USD 250 Bn industry was built on the foundation of a simple idea. Low-cost talent that can be trained to deliver high-quality software and business services. Indian Tech Services companies fueled their rapid ascent by setting up, managing, and scaling teams in cost-effective locations through Offshore Development Centers (ODCs). They outmaneuvered global competitors who lacked both the know-how and access to talent required to replicate this strategy.

For most customers—except a select few—building and operating such centers was neither practical nor desirable. The ODC model didn’t just lay the foundation; it became the bedrock of an industry that helped change India’s brand from a country of snake charmers and elephants to a country of Software Engineers.

As the tech world rapidly evolves, one question looms large: “Is the ODC model still relevant?”

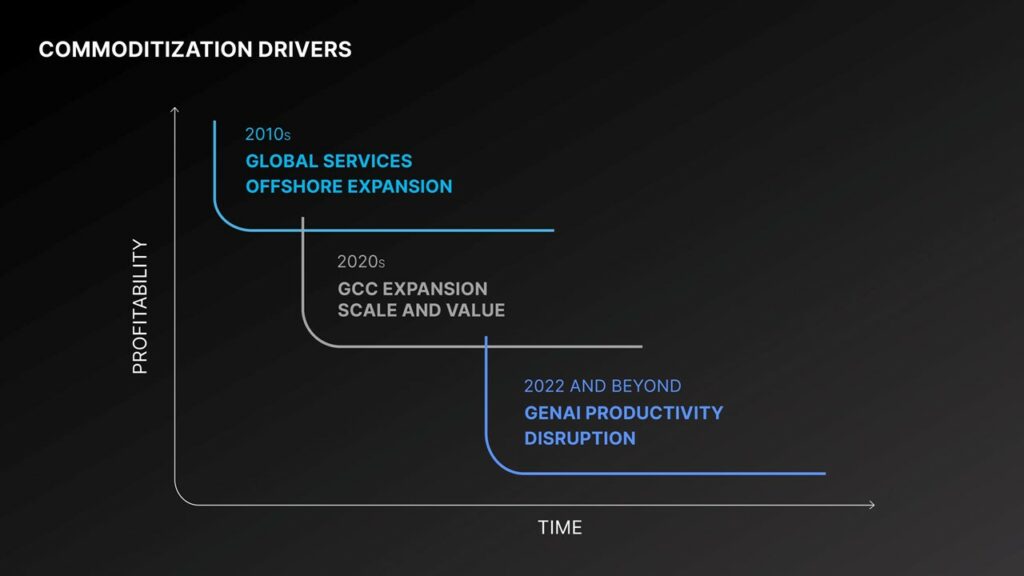

The ODC model is nearing the end of its lifecycle and becoming increasingly commoditized by three key forces:

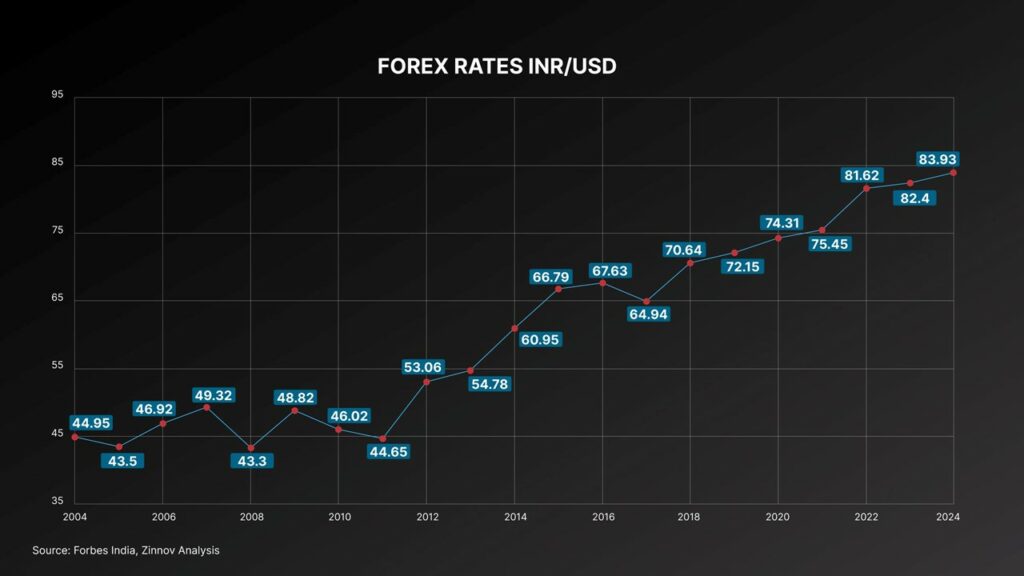

As customers’ willingness to pay went down, companies were able to sustain margins due to favorable forex rates. Since 2004, the Indian rupee has depreciated 86.6% against the USD. This decline has provided a natural cost advantage for Tech Services firms with revenue primarily generated from international clients, as it effectively lowers labor costs in USD terms. This trend has been instrumental in offsetting margin pressures and sustaining profitability.

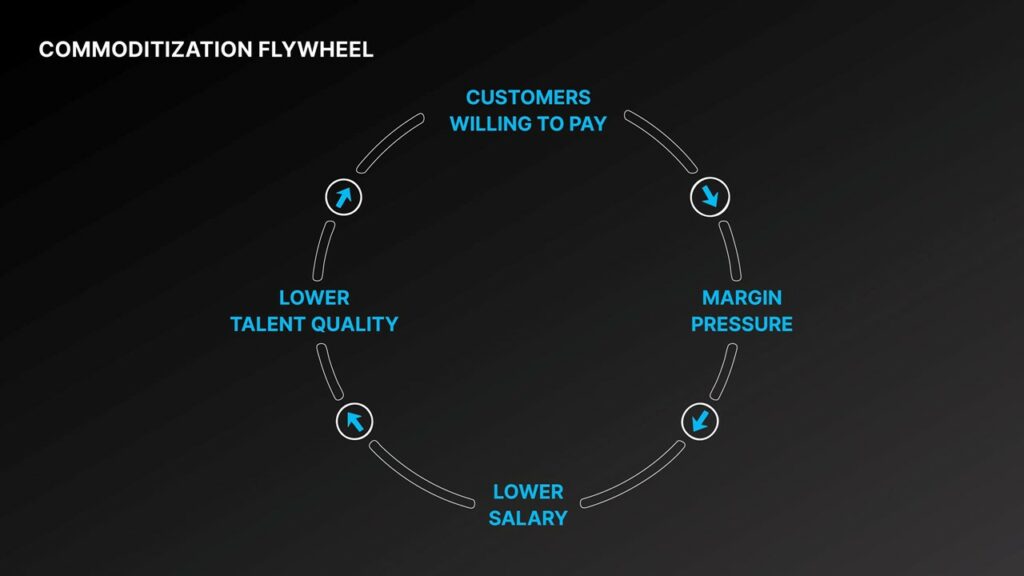

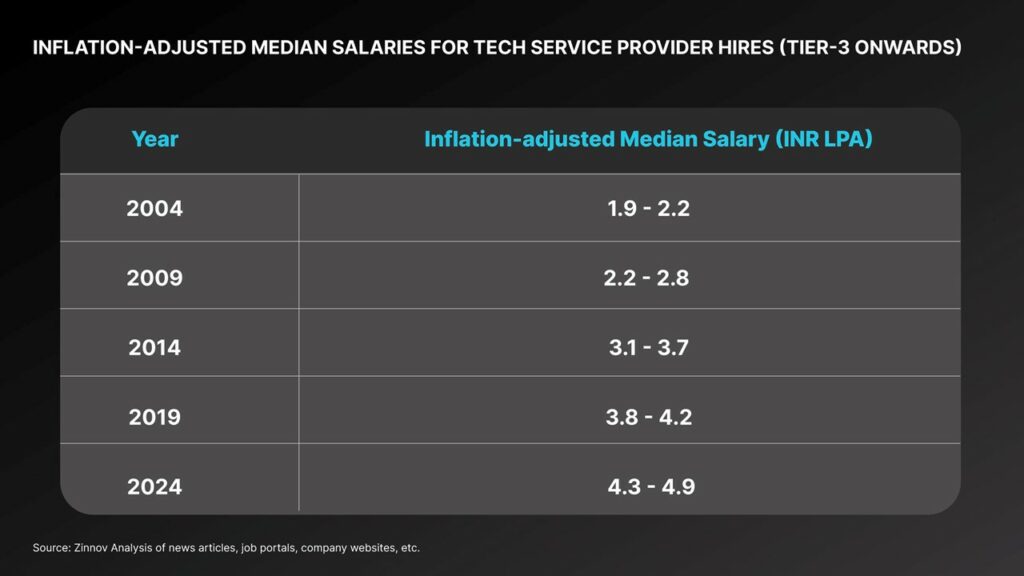

However, even the differential in forex rates was not enough to sustain the high margins. Due to the three commoditization forces mentioned above, the customer willingness to pay continued to decline. This forced companies to further optimize the talent pyramid by hiring more Entry-level Engineers and paying them lower inflation-adjusted salaries. The supply of fresh Engineers that increased 4X in twenty years from 400,000 in 2004 to 1.5 Mn in 2024 helped companies reduce the inflation-adjusted fresher salaries. They also moved away from hiring from Top-tier Engineering Colleges with strict entry criteria to easy-to-get-in Engineering Colleges that mushroomed across the country. Consequently, the top Engineers found their way to top start-ups, GCCs, and large fast-growing Indian Enterprises.

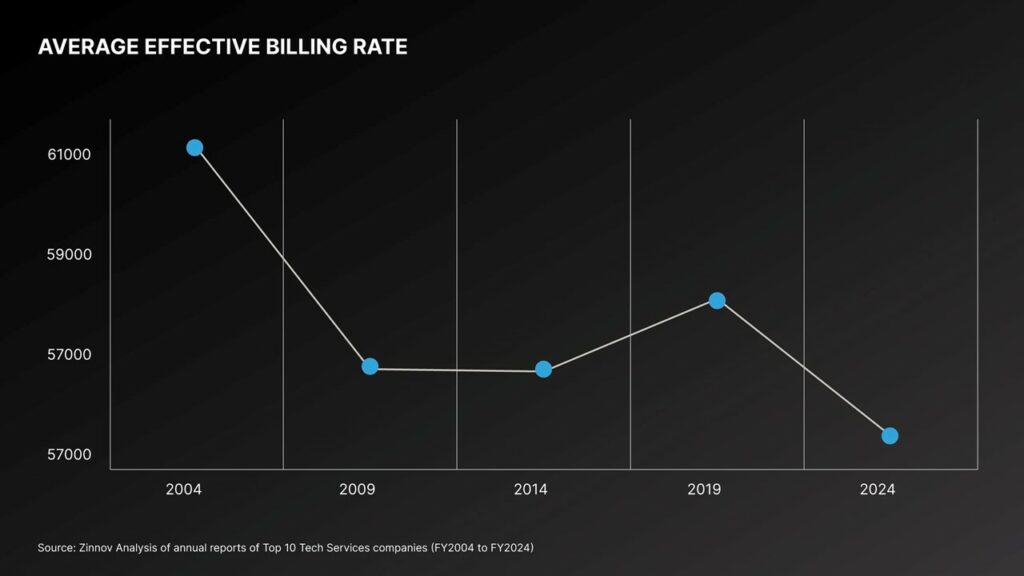

The resulting impact on the overall quality of work further affected the customers’ willingness to pay. And the effective billing rate gradually declined further.

