Automakers around the globe are taking substantial strides and already thinking ahead through investing in connectivity, electric cars and self-driven cars. However, there’s still a long way to go for the industry to achieve a globally distributed R&D footprint. The world’s largest automotive market in China has been a central attraction for global automakers for sales, but there exists a plethora of R&D potential in this region which remains unexplored. With strong growth in engineering talent located in Shanghai, Beijing and Guangdong, China is poised to become an auto R&D hub. True, that the traditional engineering hubs like Michigan, Japan and Western Europe have strong R&D infrastructure. However, it’s no small wonder that challenges such as skilled talent hiring and new regulations for pollution norms remain a top focus for R&D decision makers as they realise that a localised R&D system cannot sustain in a long run.

It begs the question: How to cope with the new R&D challenges? Firstly, the saturating engineering talent in western countries is leading to high R&D cost of innovations like Electric Vehicles. Secondly, to offset these costs levied by EU pollution standards, European automakers have made some efforts by increasing their presence in Eastern EU countries like Poland and Romania. But the limited engineering capability of these regions has failed to deliver globally.

To answer this innovation logjam, automakers are expanding their R&D presence to scalable locations like India and China. The engineering capability of China is not as strong as traditional hotspots like Michigan yet. However, through our Global R&D spenders analysis at Zinnov along with data extracted from the Global Engineering Insights Platform (GEIP), we take a closer look at the maturing automotive R&D ecosystem in China, with increasing investments in cities like Shanghai and Beijing. Asia has observed a tremendous automotive R&D growth of 75% since 2008, putting it ahead of North America, Europe and Japan. The major share of this R&D spend goes to China, reaching $12 billion in 2015.

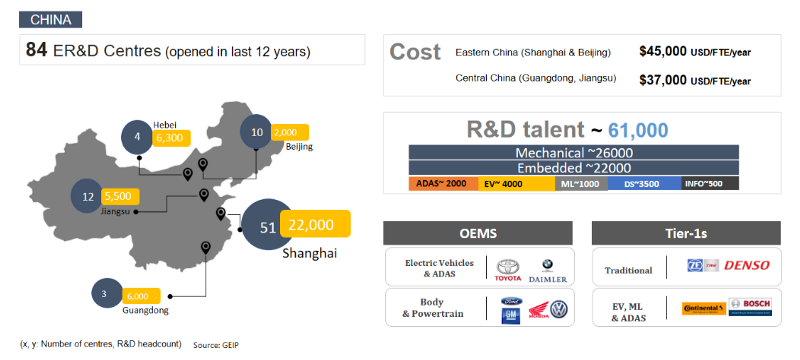

The Automakers in China continue to embrace their mature global R&D capability across traditional areas like body engineering, powertrain and infotainment. In a race for agile process development through digital transformation they are augmenting their traditional areas with local software and embedded talent. There is a significant shift in the centre of gravity of the industry’s R&D activity towards China with a total of 84 centres establishment in last 12 years. Predominantly these MNCs are shifting their R&D decision making centres i.e. the Hubs and Satellites closer to Chinese market. This is evident from the fact that 8 Engineering Hubs and 39 Satellite R&D centres were set up in China during this period.

Figure 1

Figure 1

Given the promise of such a disruptive ecosystem, automakers are investing heavily in China. GM in China has set up an Advanced Technical Centre (ATC) which is similar to its facility in Detroit and has hired 300 engineers in Shanghai. This will support GM’s operations around the world. European peers like Daimler has employed nearly

100 engineers for its technology focus on advanced machine learning and driver assistance in Beijing. BMW has set-up a technology tracking centre in Shanghai to keep a close eye on disruptors with a high focus on identifying and testing prototypes and transfer those to production if viable. In past 3 years, automakers have laid the R&D pipeline into Tier-2 cities like Guangdong and Jiangsu. This is due to high cost pressure and competition in Tier-1s for new age software skills from Chinese Internet companies like Baidu & Tencent. Average salary in Tier 2/3 is 20–30% less as compared to Tier-1s. Bosch and Continental have highly leveraged engineering talent out of these low-cost locations. Ford has a scaled R&D centre in Jiangsu with nearly 2000 engineers working on body and powertrain engineering.

