|

|

Against a backdrop of rapid technological evolution and market consolidation, the Technology Services sector stands at the cusp of what could be its most dynamic M&A cycle yet in 2025. Drawing on insights from industry analysts, veteran dealmakers, and our seasoned M&A advisory team—which has helped execute multiple deals in Technology Services sector—we see several transformative forces converging to reshape the deal landscape ahead.

So, what’s shaping the M&A playbook for 2025? From AI-fueled dealmaking to the growing role of private equity, here are the 6 key trends that will define the year ahead.

Looking ahead to 2025, Technology Services M&A is expected to maintain its momentum despite broader market uncertainties. Our experts project sustained interest from both strategic buyers and Private Equity (PE) firms, driven by an urgent need for digital transformation capabilities and emerging technology expertise.

Corporate buyers are actively seeking acquisitions to address technology gaps, scale operations, and enhance vertical and regional capabilities.

“Companies are no longer just buying for scale – they’re buying for transformation,” notes Anand Kalra, Principal, Zinnov.

Cross-border activity is expected to surge in 2025, as global firms seek to expand their footprint in untapped markets and diversify their revenue streams.

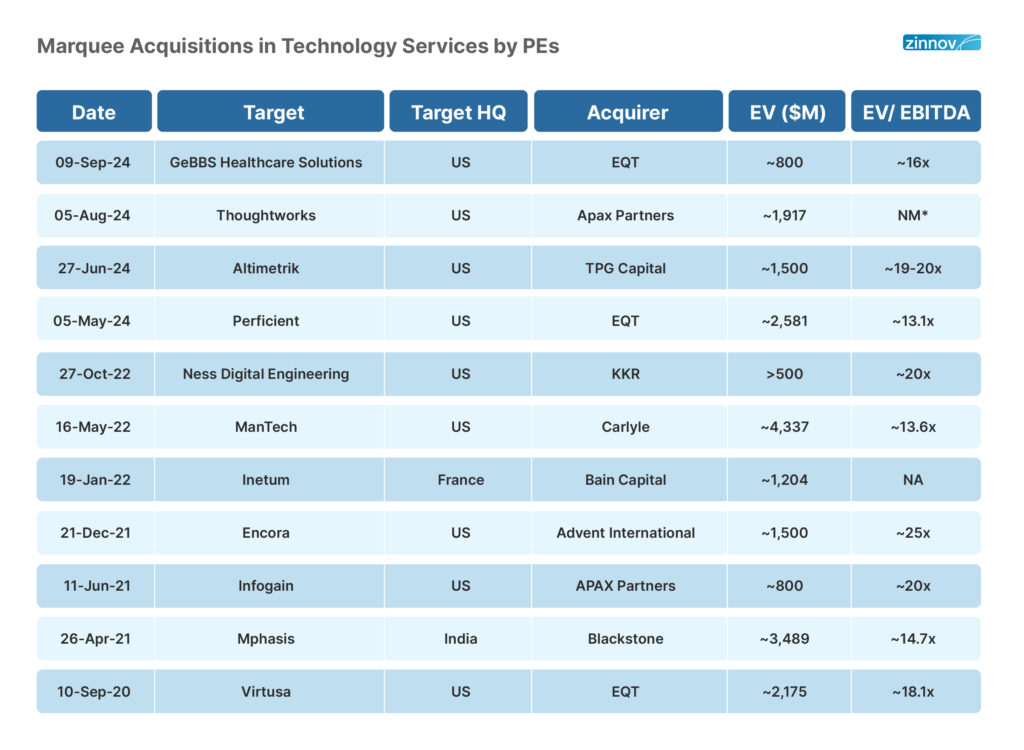

The days of sky-high valuations that characterized 2021-22 appear to be giving way to more sustainable multiples. Deals will continue to close predominantly in the mid-to-high teens range throughout 2025, maintaining the shift from the >20x EBITDA multiples common in 2021-22. This moderation reflects a significant market recalibration, with seller expectations adjusting to the current growth environment and buyers exercising increased discipline in their valuations.

Key market indicators—including the anticipated stabilization of interest rates, steady economic growth projections, and narrowing bid-ask spreads—signal a more predictable deal-making environment for Technology Services M&A in 2025. However, they emphasize that strategic assets with unique differentiation in AI, Data, and Analytics could still command premium multiples, bucking the broader trend.

The deal landscape in 2025 is further shaped by evolving ecosystem dynamics. While Hyperscaler-focused deals continue to dominate, there is a steady uptick in acquisitions of niche System Integrators offering services around growing platforms like Salesforce, Oracle, and SAP. This diversification reflects the maturing market’s appreciation for specialized capabilities.

PE firms are positioned to play an increasingly pivotal role in M&A through 2025, armed with unprecedented levels of dry powder. Private Equity firms have been aggressive in acquiring the Technology Services assets and we believe the trend will continue in 2025. The focus in 2025 will remain two-pronged: pursuing new platform acquisitions while simultaneously executing bolt-on deals to strengthen existing portfolio companies, particularly in high-growth verticals such as Cloud Services, AI, and digital transformation.

Adding another dimension to the 2025 landscape, we anticipate that PE firms will also drive the supply of assets in the M&A market. A substantial wave of exits looms on the horizon as numerous technology services businesses acquired during the pandemic period approach their investment maturity. This timing confluence is likely to catalyze increased deal flow and create new market opportunities in the coming year.

The AI revolution continues to reshape acquisition strategies for 2025. Companies with expertise in Generative AI, Large Language Models (LLMs), and advanced analytics are emerging as prime acquisition targets.

The adoption of Generative AI and Large Language Models (LLMs) has accelerated the need for specialized AI expertise, including Predictive Analytics, Automation, and Decision Intelligence Platforms. Data integration, governance, and advanced analytics remain high priorities as organizations strive to harness actionable insights from their data assets.

Our experts are tracking heightened acquisition interest in companies delivering AI-enhanced solutions across key verticals. In the Healthcare sector, firms specializing in AI-powered diagnostics have become particularly attractive targets, while Automotive Technology companies developing Autonomous Driving Solutions are drawing significant buyer attention. The BFSI sector continues to attract strategic interest, especially for companies with proven AI capabilities in Fraud Detection Systems. The appetite for these acquisitions is further amplified by growing domestic demand for Cloud, AI, and Cybersecurity solutions, with China and India emerging as key drivers of regional M&A activity.

Companies that provide digital transformation consulting and implementation services will continue to be attractive with key areas including Low code/No code Development Platforms and Business Process Automation.

Four sectors are emerging as hotbeds for M&A activity:

With the shift in global leadership in 2024 and early signs of easing tensions in the Middle East and Russia-Ukraine, Central and Eastern Europe (CEE) is emerging as a key focus area for Tech Services M&A in 2025. The region’s combination of skilled talent pools, lower operating costs, established innovation hubs, and strategic nearshore opportunities makes it increasingly attractive to global acquirers seeking to expand their delivery capabilities. Our M&A advisory experts predicts this region will see significant deal activity as companies look to establish and strengthen their European presence.

As the technology services sector continues its evolution through 2025, strategic M&A will remain a critical lever for growth and transformation. The convergence of private equity interest, imperative for AI capabilities, and emerging market opportunities presents both challenges and opportunities for industry participants.

Success in this dynamic landscape requires deep sector expertise, strategic foresight, and proven transaction experience. Having been in the industry for more than 20 years, advised on numerous landmark technology services transactions and maintained a proven track record in both buy-side and sell-side mandates, our team stands ready to help organizations navigate these complex waters—whether it’s refining M&A strategy, evaluating potential targets, or executing transformative deals.