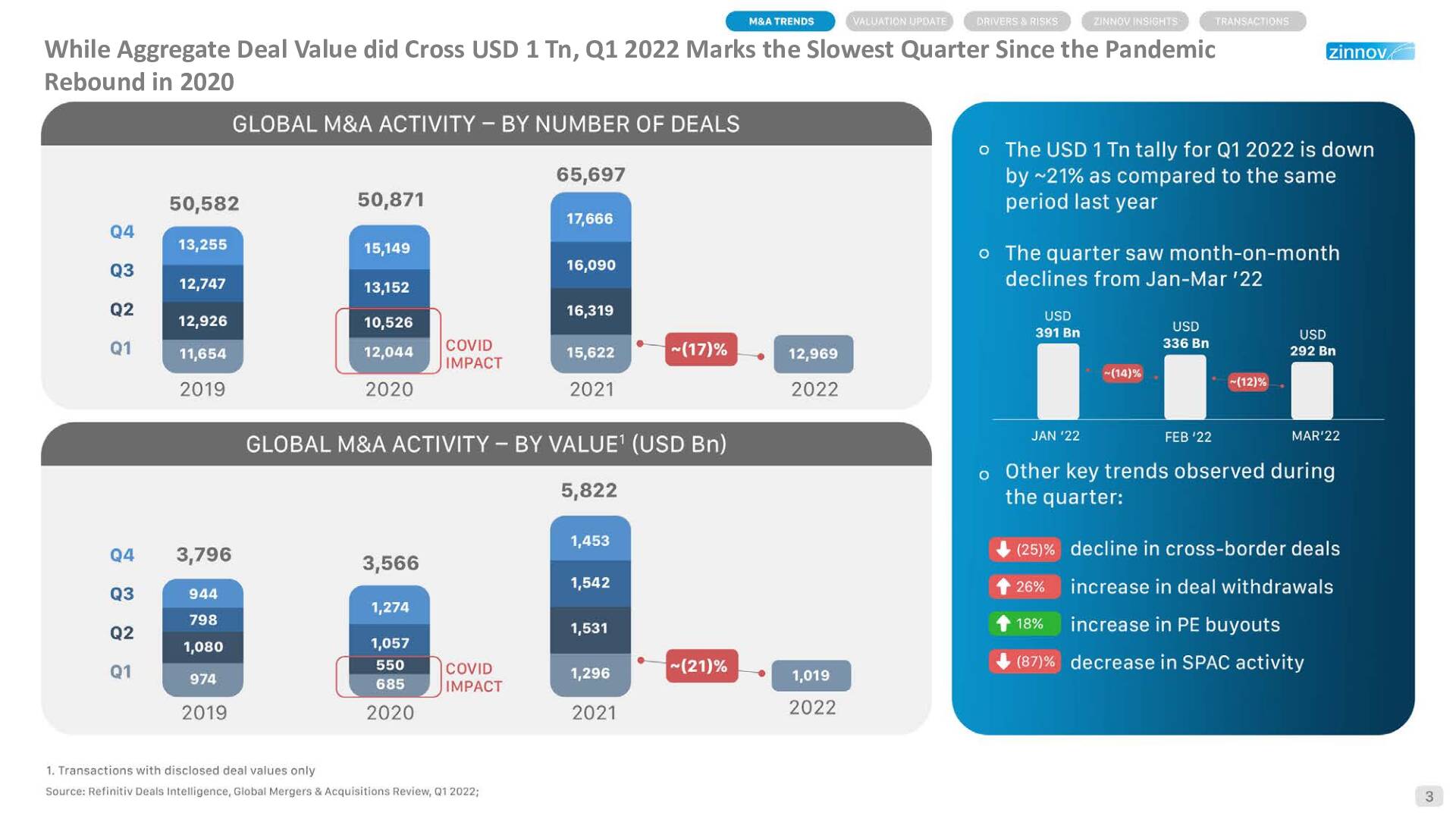

Following a record-breaking year for Mergers & Acquisitions (M&A), 2022 has had a relatively slow start. While the momentum in deal activity continued in January and February, the sky rocketing inflation and the Russia-Ukraine war have had a negative impact on the M&A market in March 2022. Also, the market trajectory through the quarter was negative, with month-on-month declines from January through to March.

Q1-2022 was the 7th consecutive quarter with over USD 1 Tn deal activity across sectors. While SPAC activity levels were down by ~87% vs Q1-2021, Private Equity buyouts were up by 18% to reach a record USD 291 Bn, which is the strongest YTD activity for PE buyouts ever.

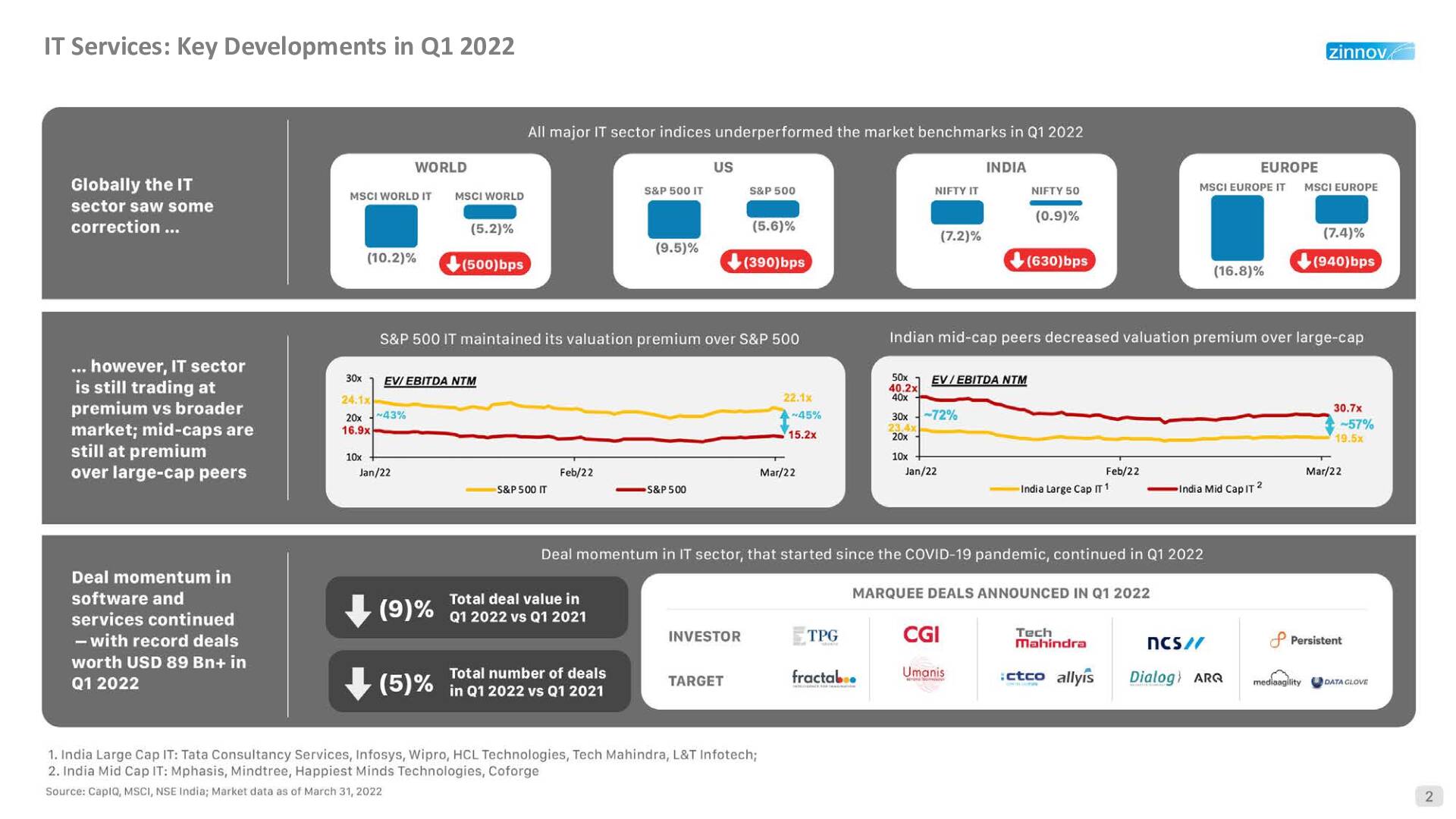

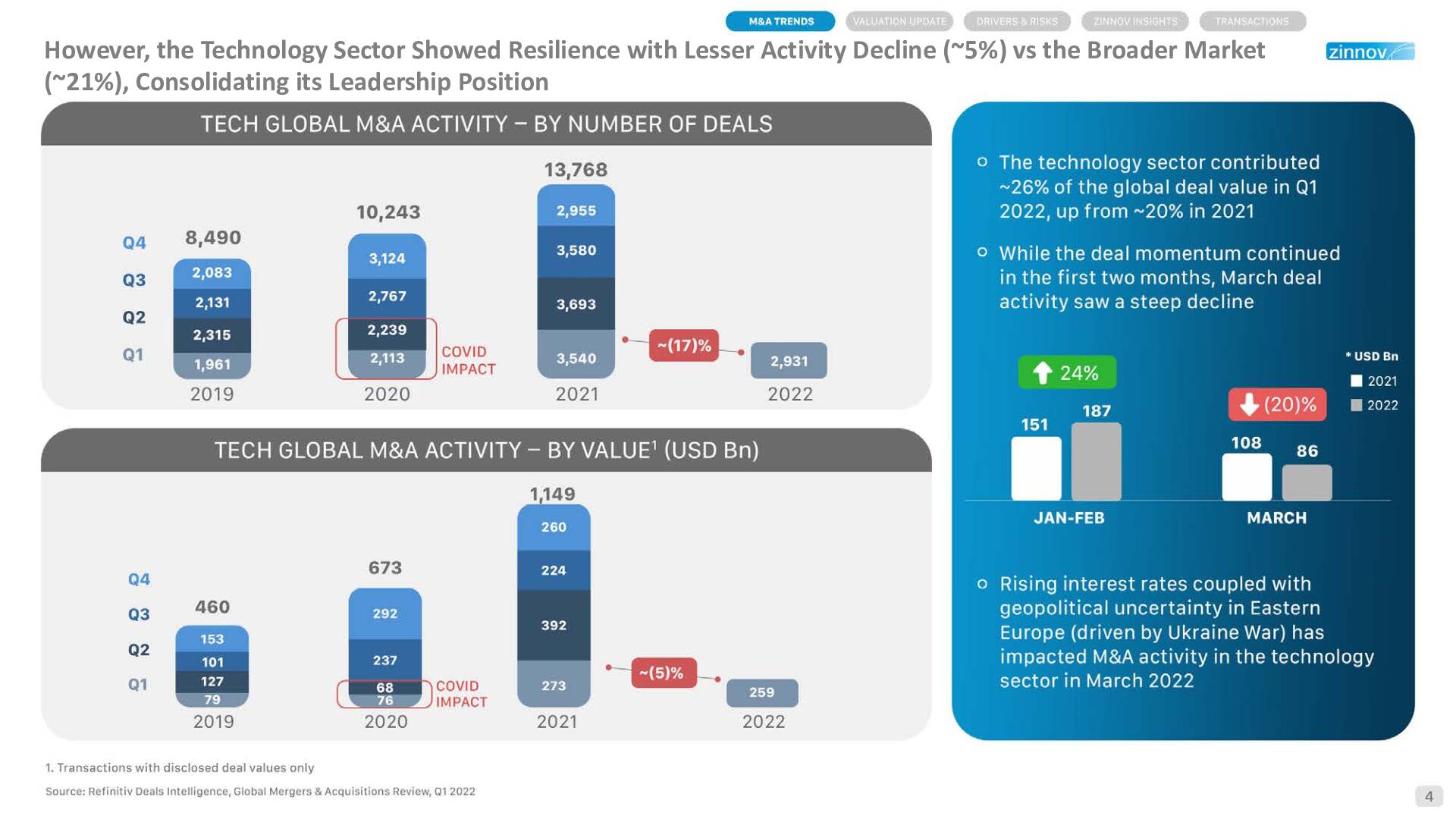

The technology sector continued to dominate the M&A market contributing ~26% to the global M&A value in Q1-2022, which was up from the ~20% contribution seen in Q1-2021. While the year started well for the technology sector, increased geopolitical tensions and the possibility of multiple rate hikes led to subdued M&A activity in the months of February and March. While public market valuations saw a mild correction in Q1-2022, they still remain at historically high levels.

While the deal activity was impacted in March, fundamental drivers of dealmaking remain robust. The technology sector continues to be a strong favorite for PE firms, while strategics continue to acquire the right assets to address portfolio gaps.

In this quarterly update, Zinnov’s M&A Advisory team explores key data points and M&A trends across the Technology & Services industry.

The report sheds light on: