|

|

“UK recession threat is now almost 50-50 for economists.” – The Economic Times

“US stocks dive as bond yields flash recession warning and investors brace for inflation reading.” – Business Insider

“S&P 500, Nasdaq slip on recession worries.” – Economic Times

“Nomura cuts 2023 India GDP forecast to 4.7% amid recession fears.” – Business Standard

“Oil sinks further below USD 100 as recession risk spooks market.” – Mint

Chaotic stock markets, increasing interest rates, and rising inflation have left one question in everyone’s mind: Are we in a recession? Major banks have changed their forecasts to reflect the increasing possibility of an economic downturn. Goldman Sachs has increased the probability of a recession in 2023 at 30%, up from 15% while Bank of America predicted a 40% chance of a recession in 2023.

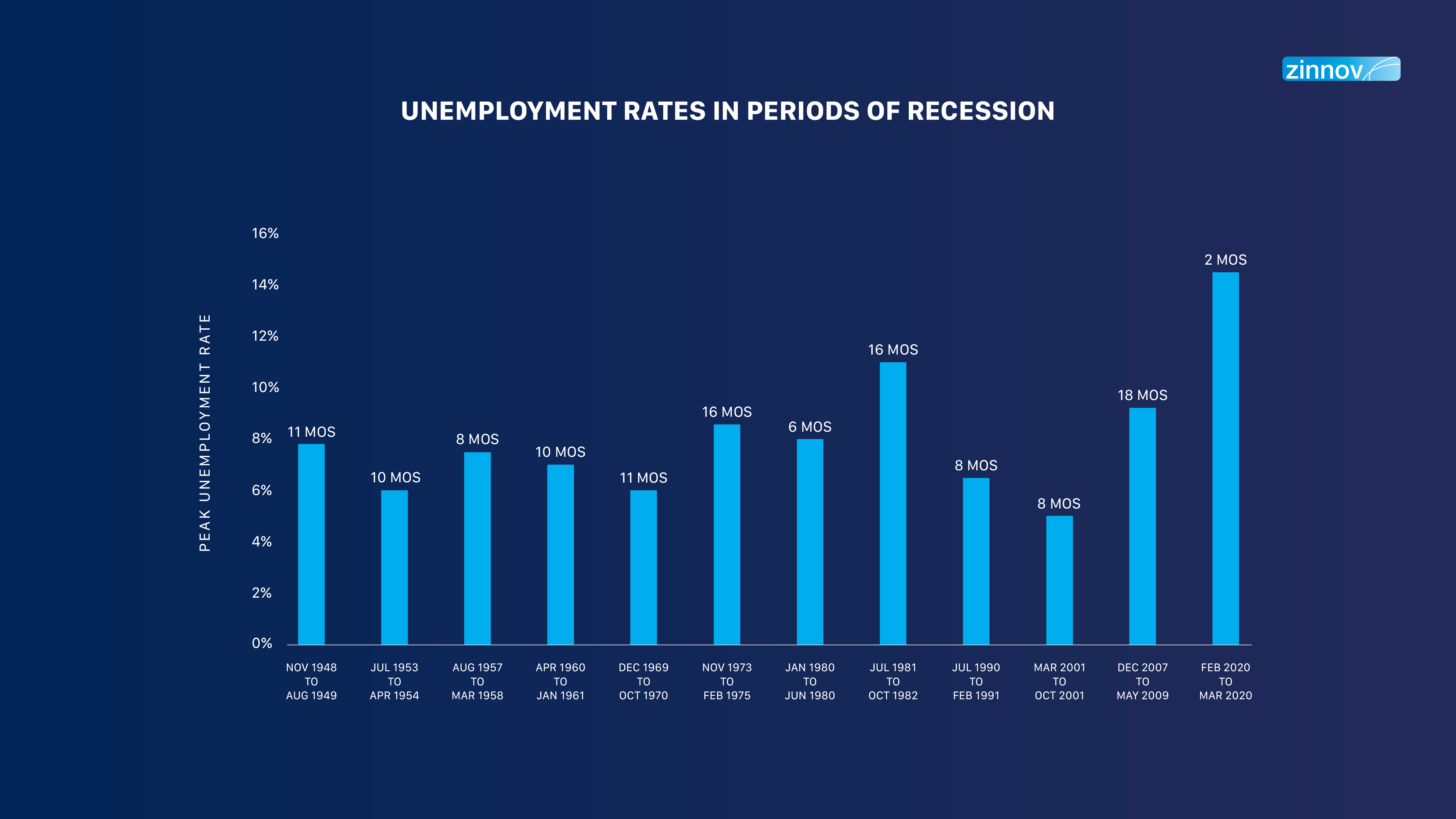

The US Federal Bank, in attempt to curb inflation (which is rising at its fastest pace since 1981), is trying to slow the economy down. Fed has recently announced its biggest interest rate hike of 75 bps since 1994, and more hikes are expected this year. This, coupled with the stock market’s decline (almost the worst first 6 months of the year since 1970), meltdown in crypto, mass lay-offs in anticipation of a downturn, and plummeting consumer confidence pose a serious threat to the health of global economies.

While the past recessions such as the dot cum burst of 2000-01, or the Great Financial Crisis of 2007-08 were led by debt-related excesses in the Internet and Housing Infrastructure markets respectively, the current one is majorly led by excess liquidity owing to COVID-led fiscal and monetary stimulus contributing to inflation and driving speculation in the financial assets. This means that if it does come to pass, a recession today is likely to be shallower and less damaging than other recent downturns.

