“AI is the runtime that is going to shape all of what we do going forward, in terms of the applications that we build, the platforms that we build, and the infrastructure that we build.”

— Satya Nadella, CEO, Microsoft

If 2024 was about discovering what AI could do, 2025 was about learning what it takes to make AI work at scale.

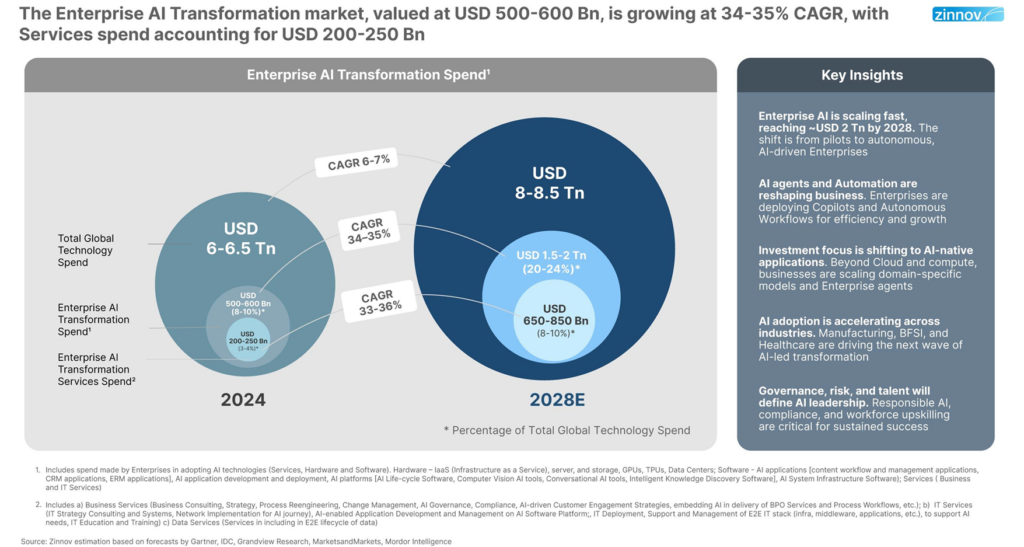

By 2024, enterprise AI transformation spend had reached USD 500–600 billion, setting the stage for accelerated execution through 2025, as highlighted in Zinnov’s Enterprise AI Transformation: The Next USD 200+ Bn Opportunity for Tech Services report. Adoption accelerated across functions and industries. Use cases multiplied. Ambition grew.

Yet, through our work with enterprises, platforms, and service providers over the year, we saw outcomes diverge sharply. Some organizations translated AI momentum into meaningful business results, while others struggled to move beyond early deployments.

The difference did not lie in intent or investment. It lay in how prepared enterprises were to execute. Enterprises that aligned data foundations, business execution, engineering depth, and ecosystem support were able to scale AI with confidence. Where these elements evolved in silos, AI progress slowed.

Looking back, four shifts define how 2025 unfolded and together, they explain what leaders need to focus on as they move into 2026.

The most visible gains in 2025 came from enterprises that stopped treating AI as an overlay and started integrating it into the core of how work operates.

One example came from healthcare. Organizations applying AI across claims processing saw up to 92% improvement in operational efficiency. Onboarding timelines dropped by up to 90%, and denial handling compressed from days to minutes, outcomes reflected in Zinnov’s AI Revolution in Healthcare: RCM Service Companies Leading the Way Towards Innovation report.

Behind these results were deliberate choices. Enterprises invested in stronger data consistency, clarified ownership for AI-driven decisions, and put governance structures in place that allowed automation to operate with confidence. Business leaders became more directly accountable for outcomes, and funding increasingly flowed toward initiatives with a clear path to execution.

Across industries, enterprise transformation in 2025 focused less on introducing new tools and more on rethinking how decisions and execution flow when AI participates directly in operations.

As enterprises strengthened their foundations in 2025, AI itself evolved in how it showed up across the organization. The shift was not just about broader adoption, but about where AI operated and what role it played in day-to-day execution.

We saw this evolution unfold across three distinct but increasingly connected layers.

Generative AI: Supporting Everyday Business Decisions

Nearly 80% of Generative AI investments in 2025 centered on workforce productivity and automation, signaling a clear shift toward efficiency-driven deployment. As a result, Generative AI moved firmly into the flow of daily work across enterprises.

Organizations used it to support reasoning, synthesis, and decision-making across Finance, HR, Engineering, and Customer Operations. Rather than operating as standalone tools, these capabilities increasingly lived inside existing systems, helping teams analyze information, explore scenarios, and make faster, more informed decisions.

The value came less from novelty and more from consistency: AI supporting thousands of small, repeatable decisions that shape business outcomes every day.

Agentic AI: Coordinating End-to-End Enterprise Processes

As enterprises looked beyond task-level automation, Agentic AI gained momentum as a way to coordinate multi-step processes across the enterprise.

Agentic systems began planning, sequencing, and executing work across ERP, CRM, IT operations, supply chains, and customer-facing platforms. As outlined in Zinnov’s Building the Agentic Frontier: How Enterprise Software Firms Are Engineering the Next Wave of Autonomous Systems report, the Agentic AI market stood at USD 12–15 billion in 2025 and is expected to grow at a 40–45% CAGR, reaching USD 80–100 billion by 2030, driven by enterprise adoption of agentic systems across core enterprise platforms.

As autonomy increased, enterprises tightened expectations around control and predictability, making governance and human oversight integral to production-scale deployment.

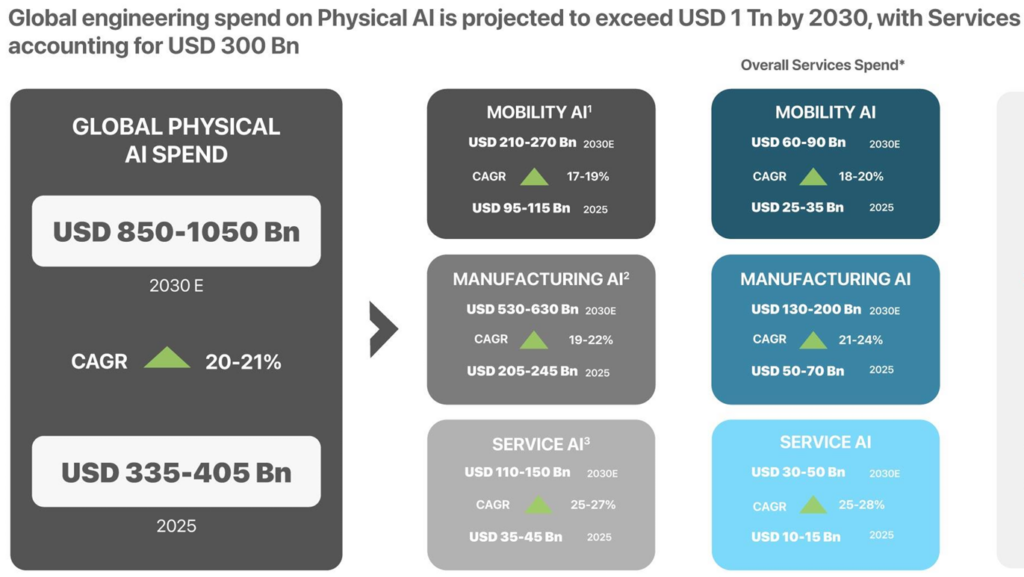

Physical AI: Executing Decisions in Real-World Operations

Physical AI extended enterprise intelligence beyond digital systems and into real-world environments. Deployments across Manufacturing, Mobility, and Services operations followed a Sense–Reason–Act–Learn (SRAL) loop, combining perception, decision-making, execution, and continuous learning to address constraints such as labor availability, safety compliance, asset uptime, and throughput.

Machines not only interpreted data but acted on it, adapting over time as conditions changed. As reflected in Zinnov’s Physical AI: The Next USD 300 Bn Opportunity for Tech Services report, this shift is attracting significant investment and shaping how industries think about resilience and continuity in operations

Together, these three layers expanded what enterprises expected AI to handle. They also increased execution complexity raising the bar for integration, reliability, and ongoing operations. This naturally elevated the role of engineering depth, operating discipline, and ecosystem support as AI moved deeper into the core of enterprise execution.

As AI moved deeper into enterprise execution in 2025, the constraint shifted from intent to capability. Enterprises understood where AI could create value, but running it reliably across complex environments proved harder than deploying it.

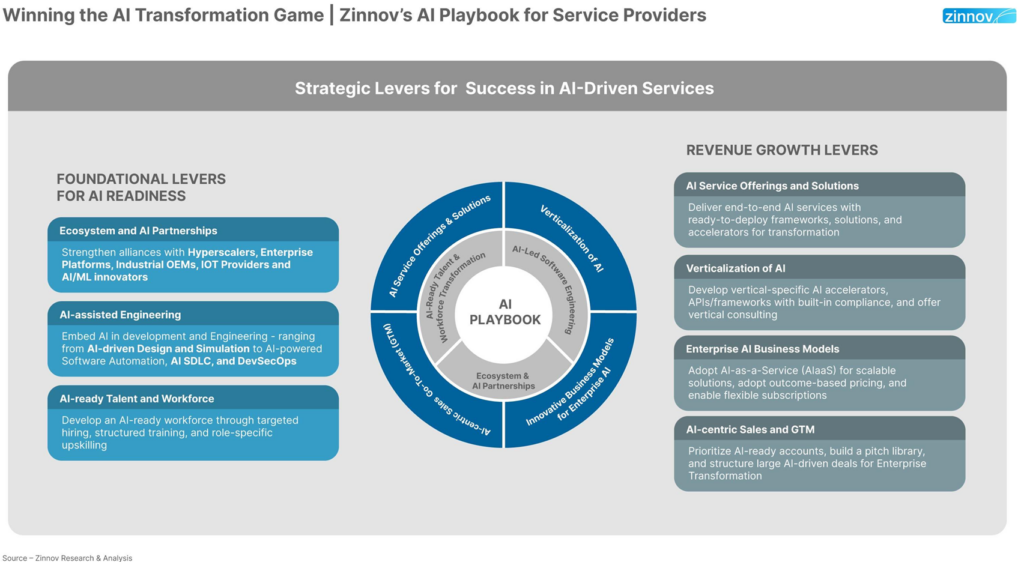

Tech Services firms held a clear advantage in this phase. They sat at the intersection of enterprise systems, data platforms, industry workflows, and operating models. Their engineering depth, integration experience, and ability to operate systems over time positioned them to support enterprises in ways that were difficult to replicate internally.

As a result, enterprises increasingly relied on Tech Services firms to move from deployment to sustained execution.

One such example emerged in physical operations. Physical AI deployments required close coordination between digital systems and real-world execution. This, in turn, drove demand for systems engineering, integration, simulation, and managed operations, creating a USD 300 billion Tech Services opportunity.

In practice, we observed Tech Services firms concentrate on a focused set of execution-critical areas: integrating AI into enterprise and operational systems, translating horizontal AI capabilities into industry-specific solutions, and operating AI systems consistently over time.

While enterprises set the direction for AI in 2025, Tech Services firms enabled that direction to be executed at scale.

As outlined in Zinnov’s The 2030 Tech Services Firm: Straight-Line People Business, No More whitepaper, this shift marks a broader transition toward IP-led solutions, outcome ownership, and managed operations as AI moves deeper into enterprise execution.

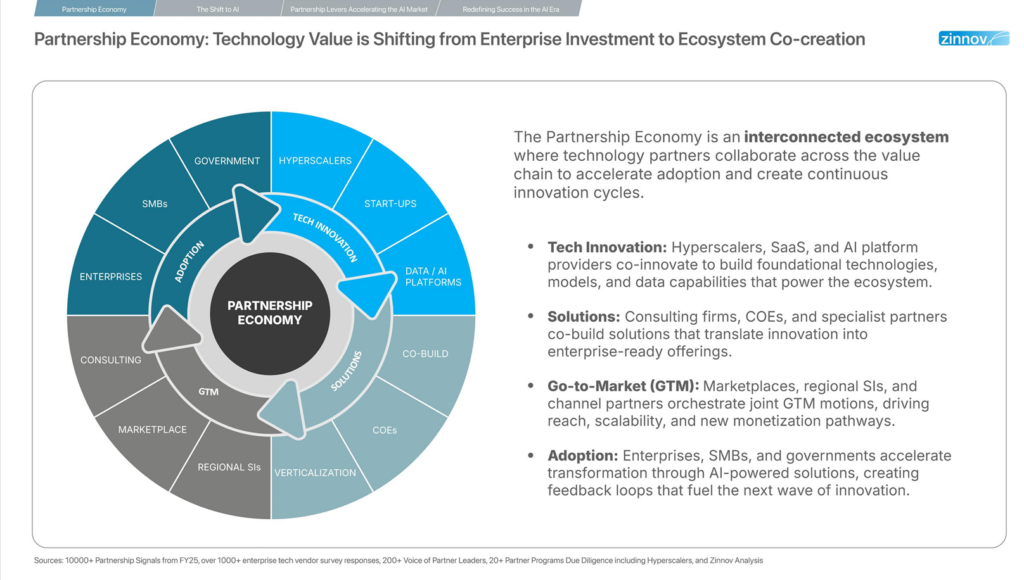

As enterprises scaled AI execution in 2025, partnerships became essential, enabling ecosystems to bridge capability gaps that no single organization could address alone.

Zinnov’s State of Partnerships 2026: Partnership Economy 2.0 – From Spends to Outcomes report, highlights how this shift played out in practice.

By the end of 2025, partnerships were no longer supporting AI adoption at the edges. They had become a core mechanism for scaling AI execution into measurable business outcomes.

What we saw in 2025 makes a few things clear about how enterprises will move forward:

In 2026, the advantage will belong to enterprises that act on these shifts early and consistently.