We are in an era where the start-up ecosystem is inundated with unicorns, with horses left behind far enough in the fields to graze! A unicorn is a privately-held start-up/company which is valued at over $1Bn. As the valuation of these unicorns rises, so do their names – a pentacorn is valued at over $5Bn, a decacorn is a company with valuation over $10Bn, and a hectacorn is valued at over $100Bn. Interestingly, unlike an established company’s valuation which is based on past years’ performances, a start-up’s valuation is arrived at through its growth opportunities and expected long term development for its potential market.

While the term was coined in 2013 by Aileen Lee comparing these rare companies to the mythical creature, unicorns have only multiplied exponentially, especially in the past 5 years. As of January 2019, the number of unicorns stands at a whopping 335, with a total cumulative valuation of ~$1090Bn, according to CBInsights.

In the last 5 years, the Unicorn club in the startup ecosystem has seen exponential growth, with a hockey stick rise, in terms of the number of companies formed. Verticals such as TravelTech, Enterprise Software, and eCommerce/Marketplace are home to a large number of unicorns. When it comes to capital, unicorns have leveraged a diverse group of non-traditional investors such as public market funds, along with micro-investors like angels and accelerators across growth stages to reach the hallowed halls of the Unicorn club.

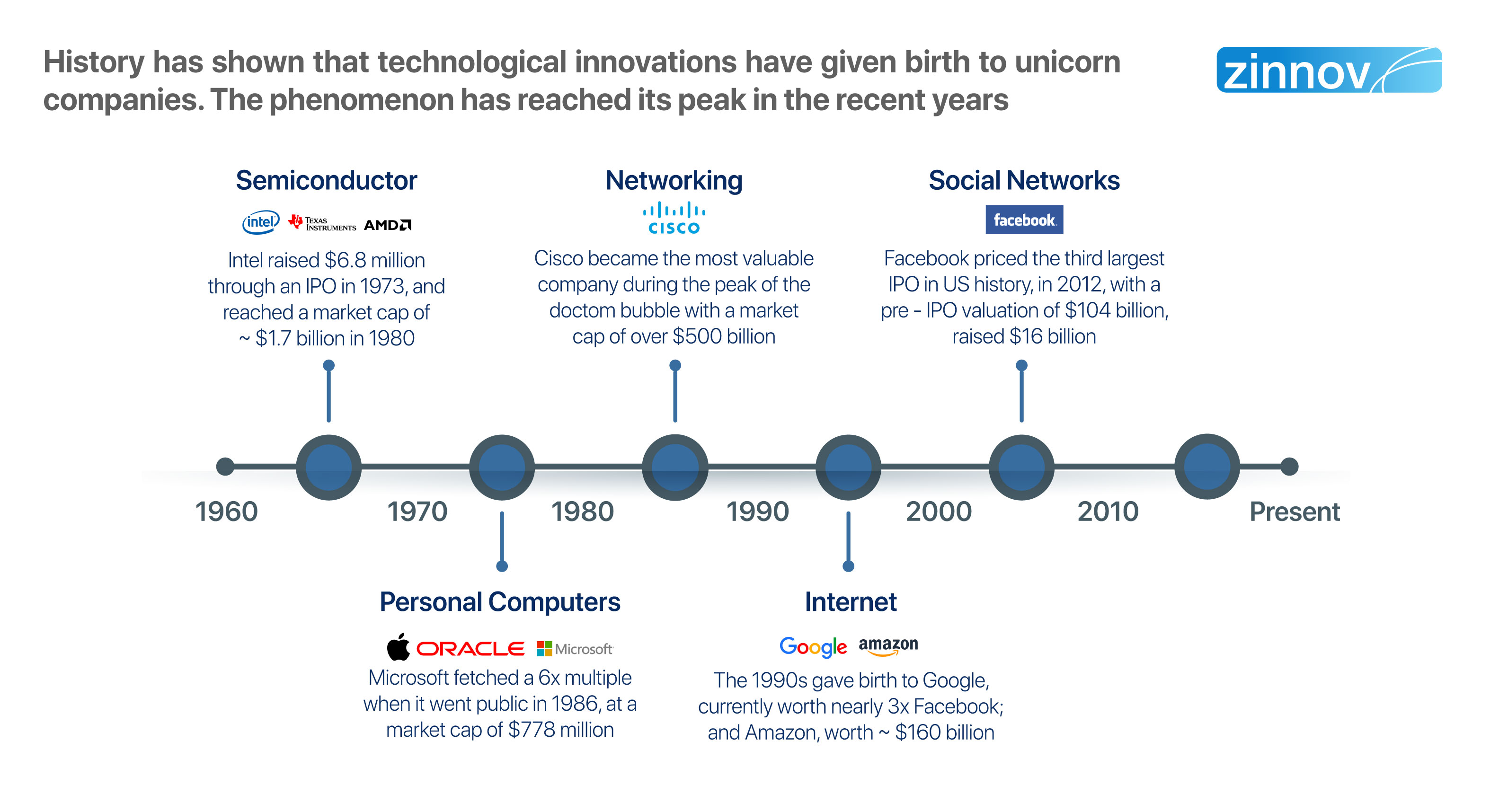

Historical data suggests that technological innovations have given birth to unicorns, a phenomenon that has reached its peak in recent years. However, as more technological innovations come to the fore, more unicorns are being birthed. But, in the recent past, being part of the Unicorn club hasn’t been all that rare, because of the sheer number currently in existence. While the US housed the most number of unicorns till about 2015, geographies such as China, India, and the UK are homes to unicorns today. In fact, 63% of unicorns established from 2012 to 2017 are outside of the US.

Unicorns have disrupted several traditional industries, as a direct consequence of global user base, optimizations in technology product development, and a change in customer mindset to adapt to new products. A few prominent examples include Uber disrupting the traditional taxi industry, Airbnb disrupting the lodging industry, and with a lean team of 50 engineers, WhatsApp disrupting the telecom industry in less than 4 years.

Verticals such as automotive, telecom, media & entertainment, retail, enterprise software, and healthcare & pharma are leading the pack with a large number of unicorns. From sharing economy to OTT to personalization to immersive experience, unicorns have caused disruptions and put customer experience and expectation at the core.

