, but this holds true across multiple other verticals.

Companies across the Healthcare value chain, starting from providers such as Providence, payers such as United Health, medical devices companies and pharmaceutical companies such as GE and Regeneron are present in India.

Companies across the Automotive ecosystem, starting from luxury OEMs such as Mercedes-Benz, tier-1 suppliers such as Continental, and chip manufacturers such as Texas Instruments – all have GCCs in India.

Similarly, in the Enterprise Software stack, India houses Hyperscalers, ERP providers, and next-generation experience platforms such as ServiceNow, and vertical and horizontal companies – all have a presence in India.

Though these companies across the value chain closely collaborate in headquarters, their relationship in India is non-existent. The teams that work together in India, often liaise through the headquarters.

If we can create strong relationships and collaboration within India, this will exponentially improve ecosystem capabilities. Some companies have dedicated teams and programs within their GCCs to help them co-innovate with their partners and suppliers. However, this model will bring in exponential outcomes, only when it is adopted universally.

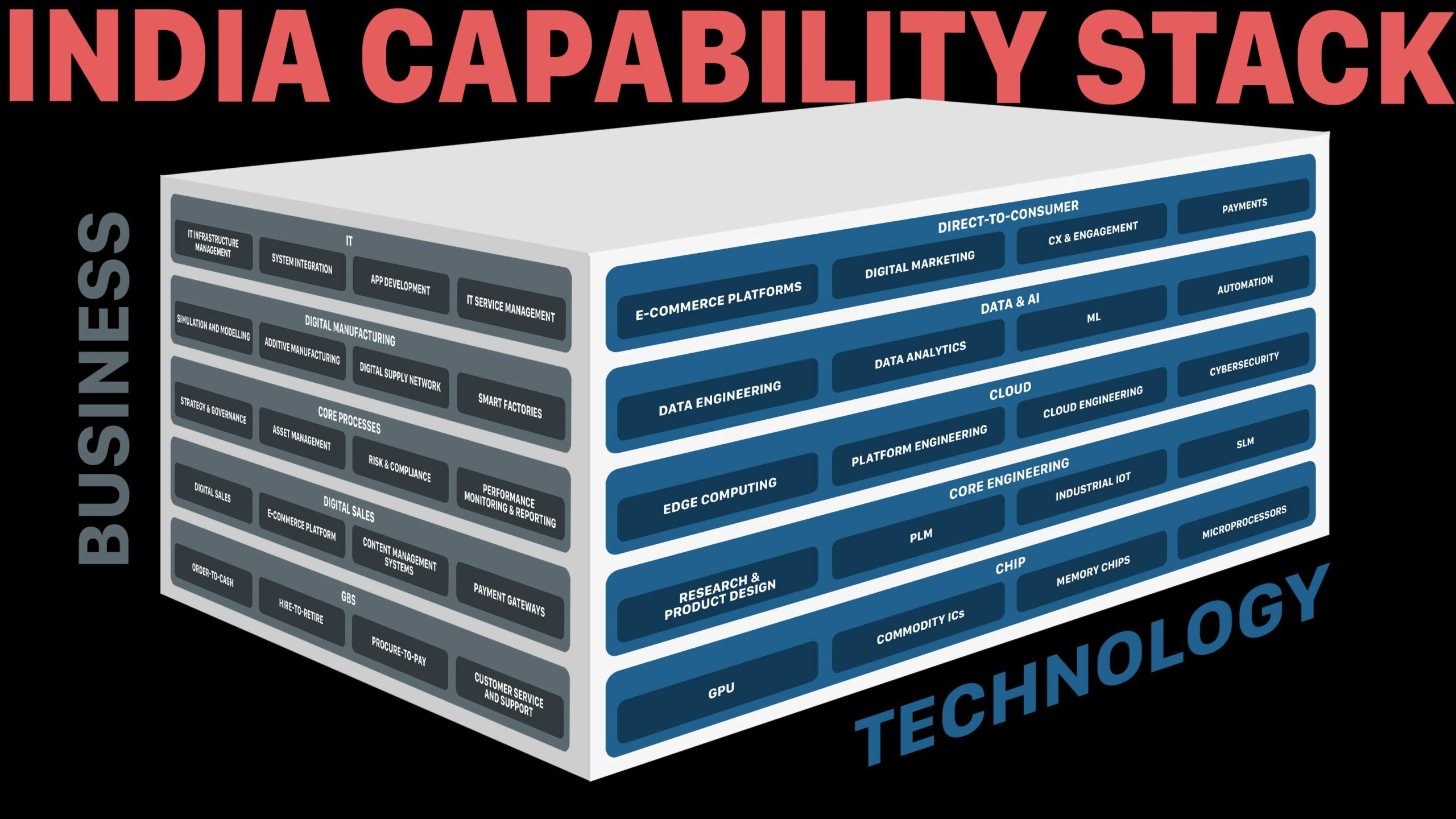

Though the India Capability Stack is strong, it needs to be augmented as we move ahead and transform the current GCC model. India is part of global companies’ China + 1 strategy for manufacturing. We will witness a massive increase in manufacturing exports.

We also have an opportunity to become leaders in sustainability engineering across new material capability, engineering for circularity and sustainability, focusing on both EV and hydrogen and using digital technologies for monitoring and compliance.

One of the biggest augmentations for the India Capability Stack is the abundant talent in India. The biggest complaint about the Indian technology ecosystem is that even though we have close to 2.3 Mn STEM students graduating every year, there is a dearth of experienced engineers.

We need to turn this into our strength by leveraging new AI technologies to augment this vast talent pool. We should transform the traditional apprentice model of training using AI and build our engineers’ domain and business capabilities within a short period.

Top engineers from the top schools in India want to work at GCCs. It is our job to provide them the right opportunities, train them, fight for them, and build an infrastructure to provide them a level playing field. The dreams of such engineers in on our shoulders. We should give them a fighting chance.

As global capability centers evolve and newer GCCs are set up at higher maturity than ever before, it is a matter of time before India GCCs will become true partners of headquarters, or transition into headquarters as such. The vision for 2030 is not only bold, but a definite possibility, if the GCCs play their cards right.