Effective Billing rate = Revenue / (Headcount * Utilization Rate)1

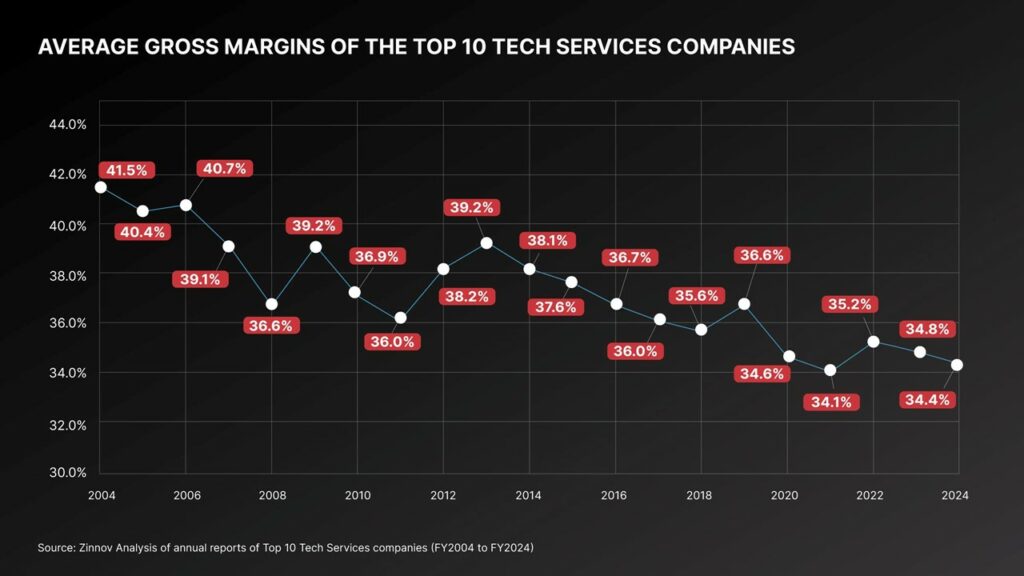

The ODC business model, which once provided gross margins upwards of ~40% in the early 2000s, has now settled into the margins typical of commoditized services and offerings. In fact, Tech Services firms have seen their gross margins tighten by as much as 700 basis points over the last two decades.

However, while the traditional ODC model may be waning, this shift presents new opportunities for Tech Services companies to reinvent themselves.

While we are witnessing the sunset of the high-profit ODC model, there are still significant opportunities for Tech Services companies to tap into:

When the industry last underwent a transformation in the late 90s and early 2000s, Accenture was able to rapidly grow and displace IBM as the preeminent Tech Services firm, owing to its strong consulting capabilities, coupling it with cost take-outs and offshoring advisory.

As the next set of Generative AI-led transformations take place, winners would be firms with extensive consulting capabilities that have access to the P&L owners and CXOs within enterprises, and not those that are majorly only exposed to CIOs/CTOs.

Enterprises are struggling to keep pace with the rapid changes in technology. Tech Services companies can add immense value by offering deep technology consulting services to help clients make informed decisions and navigate complex tech choices. They can help enterprises improve their agility by helping them reallocate resources to capture new opportunities. Transformation services, such as team, technology, infrastructure, and location carve-outs, can help customers to shift costs from legacy initiatives to new growth areas.

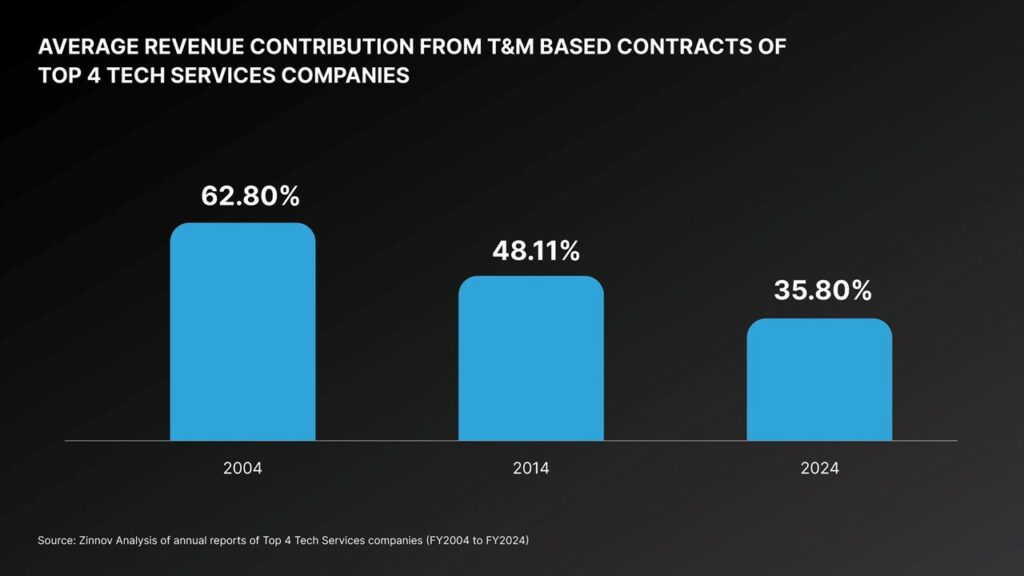

Enterprises are seeking collaborative partners who can co-innovate and commit to shared outcomes as well as risks. This calls for outcome-driven pricing models that align the goals of both service providers and customers, to ensure mutual success through shared accountability. The numbers speak for themselves – the revenue contribution from Time & Material-based contracts have been steadily declining.

With increased adoption of Enterprise AI, the cost of new applications and migrations will decrease. This will allow companies to move away from expensive SaaS subscriptions and build internal tools. AI-led development and managed services will become higher-value offerings that drive cost efficiency.

Enterprise technology was once expected to become simpler with the rise of SaaS, but instead, it has grown more complex. The future of Tech Services will be shaped by intelligent system integration that requires AI deployment, platform engineering, data engineering and analytics, and AI-driven automation. Intelligent integration will be a key driver of growth and contribute significantly to the industry’s incremental growth.

To navigate the commoditization journey of the ODC model and offer new services, Tech Services companies would have to rebuild their capabilities:

When the fundamentals of the profit drivers are changing, hiring and retention patterns need to change as well. Over the last decade, Tech Services companies have been trying to shed the “flab” in the middle of their pyramid, while bulking up the bottom of the pyramid, to manage margin pressures. With AI potentially changing how most of the code would be written, and by whom – the volume-based hiring from campuses will reduce over the next decade, while focusing on retaining talent with great domain and contextual expertise.

The fresher training engines will need to be retooled, with more focus on domain and basic sciences, as compared to focused training on coding languages, agile processes, etc., as is the practice now.

The net winners of the AI shift are going to be the consulting organizations, who have the right relationships and have the back-end scale. Majority of the Indian Tech Services firms today do not have the front-end consulting muscle. They will have to organically build it, while making the right inorganic punts – at boutique houses, or carve out front-end consulting organizations from the Big 4.

Currently, most of the sales conversations are still driven by cost take-outs that Tech Services firms can enable for customer CIOs and CTOs, and by volume of talent that could be deployed at scale and pace. This would need rewiring with more business context, and increasingly with the customer CFO, not limiting just to the CIO or the CTO.

The industry has made progress in structuring larger deals that focus on outcomes and risk-sharing. These models often work best with existing customers, since larger deals require higher levels of trust and credibility. To sustain profitability on such deals, companies need to focus on operational efficiency, ensuring margins are secured in the latter stages of contracts.

Companies should consider spinning off new ideas that require distinct business models and operational rhythms to thrive. This approach helped make the BPO industry successful. Now is the time to create similar spin-offs for AI-led Tech Services, with the potential for spin-ins once the AI wave matures. Companies should also explore bold acquisitions as an alternative to the spin-off/spin-in strategy, to accelerate their capabilities in key areas.

Bold, visionary, and courageous leadership is the need of the hour, if Tech Services firms are to seize these new opportunities. In the past, many Indian Tech Services companies brought in CEOs from the Software industry to drive change – but these transformations often proved challenging. Companies should look deeper within their leadership bench to identify potential leaders – even two levels down from the CEO – who have the potential to drive transformation.

Create strong leadership programs to train young leaders in the company who have the conviction, courage, and capability to be a part of such transformations. External leaders can succeed if they demonstrate empathy for the company culture and build the right team to lead the transformation.

In a constantly changing tech landscape, clinging to outdated models is no longer an option. By embracing innovation, investing in talent, and adopting newer business models, Tech Services companies can not only survive but thrive in this new era.