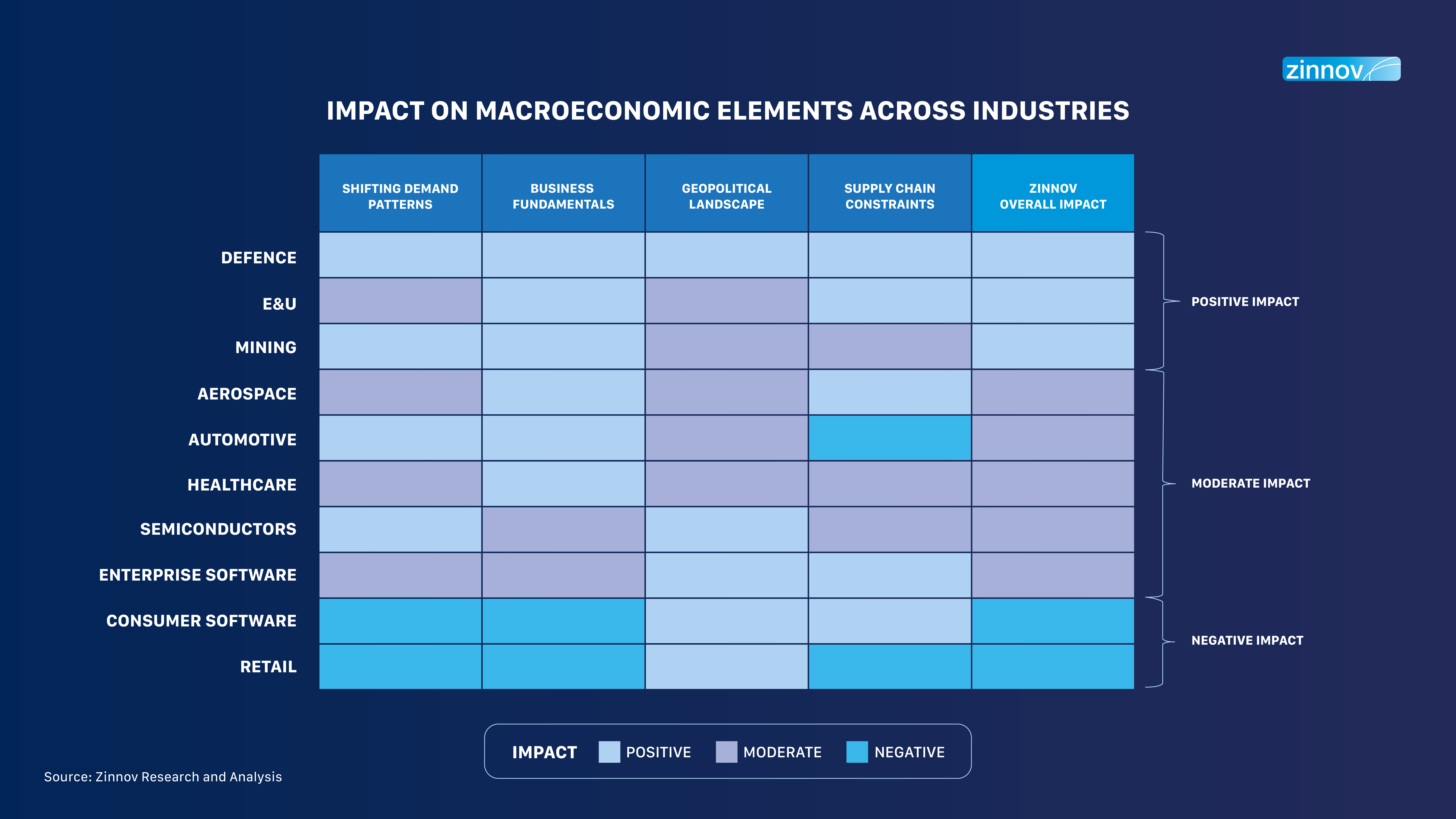

Shifted demand patterns (due to changing consumer sentiments), uncertain geopolitical landscape, supply chain constraints, changing business fundamentals – all such macro factors shall impact enterprises across verticals.

Potential US and global recessions pose threat to India’s IT growth for the ongoing FY, as a chunk of Indian IT’s revenue comes from the US. The US market contributes anywhere between 40% to 75% of the revenues earned by Indian IT companies. Tata Consultancy Services, Infosys, Wipro, HCL Technologies, and Tech Mahindra, which are the top five firms, have more than a 50% exposure to it.

JP Morgan analysts have downgraded India’s IT services industry to “underweight”, citing soaring inflation, supply chain issues, and the hit from Ukraine war will bring an end to the growth boom the industry enjoyed during the pandemic. Nomura has downgraded IT companies over declining revenue as well. Additionally, the markets have reacted. Indian IT stocks have seen a sharp correction in 2022. Nifty IT Index has plunged around 25% so far this year. In particular, May turned out to be bad for IT stocks.

However, with companies moving towards digital innovation, even with the reduced IT budgets, the sector may not witness a huge downturn for a long time. IT companies see the pipeline for digital transformation deals staying strong for several years. Tech focus areas such a Meta, 5G, Digital Thread, and Cloud/AI are driving the Digital Engineering spend. While expenses on experimental projects in AI and AR/VR might reduce, focus on core offerings such as cloud ERP, Mobile Development, Analytics, and Outsourcing is expected to increase supporting the sector. Also, unlike in the 2000s, Indian Tier-I IT services firms are now strategic partners and not just glorified staffing providers who will be the first to bear the brunt of cuts. Inflation-led wage-hike pressure in the US and Europe will also lead to IT jobs continuing to move to India. Attrition, which is a big problem faced by Indian IT also gets resolved as employee resignation reduces.

