Banks filing for bankruptcy. Banks hoarding cash to write off bad mortgages. The housing market collapsing. This was the scene of the BFS industry during the recession in 2008, which marked a catastrophic milestone in the history of the global economy, next only to the Great Depression of the 1930s. Now COVID-19 has led to a planned shutdown of leading economies and has severely impacted key industries such as aviation, automobile, hospitality, retail, etc.

The onset of this unprecedented situation has sparked off several questions – How has the BFS industry been impacted now? What are the measures being taken by BFS firms to keep the global economy afloat? What is the future of the BFS industry?

Impact of COVID-19 on the BFS industry

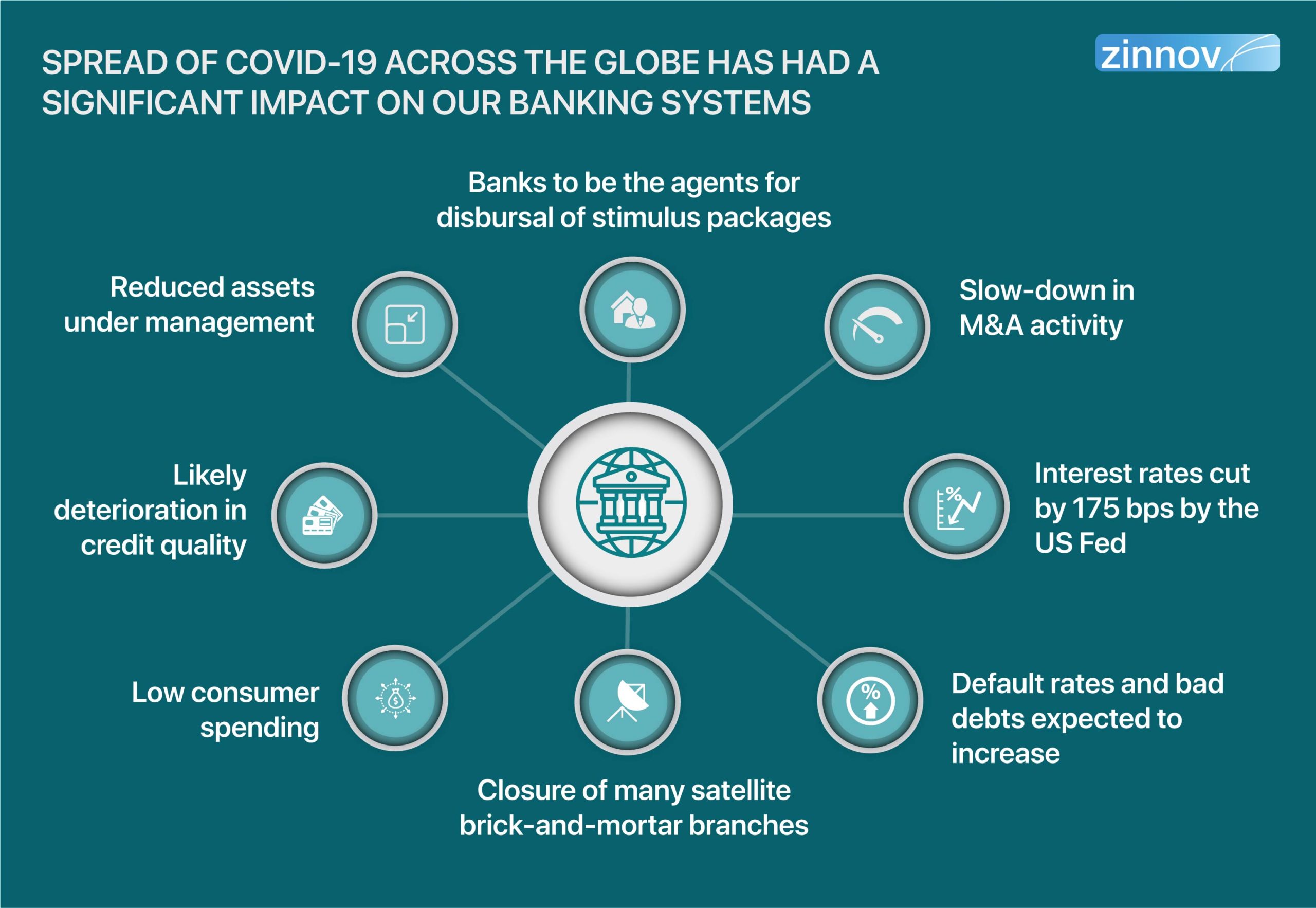

The rapid spread of COVID-19 has had a significant impact on the global banking systems, with its ripples being felt across the world.

Banks to be the agents for disbursal of stimulus packages

Banks have taken a deep blow with the collapse of global markets. The Central banks and governments across the world are stepping up to provide stimulus packages and other aids as countermeasures. An example of the disbursal of aids through central banks is the USD 2Tn Quantitative Easing program launched by the US Federal Reserve System to aid businesses and households.

Reduced Assets Under Management (AUM)

The overall AUM are showing a decline, thereby effecting a downward trend in the revenue generated from commissions for asset management firms.

Likely deterioration in credit quality

COVID-19 has brought about a deterioration in credit quality, resulting in losses across the credit portfolios. As far as commercial and wholesale banking are concerned, any increase in the borrowing volumes will be offset by the credit losses. The opportunities to refinance existing debts or raise new funding is also limited, given the current situation.

Low consumer spending

There is a significant shift with respect to consumer spending in the current situation, which is impacting various players across the BFS value chain. For example, online trading platforms like Robinhood and eToro are faced with declining trades as consumers are withholding new investments.

A slowdown in M&A activity

There is a marked slowdown in the M&A (Merger & Acquisition) and IPO (Initial Public Offering) activities until markets stabilize. Investment banks will however remain opportunistic and carry out M&A transactions in the industries affected by COVID-19.

Cut in interest rates

COVID-19 has forced the US Federal Reserve System to cut interest rates by 175 BPS (Basic Points) and the UK has also adopted the approach for their Small and Medium-sized Enterprises.

Default rates and bad debts expected to increase

A large number of BFS categories such as commercial & wholesale banking, wealth & asset management, investment banking, etc. are expected to witness a negative impact as customers default on payments. A classic reference point is China which is on the verge of facing its first credit downturn in decades. Capital markets will thus struggle to return to normalcy, even in a post-COVID world.

Closure of many satellite brick-and-mortar branches

With social distancing becoming the order of the day, there has been extensive closure of branches as well as back offices. Many banking services have been temporarily paused due to the absence of human intervention. The situation has also led to difficulties in maintaining SLAs (Service Level Agreements) and controls, owing to the reduced back office operations.

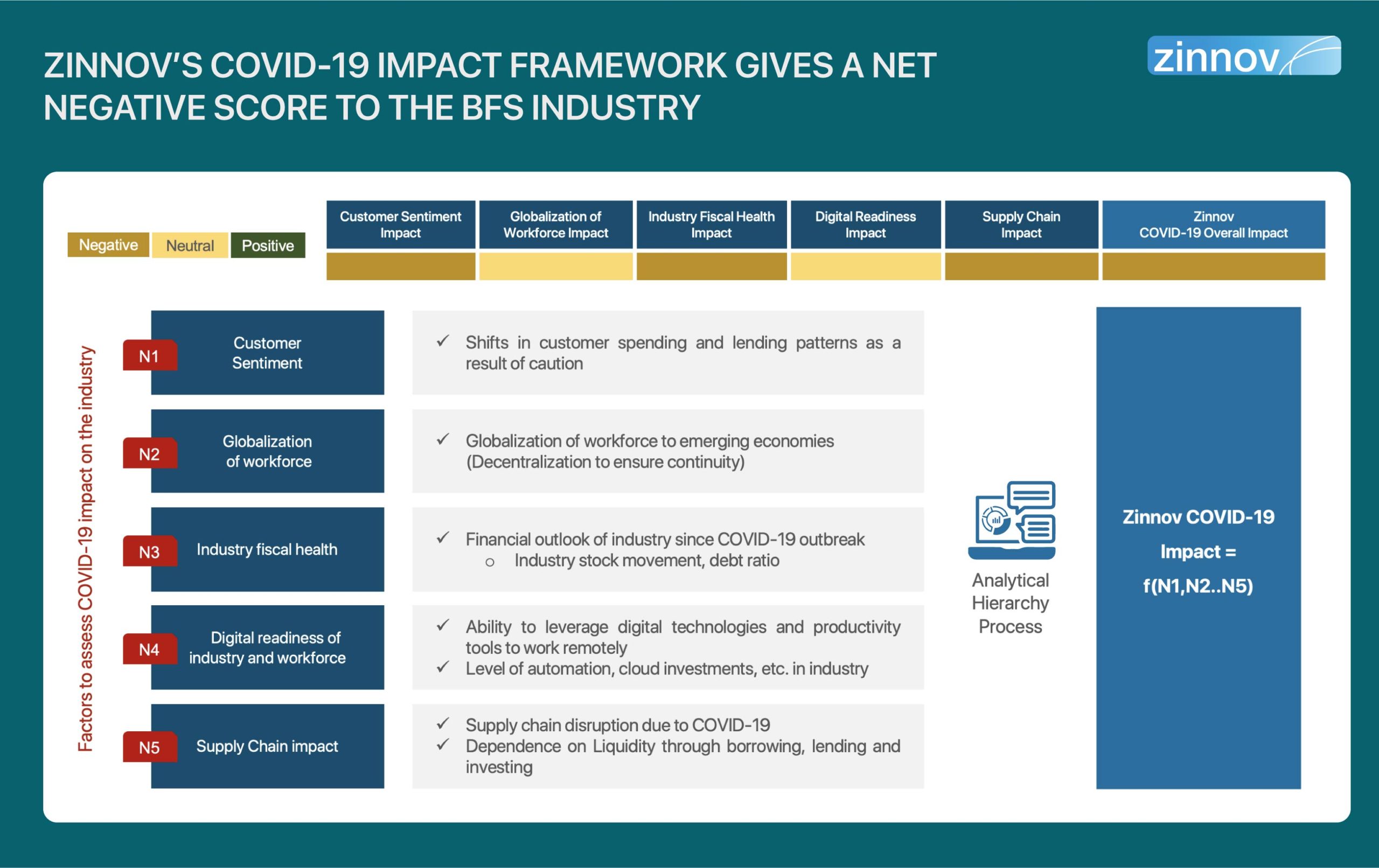

Zinnov evaluated the impact of COVID-19 on the global BFS industry as a whole and on the various players across the value chain across various parameters such as customer sentiment, globalization of the workforce, industry fiscal health, digital readiness, and supply chain impact. This impact has been rated across three levels – Negative, Neutral, Positive, and the overall impact on the BFS industry is negative.

The BFS industry is holding its own against COVID-19, re-emphasizing its good track record of resilience – the industry has survived the 2008 financial crisis and is now fiscally stronger because of it. But will the BFS industry’s resilience hold against COVID-19?

BFS and its Resilience

Unlike the other sectors facing a large-scale disruption due to COVID-19, BFS is one of the few sectors which has been preparing for a crisis of unprecedented scale. This preparation has made the banks became resilient with measures to build buffers in order to contain fallbacks. Post the 2008 financial crisis, most banks across the world began internal stress testing to avert a similar crisis in the future. Here are a few critical improvements aiding the BFS companies in tackling the current situation:

The BFS industry has thus been preparing for calamities, although with a few gaps yet to be addressed. But what role will banks play in overcoming this disruption?

The role of Banks in Navigating choppy waters

Looking beyond the COVID-19 impact on BFS industry, it has a unique role to play in the current situation. Governments across the world have introduced liquidity stimulus packages to support credit lines of major banks while reducing borrowing costs. These institutions are expected to act as agents for the disbursal of the stimulus packages. Therefore, banks will be expected to:

To overcome the stress on the liquidity buffer, banks are looking at their bottom line with renewed interest.

In addition, as banks adhere to social distancing norms while servicing their customers, going digital has emerged as a clear call to action. However, banks have been the slowest movers in the digitalization space due to the following reasons:

It’s high time the BFS industry accelerated its digitalization spend and build forward-looking digital-first institutions. What are the other critical areas of focus that will build a moat against such disruptions?

Focus for the Future

BFS companies need to build digital lending applications with a sense of urgency, in order to effectively be agents for disbursing the governments’ stimulus packages. Cutting costs through automation and a renewed focus on Liquidity and Risk Management will ensure that the banks come out on the other side with their credibility intact.

The immediate areas of focus would be to explore digital channels to sell products and adopting technology to reduce overheads, wherever possible. This will include:

The COVID-19 impact on BFS industry is a strong reminder that digitalization is the way forward. The goal, therefore, for banks will be to leverage the power of data and utilize digital to provide great customer experience through efficient banking.