Indian IT giant, Tech Mahindra (“TechM”), announced its acquisition of Com Tec Co IT Ltd (“CTC”), a European Digital Engineering firm, for € 310 Mn (USD 354 Mn) last week. Of this, € 210 Mn is upfront, with the balance € 100 Mn to be paid over the next four years, in the form of earn-outs as well as synergy-linked pay-outs. The deal is TechM’s second-largest acquisition (only after the scam-hit Satyam), and is among its most expensive acquisitions, being funded 100% through cash (with no plans to raise any debt).

The Digital Engineering market has witnessed a boom since the onset of the COVID-19 pandemic, with businesses trying to become antifragile by rapidly adopting intelligent and connected technologies. As a result, the M&A activity in the space has also risen with strategic players looking to fill portfolio gaps, as well as private equity firms finding long-term value in the sector. The increased demand for digital assets has had a positive impact on the sector’s valuation as well. Some of the recent marquee deals in the space include Hitachi’s acquisition of GlobalLogic for USD 9.6 Bn, Carlyle’s acquisition of Hexaware for USD 3 Bn, Advent’s acquisition of Encora for USD 1.5 Bn, BC Partners’ investment in Valtech at a USD 1.4 Bn valuation, Apax Partners’ acquisition of Infogain for ~USD 800 Mn, to name a few.

We believe that the CTC acquisition is a move in the right direction and will offer some unique advantages to TechM.

CTC’s acquisition will enable TechM to expand its delivery capabilities in Eastern Europe as the former has 720+ highly skilled IT professionals located in Latvia (85%) and Belarus (15%) – regions with significant tech talent pools. The acquisition is in line with the sector’s nearshoring trend, wherein large Service Providers are acquiring companies in Eastern Europe and Latin America to strengthen their delivery capabilities, while leveraging the unique aspects that the region has to offer – talent, cost advantage, and geographical proximity.

Zinnov believes that the trend of nearshoring will continue to grow in the coming years, with companies making acquisitions in the Eastern European and Latin American regions.

Suggested Read: Zinnov advised intive in acquiring SimTLiX in LatAm – a transaction following the nearshoring theme