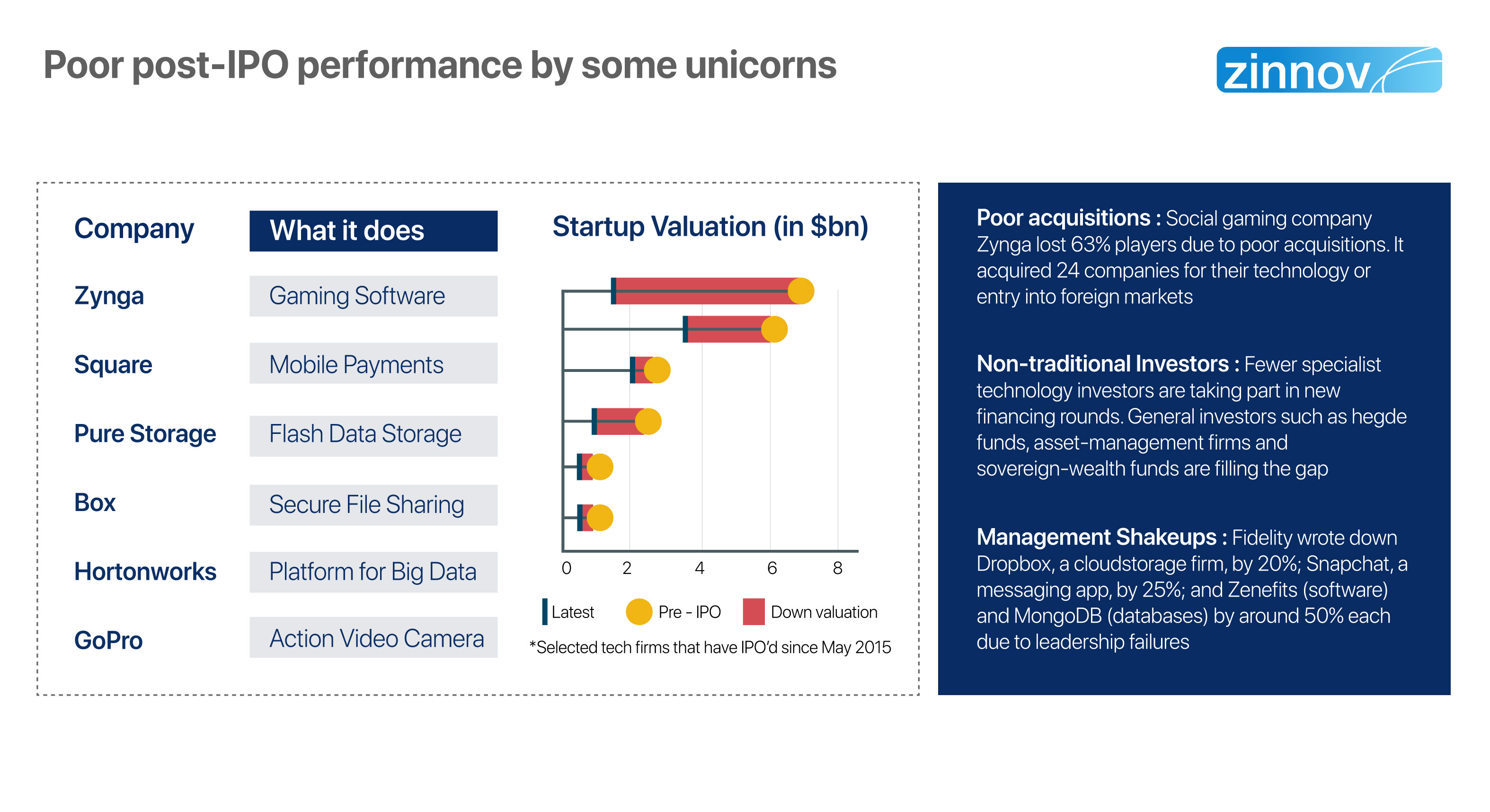

One of the primary aspects fueling the growth of unicorns is the investment that is being pumped into these companies. A varied set of investors, ranging from angel investors to public market funds – mutual funds and hedge funds, to venture capital firms to corporate venture arms have invested in unicorns. While these investments are propelling these companies to taste stratospheric growth in a compressed time frame, there have been some serious concerns as well.

One example is Square, which priced its IPO at $9 a share in November 2016, well under the $15+ that private investors paid the year before. Though the share price did rise during the IPO, the firm’s valuation leveled off at around $4Bn, just two-thirds of the $6Bn that Square was valued at.

Theranos is another exalted unicorn which fell flat early on. Started in 2003, by a then-19-year-old Stanford dropout, Elizabeth Holmes, Theranos was the blood testing start-up that had everyone hankering to get a piece of. Theranos, once valued at a whopping $9Bn, came under repeated fire for vaunted core technology, unreliable results, questionable methodology, and inadequately trained staff. Following a furor over the false claims of the breakthrough technology used as well as the very small amounts of blood required for the tests, the company was shut and its assets subsequently liquidated.

The large investments being made in unicorns are eerily similar to the infamous tech bubble era of the mid-nineties. Many unicorns, though valued in excess of $1+Bn, are operating at low revenues and fewer customers. Additionally, some of the unicorns that have gone public, have posted poor post IPO performance which further cement the comparison to the dot com bubble era.

Despite these missteps by some unicorns, these high valuation companies are real, much bigger, and different than the failures of pre-2000 era. Three key factors are shaping the stratospheric growth of these unicorns –

a) Larger addressable markets: Since inception, unicorns are targeting global markets. Additionally, 3.9Bn people who have access to the Internet and are spending close to $3Tn online, the world has truly become flat.

b) Higher revenues before IPO: Today, unicorns are posting higher revenue growths before filing for IPOs than the younger companies of the Internet bubble era. In the pre-2000 era, 65% of investments were funneled into companies that were less than 3 years old, while in 2016, 80+% of current investments were made in 3+ year-old companies.

c) Born global: Unicorns and other start-ups are accessing global markets and targeting multiple industries in the early growth stages itself, thus casting a wider net to gain customer access. They are leveraging a much larger customer base across global markets, across verticals such as TravelTech, Food delivery, AutoTech, and Aerospace.

