The year 2024 has presented fresh challenges and exciting opportunities in the M&A landscape for both buyers and sellers. Despite the 2023 downturn, deal-making defied expectations with a strong Q1 2024, even amidst ongoing economic worries and global tensions. This surge in M&A activity across sectors, with deal value reaching USD 798 Bn compared to USD 580 Bn in Q1 2023, is fueled by emerging trends that signal a significant rebound.

The Technology Services sector has emerged as a frontrunner in the resurgence of global M&A activity, with Q1 2024 witnessing a significant surge in deal value to USD 125 Bn, up from USD 92 Bn in Q1 2023. This positive sentiment surrounding tech deals suggests a bright outlook for the rest of 2024.

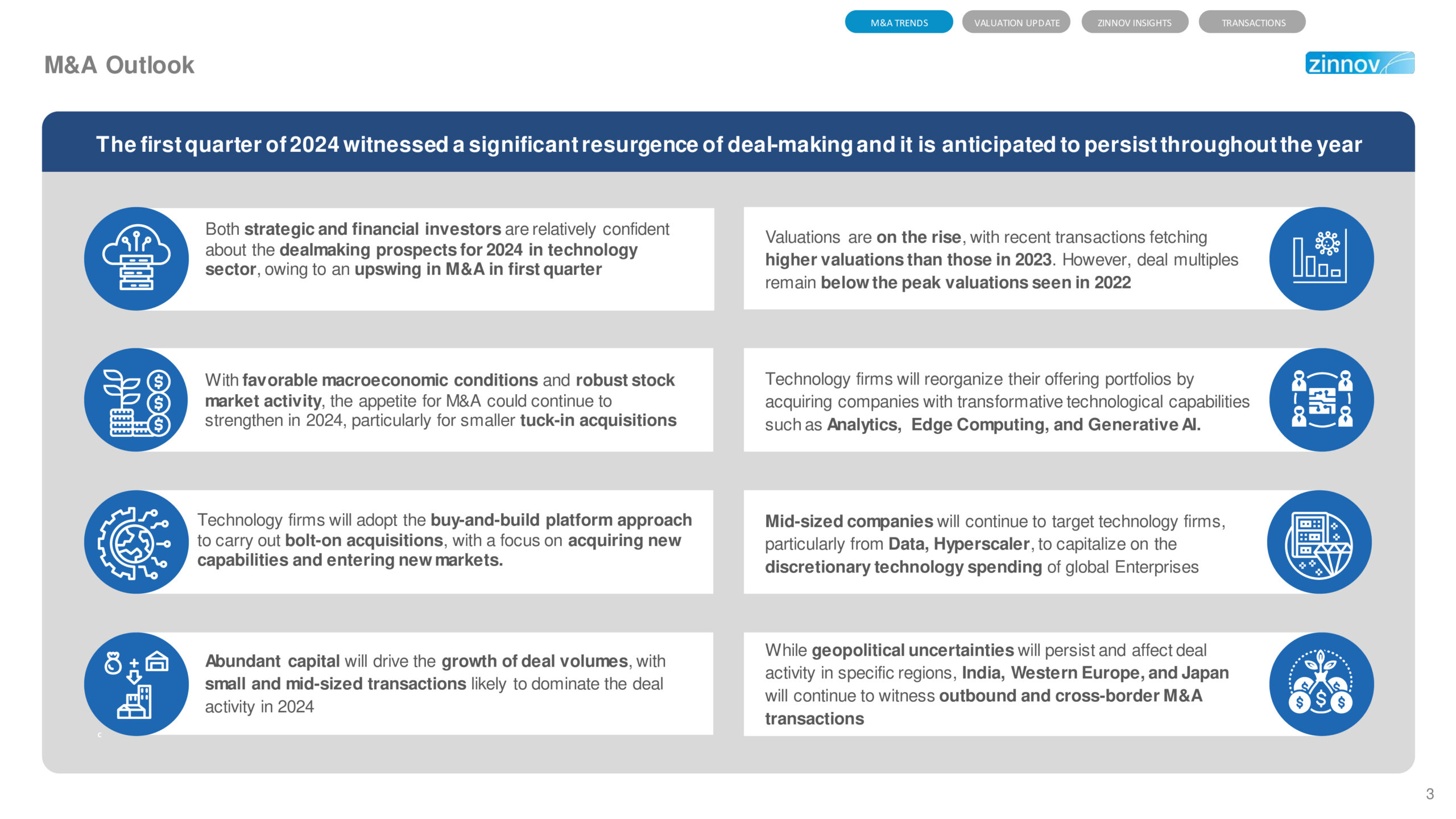

The positive sentiment in the Technology Services sector is driven by several key factors that have collectively fostered a wave of cautious optimism in the broader Mergers & Acquisitions landscape. The stabilization of inflation and interest rates, coupled with the availability of ample capital awaiting deployment, has reignited confidence among dealmakers. Moreover, companies are recognizing the operational imperatives of portfolio restructuring for digital agility and resilience, further fueling M&A activity.

Notably, dealmakers are increasingly confident that the current interest rate cycle has reached its peak, and systemically important central banks in the US and Europe will ease monetary policy in the near term. This belief has paved the way for pent-up buyer demand and a growing pool of seller assets, setting the stage for a transformative year in M&A.

Driven by the strong market performance in 2024, technology companies are actively seeking to enhance operational efficiencies, expand market share, and acquire AI/ML and Hyperscaler expertise while broadening their digital transformation efforts. To achieve these goals, they are actively pursuing promising private companies and Private Equity portfolio assets that can fuel their inorganic growth journey.

The Technology Services sector has demonstrated remarkable resilience, recording the highest number of deals in value as investors capitalize on emerging M&A trends. Early indicators suggest a resurgence in mega-deals and cross-border deals across the broader market, a trend projected to continue in the coming months and expand to encompass all sectors, including Technology Services.

Furthermore, sellers are strategically recalibrating their approach, prioritizing profitability amid margin pressures. This shift underscores the importance of aligning M&A strategies with operational objectives and highlights the need for a comprehensive understanding of the market dynamics shaping the Technology Services sector.

As the M&A landscape continues to evolve, the “Technology Services M&A Quarterly Report Q1 2024” serves as a valuable resource, offering insights and trends that empower leaders to make informed strategic decisions in the exciting landscape of M&A in 2024.

What you’ll find in the report: