|

|

Every software company moves through a predictable arc: early funding fuels speed, the mid-stage demands structure, and scale requires a different operating system altogether. The transition between these stages is where most companies lose momentum. Zinnov’s analysis shows that 42 percent of companies in the USD 100–500 Mn band are already more than 25 years old, highlighting how often firms plateau at this stage. Complexity begins to grow faster than the systems built in earlier phases, creating a long-term stall rather than a temporary slowdown.

Early systems are designed for speed and improvisation. They are not equipped to manage the weight, interdependencies, and coordination needs that arise as product portfolios broaden, customers scale globally, and functions expand across regions. Execution becomes less about market opportunity and more about operating maturity.

This strain becomes visible across the organization.

These challenges reflect an operating model that has not kept pace with the company’s scale. Demand is rarely the issue. Operating maturity is.

Companies that scale beyond the USD 100–500 Mn plateau institutionalize four capabilities, with Private Equity (PE) backed companies excelling because their operating models hinge on four core execution levers.

Partnerships become a formal revenue channel in PE based companies. Companies define partner tiers, align co-selling programs, and create standardized materials that support consistent positioning across the field. Partner performance is tracked through the same forecasting and review processes used for direct sales.

Impact: broader distribution, more efficient market entry, and higher attach without linear sales hiring.

Engineering scales across global centers spread across geographies that foster innovation and scale. These hubs operate on shared tooling, processes, and security frameworks, enabling continuous development cycles and access to diverse skill sets.

Impact: faster delivery, stronger margins, and capacity for reinvestment.

M&A is run as a structured program. Companies use adjacency maps to guide target prioritization, establish integration offices, and execute 100-day plans supported by synergy dashboards.

Impact: targeted capability expansion without operational drag.

Sales execution becomes consistent and predictable. PE-backed companies define sales stages, implement reliable forecasting methods, build structured coverage models, and provide standardized commercial guidance. Partner motions are incorporated into these processes to ensure full visibility.

Impact: higher win rates, more consistent deal cycles, and forecasts leadership can rely on.

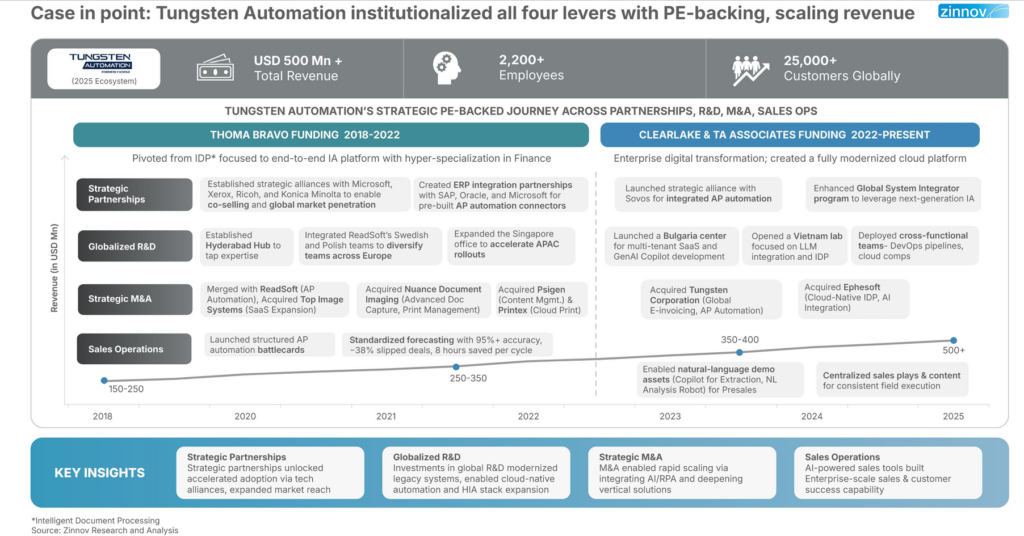

Case in point: Tungsten’s trajectory shows what happens when all four PE levers fire in sequence.

Phase 1: Thoma Bravo (2018–2022)

Tungsten aligned deeply with enterprise ecosystems. Partnerships with Microsoft, Xerox, Ricoh, and Konica Minolta created access to large enterprise customers. Pre-built connectors for SAP, Oracle, and Microsoft standardized AP automation and reduced implementation effort.

Engineering operations expanded and were coordinated across Hyderabad, Sweden, Poland, and Singapore. These hubs operated on consistent processes, improving delivery velocity and maintaining margin efficiency, while keeping the pedal on constant innovation.

Acquisitions included ReadSoft and Top Image Systems to expand the application layer, as well as Nuance Document Imaging, Psigen, and Printix to strengthen content, capture, and print capabilities. Integration focused on building a unified platform.

Thoma Bravo standardized sales stages, processes, and forecasting approaches, which reduced slippage and improved predictability.

Phase 2: Clearlake and TA Associates (2022–present)

A strategic partnership with Sovos and a more developed GSI engagement model strengthened enterprise positioning in regulated automation and global environments.

New engineering centers were established in Bulgaria for multi-tenant SaaS and Copilot development and in Vietnam for LLM-driven IDP. DevOps and cloud engineering teams ensured platform consistency.

Tungsten Corporation expanded e-invoicing and AP automation capabilities. Ephesoft added cloud-native IDP and accelerated AI integration.

Centralized sales plays and standardized AI-assisted demo assets improved consistency in customer conversations and evaluation processes.

Together, these phases show how Tungsten has strengthened its operating model, increased product velocity, and modernized its go-to-market model.

Most enterprise software companies stall in the USD 100–500 Mn band because their operating model does not keep up with their growing complexity. Companies that move beyond this plateau do so by upgrading how the business operates, not by increasing headcount or product lines alone.

PE-backed companies in the growth stage outperform because they bring structure, discipline, and alignment to the areas that matter most. They strengthen partnerships, global R&D, M&A, and sales execution in ways that create predictable scale.

At this stage, ambition is not the barrier. Execution is. Companies that modernize their operating model move forward and successfully cross the growth chasm leaving behind those companies that are stuck with legacy processes and execution models.

For deeper insights into how software enterprises can break the growth barrier, read our full report Breaking the Growth Barrier: Enterprise Software Scaling Blueprint.