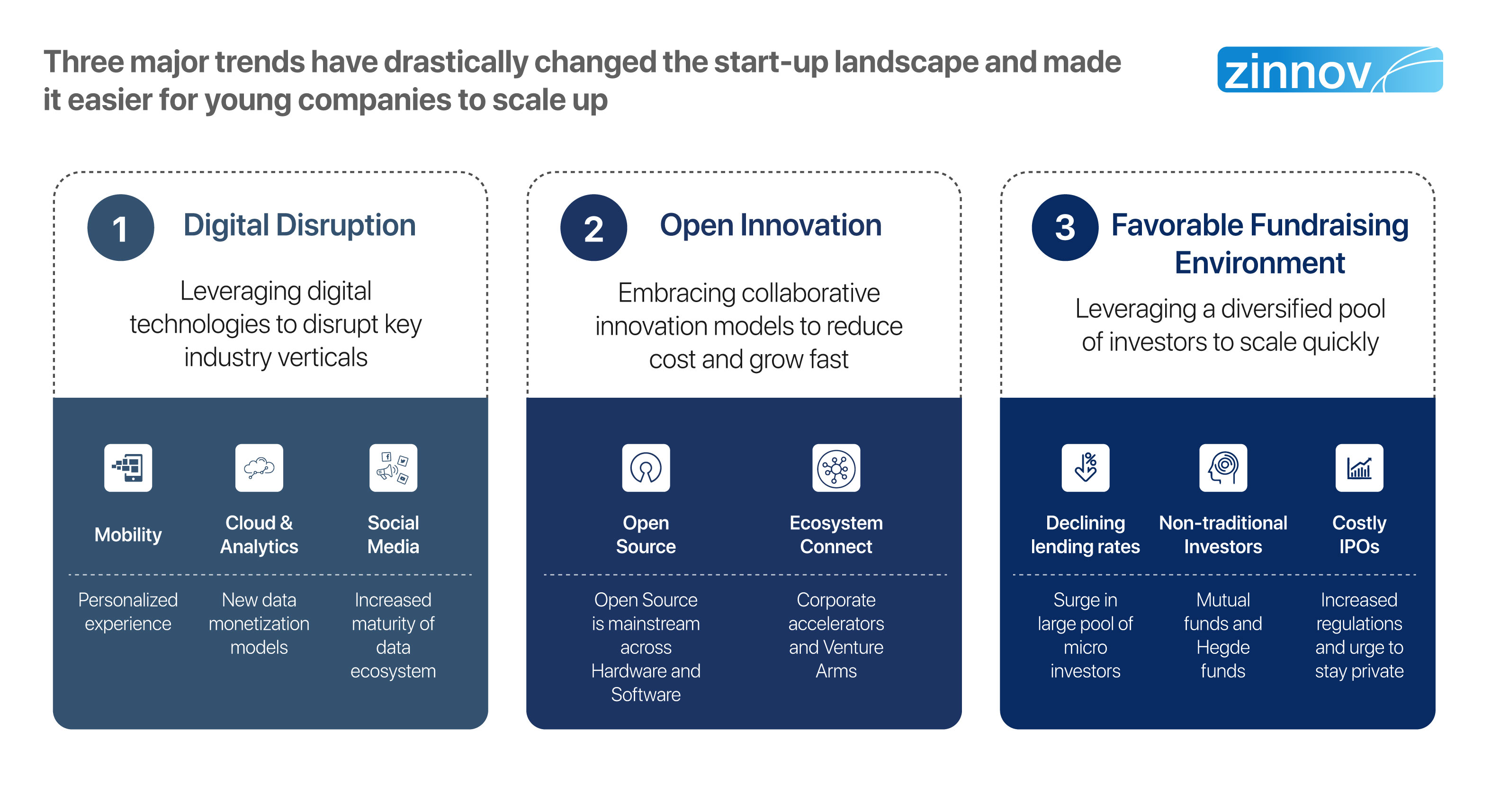

Besides the broad level factors outlined above, three key enablers are further fueling the seemingly sudden explosion of unicorns, thus making it easier for young companies to scale up in a short time frame –

Digital technologies have impacted businesses, irrespective of verticals. In fact, every business is transforming into a digital business. Companies leveraging digital technologies to disrupt key industry verticals has been the modus operandi of most members of the hallowed Unicorn club. Digital technologies have also enabled companies to provide personalized experiences to customers (through mobile), develop products through agile processes (cloud), and take data-driven decisions in real-time (big data and social).

The impact of digital is far-reaching and is being felt by large organizations as well. They are establishing new age business units that are focused on digital platforms. General Electric (GE) set up a digital business unit, GE Digital, to compete in the IoT market with IBM and other large analytics players. Walmart established Walmart Labs to develop technologies and solutions for its global eCommerce business.

In the wake of start-ups – especially unicorns – disrupting the way traditional organizations across verticals operate, these organizations have realized the potential of working with unicorns. Hence, large organizations are creating a viable ecosystem for start-ups to prosper and grow through multiple avenues such as venture arms, accelerators, mentorship support, etc. Further, the democratization of computing through cloud computing and open-source platforms have enabled organizations to scale rapidly with limited capital budgets.