Figure 2

Figure 2

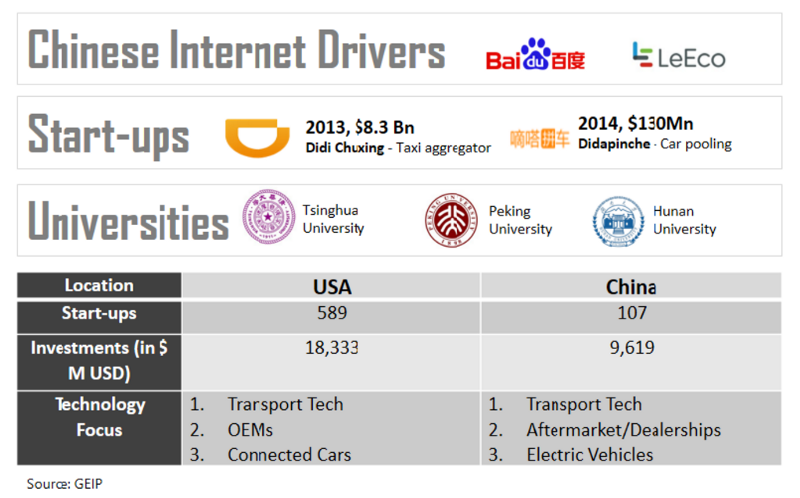

The ecosystem led by start-ups, universities and accelerators has opened new business opportunities such as alternative ownership and ridesharing. China stands second only after US for automotive start-up investments and has always been at the forefront of new age technologies. Internet and tech giants like Baidu and LeEco are investing heavily in Electric vehicle, mobility and driver assistance. Baidu is determined to develop its own Electric car. LeEco has not only invested in US based Electric vehicle start-up Faraday Future but has also partnered with Aston Martin and unveiled its electric concept vehicle in Beijing auto show last year. Ride sharing start-up Didi Chuxing books over 11 million rides a day and has significant R&D focus on using advanced machine learning algorithms for route optimisation. Apple’s $1B investment in Didi is well aligned with former’s data access strategy for self-driving cars, where the ride-sharing company is vital for mining millions of vehicle data point.

Automakers have taken notice and have broadened their engagement strategy with these disrupters through partnerships, accelerators, venture arms along with scouting through endeavours like hackathons. Last year, Daimler China’s CIO, Marc Lampe, announced a partnership with Plug and Play, to co-invest in Chinese start-ups. GM has recently invested in Chinese start-up Yi Wei Xing Technology focused on car rentals. Others are sure to follow and in 2017, we expect more automotive start-ups will raise funds through OEMs.

Incumbents are also running mentorship programs for the young graduates coming out of universities to help them commercialize new age technologies. To expand their core capability, these players have high hiring focus from Tier-1 universities like Peking and Tsinghua University in Beijing. Toyota Motor and Tsinghua University conducted a joint research on air pollution, wherein Toyota’s hybrid vehicle technology, provided data related to

exhaust emissions to Tsinghua. PACE which is an alliance between GM and other multinational corporations established its centre in Hunan University in 2015, collectively donating $280M worth of software and hardware resources. These companies have also hired top Chinese leaders, experienced in automotive R&D to leverage their close university connects.

There are some roadblocks for the global data platform players in China. The regulatory conditions in China protects local defence companies to use proprietary navigation systems, to compete head to head with US in areas such as the connectivity and Industrial IoT. Though governed by local regulatory and safety requirements, automakers in China have high incentives from the government to commercialize innovations in early stage. For example, consider how western companies take products to market through regressive testing and revalidation of the product. Unlike West, Chinese government is changing the equation by supporting these automakers to test concepts directly in market following a data driven R&D approach. Can this R&D policy disrupt the automotive industry? It depends on how automakers react.

Amidst a large automotive market, a good education hotbed and an innovative policy which is actively shaped by the government, automakers should leverage this new R&D paradigm on the other side of the world to build the “Car of the Future”.