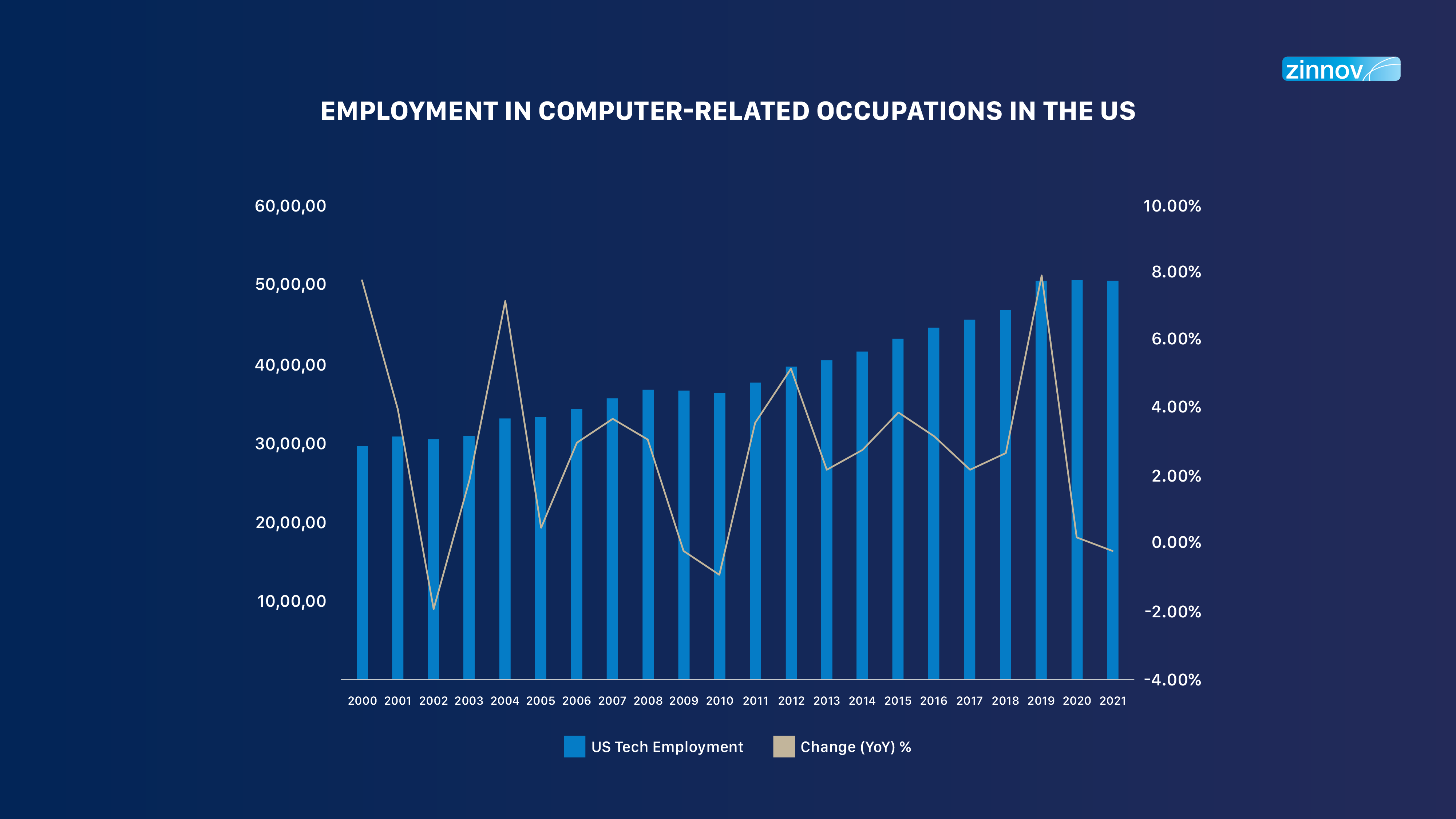

Historical data also suggests that IT spending seems recession-proof, with US computer-related employment down by just 0.3% over 2008-09, and 0.8% over 2009-10. For instance, the US employment in computer-related occupations has increased from 2.03 million jobs in 1997 to 3.54 million jobs in 2007, 4.56 million jobs in 2017, and 5.07 million jobs in May 2021.

Post the 2008 crisis, worldwide IT/ITES grew by 12%, the highest among all technology-related segments. Hardware spend had also grown up by 4% from USD 570 Bn to c. USD 594 Bn in 2008.