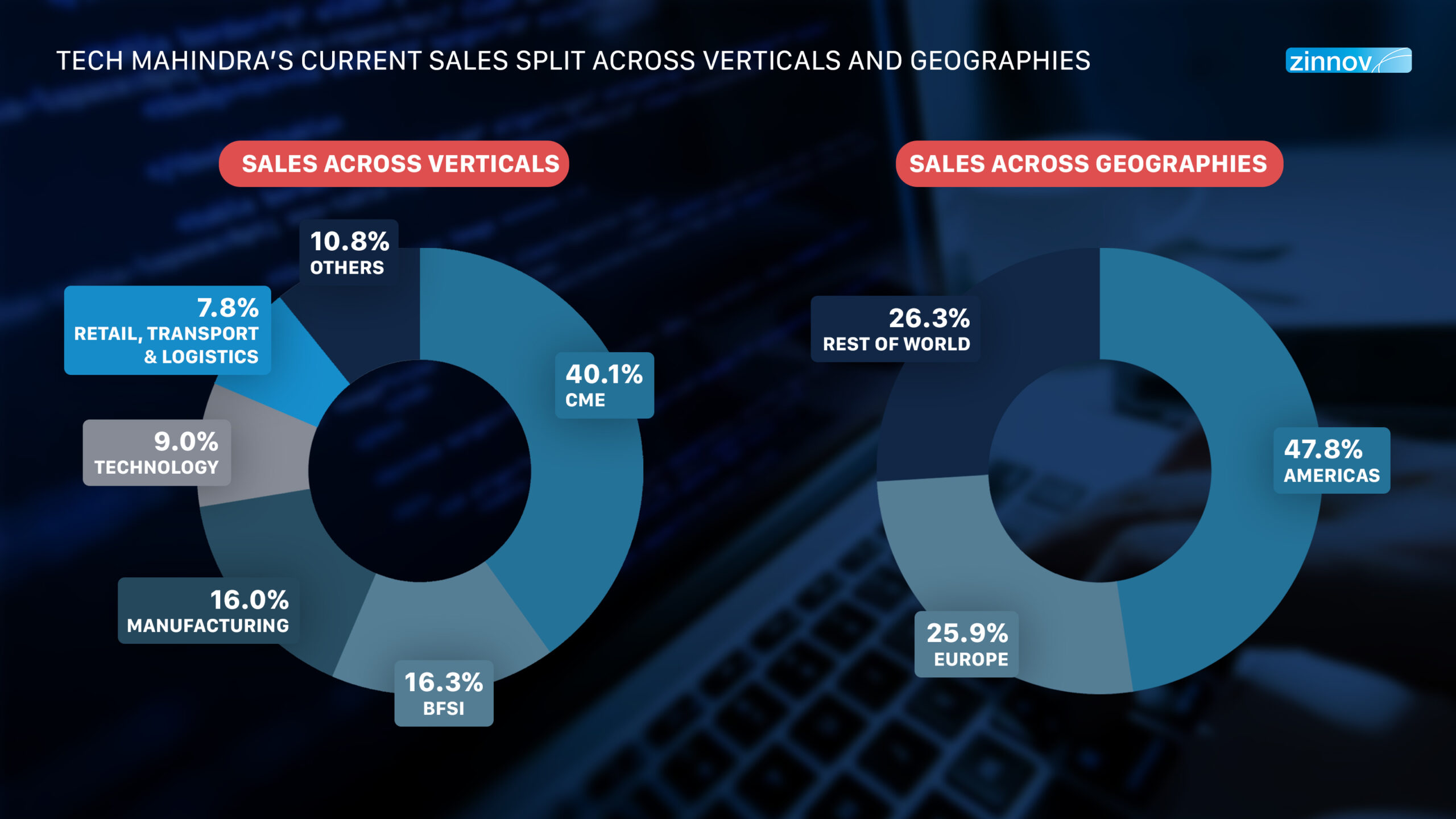

TechM’s most robust presence is in the Communication, Media, and Entertainment (CME) vertical, totaling a massive ~USD 2.4 Bn (or 40% of its annualized September 2021 revenue), with Banking, Financial Services, and Insurance (BFSI) a distant second at USD 961 Mn (or 16% of its annualized September 2021 revenue). The acquisition is expected to strengthen TechM’s insurance capabilities and double down on scaling its insurance business by leveraging the targets’ MOATs and disruptive business models.