Large R&D spenders are building the core infrastructure and platforms across emerging technologies to enable newer companies to invest in vertical use cases. Additionally, these large spenders are also creating an open innovation ecosystem through multiple avenues such as accelerators and venture arms, which provide specific support in areas such as product GTM, customer and investor connect, business and technology mentorship, ecosystem partnerships, to name a few.

Several reasons have laid the ground for creating a favorable funding environment for the exponential growth of start-ups.

(i) The lower interest rates set by the Federal Reserve since 2009 have pushed a large number of investors into the private market. This has propelled the rise in participation from micro-investors like angels and accelerators, who are investing in numerous start-ups, which promise higher returns than conventional investment channels.

(ii) Late-stage investment valuations have been fueled by the interest of mutual funds and hedge funds in the private market. Also, the private market is yielding higher returns to investors than the public stock market.

(iii) Near-zero interest rates are driving investments away from bonds and fixed-income securities into start-ups that promise higher returns.

In a time when unicorns and start-ups are rewriting the rules of the game and are bigger, faster, and better than ever before, traditional organizations have their work cut out for them. It’s a game of do or die, with very little room for the in-betweeners – those that are barely in the game, playing safe. Unicorns are here to stay, and their ilk will only grow and expand in the years to come. With the average age of an S&P company bottoming out at a mere 20 years, traditional companies need to gear up and build a moat around their business – stat!