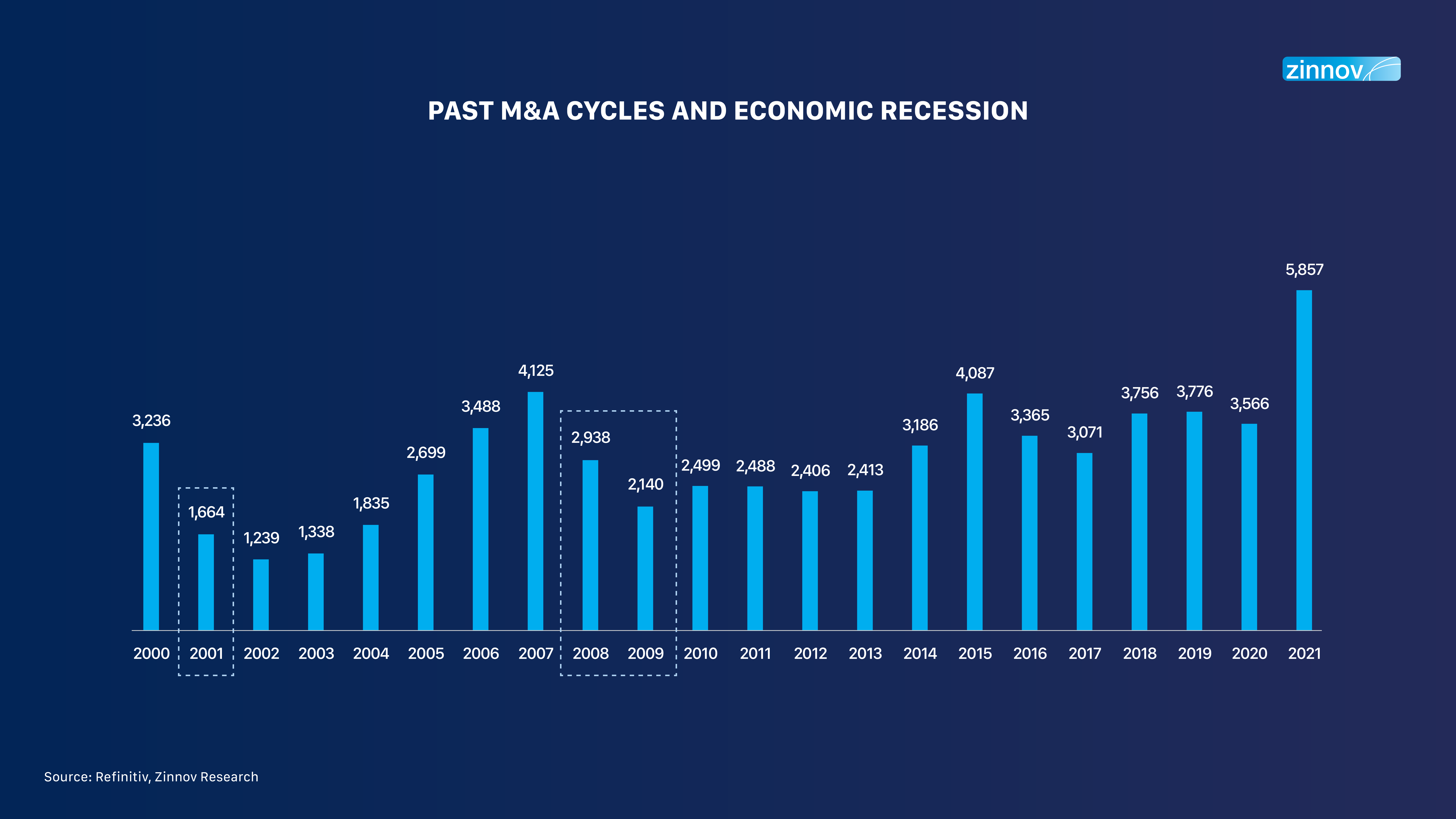

Historically, M&A activities and dealmaking have always plummeted in an economic downturn. Evidence from the last financial crisis from late 2007 through early 2009 shows that companies that made significant acquisitions during an economic downturn outperformed those that did not.

The recovery, beginning in 2009 was very much U-shaped. That is, it took more than five years for deal volume to recover to average pre-crisis levels, and the deal value never quite recover completely until 2021. The story regarding deal multiples [EV/EBITDA] was somewhat different, with much more of a V-shaped recovery. Deal values plummeted from an average of 10.8x in the three years before the 2008 crisis hit, to as low as 6.5x in 2009, before rebounding to the 10-year average of 11.6x by 2019. [Source: HBR]

In H1 2022, M&A activity has slowed down from its record-setting 2021 pace, with economic headwinds stunting deals. Global M&A deal activity took a beating with total deal values tumbling by c.22% and deal volume reducing by c.25% on YTD basis. However, setting aside this decline, the deals are still higher than the pre-pandemic levels.

While correction in the broader technology space has deterred M&A activity in the sector globally, IT and ITeS sectors continue to lead the M&A front, (as has been the case in each of the last 29 months), and as evidenced by the fact that roughly 1 of every 5 deals based on the total number of deals emerged in the technology space. This underscores the presence of many megadeals and the impact of digital transformation as a key enabler in driving such deals.

While many of the factors that led to record breaking M&A in late 2021 and H1 2022 remain influential even for the latter half of the year – particularly ESG, and need for technology to digitise businesses – the new inorganic growth approach requires fresh focus in the current uncertain scenario. Due diligence needs to be looked at with multiple simulations around inflation, interest rate, growth, and employment & wages scenarios. M&As are expected to be vital in setting out firms’ corporate growth strategies in the remaining half of the year, with lower valuation levels providing ample opportunities for CXOs to reset and reassess their strategic priorities and generate a healthy return on invested capital.

While we are not in a recession yet, there are definitive signs of an economic weakness emerging. While a recession might not be the real challenge for the IT sector, it will be critical for IT firms to balance between the revenue and the margin impact as pressure on the margins is expected to grow along with reduction in per employee revenue.