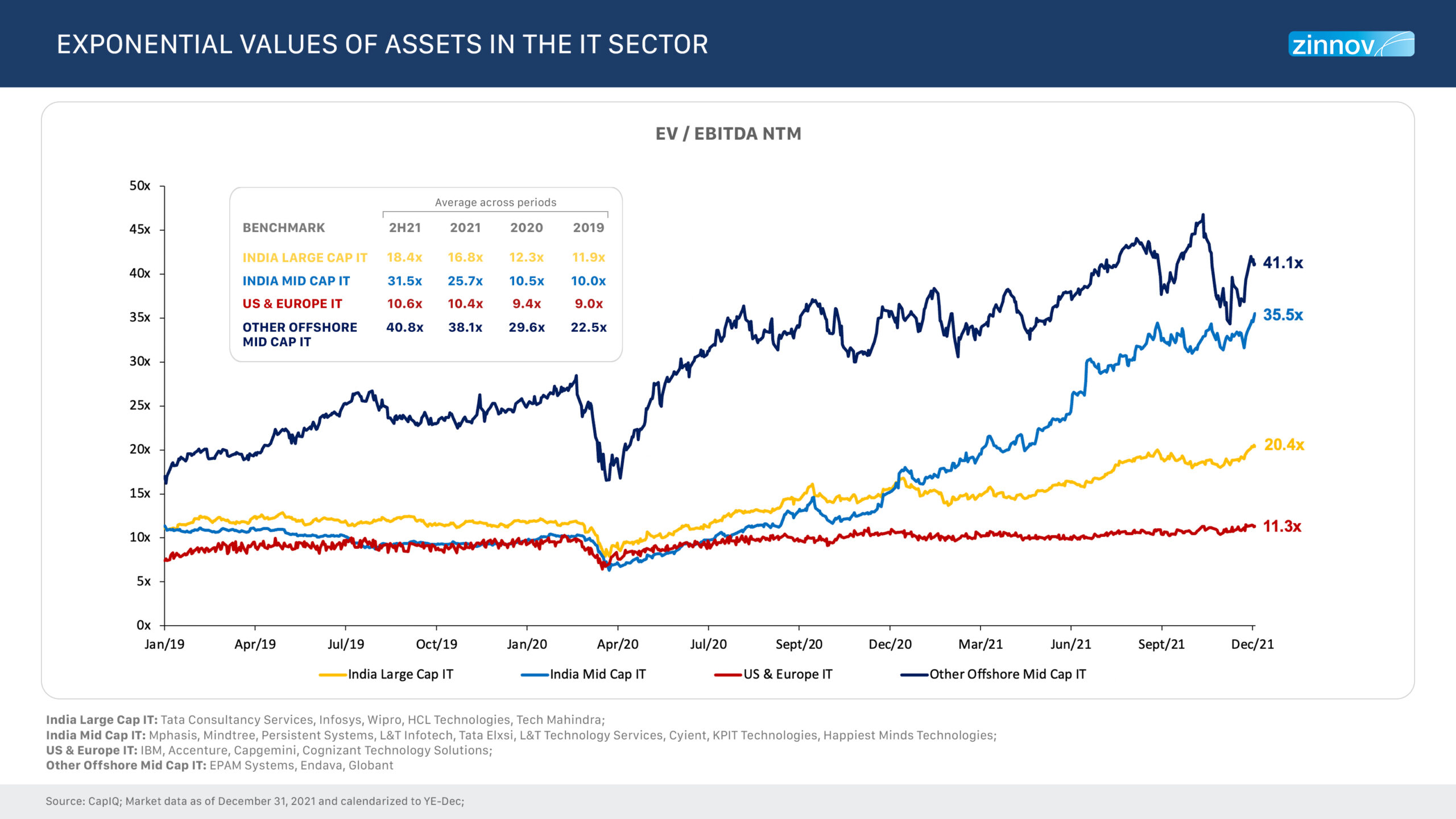

CTC is valued at ~4X EV/Sales – one of the most expensive deals by TechM. Given the rise in valuations across the sector since 2019, we believe that the valuation levels are broadly in-line with the current industry trends. Moreover, CTC has also reported strong revenue growth of 40% CAGR over the period 2018-20 and has industry-leading EBIT margins. TechM management believes the deal will be accretive on EPS (earning per share), FCF (free cash flow), and ROE (return on equity) basis. Also, there is no seasonality in the business (hence, no fluctuations in the earnings across quarters or years), and the attrition rate is also in single digits, which is a big positive in the current environment.

However, CTC derives ~60% of its revenue from a single client, and its strong revenue growth has only been in the last three years.

The Tech Mahindra-CTC acquisition has received mixed response from the Street. It is a marked pivot from the IT giant’s M&A approach so far, to a BUY approach from a BUILD approach. Coupled with the fact that integration of larger acquisitions is a bigger challenge, the question then becomes – will it move the needle for TechM, significantly? With CTC revenues less than 2% of TechM’s revenues, the deal is not significant for the overall business, and hence, the market reaction has been subdued.

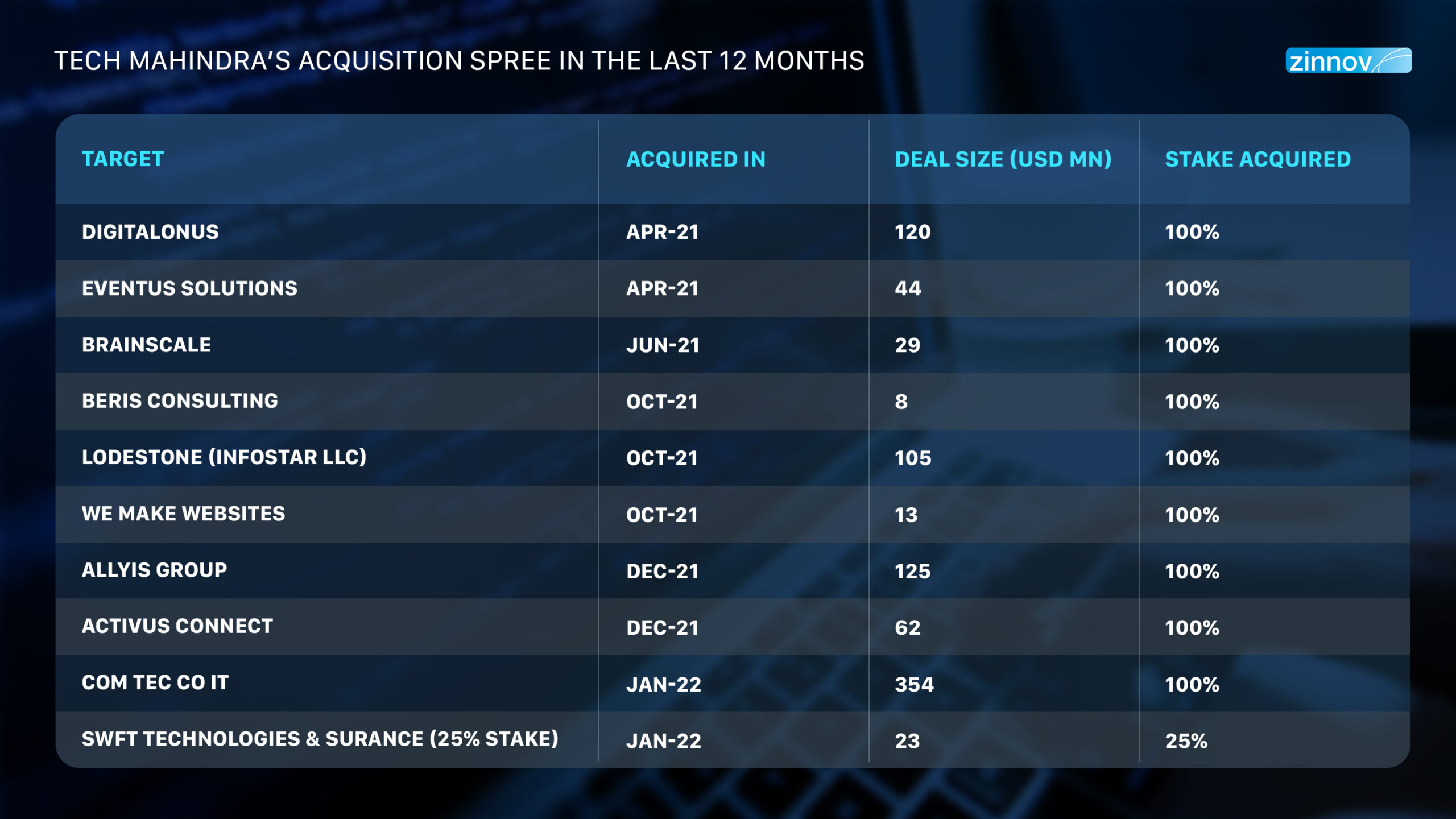

However, TechM has been on an acquisition spree, taking control of ten companies in the ten months of FY2022 alone, with a cash outlay of around USD 880 Mn, which is much higher than in the last few years.

The profile of acquisitions has significantly improved since 2017-18 though, with margins comparable to TechM’s average margins, and in high growth areas. The market, however, seems to have some concerns with the pace of the acquisitions. Hence, going forward, we believe that TechM should focus on opportunistic and strategic acquisitions to build capabilities and address portfolio gaps while prioritizing the integration of its acquired businesses.

While any acquisition comes with inherent business, execution, and integration risks, we believe that the CTC acquisition is a step in the right direction for TechM. The deal allows the IT giant to fill gaps in its digital portfolio, strengthen its capabilities in the insurance and reinsurance sectors (which are undergoing significant transformation), and gain access to some of the attractive nearshoring markets in Europe – Latvia and Belarus. We expect the recent acquisitions to generate long-term results for TechM, if integrated well.