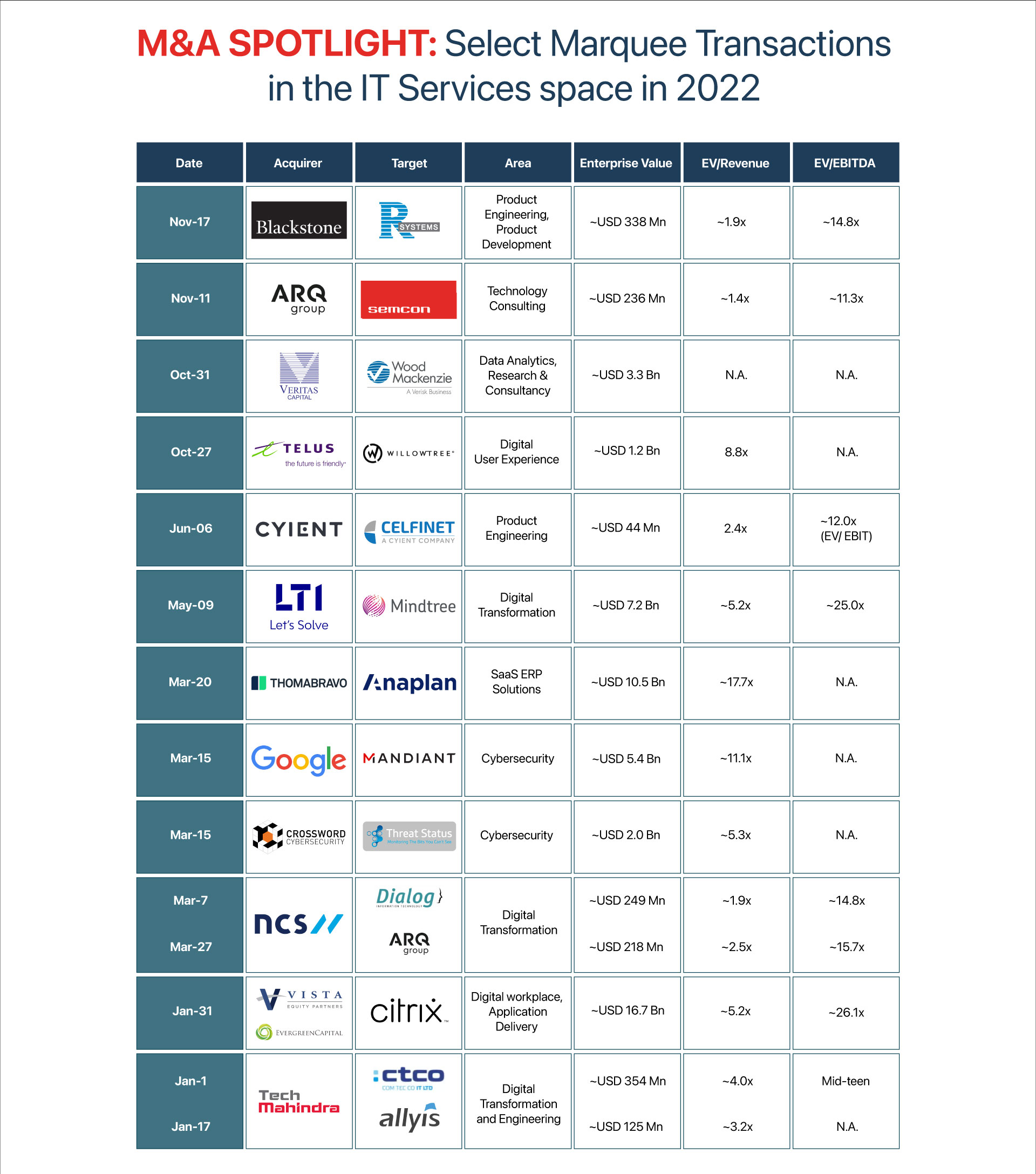

The volatility that the stock markets have shown in the recent times has left everyone with one big question: Is the valuation correction in public markets going to be followed by a correction in the private markets?

The liquidity crunch-led stock market decline in the initial half of the year was the worst that has been seen since 1970. This liquidity crunch is an aggregation of multiple factors—global supply chain disruptions owing to lockdowns, the Russia-Ukraine war, meltdown in the global tech stocks, and spike in inflation and consequent hike in interest rates. This, along with a forecasted slowdown, increasing interest rates, crypto meltdown and mass layoffs are leading everyone to question the sky-high valuations that the start-ups have enjoyed in the last decade. While the public markets have corrected, deals continue to happen at higher multiples in private markets – Will the same trend be followed in private market remains to be seen.

Happenings in the U.S. economy, and market shifts in Europe will influence the growth outlook of one sector the most – the technology space. With so much macroeconomic uncertainty, budget realignments are bound to happen . The focus is now shifting towards cost cutting measures rather than discretionary IT spends. This is going to impact the overall revenue growth trajectory and valuations, in the near-medium term for the sector.

The move to cut costs will also impact valuations of assets in the market at large. Publicly traded companies usually tend to enjoy much higher Enterprise Value multiples than small privately held companies due to scale, reach, stability, and lesser risk associated with them. While the public market multiples have already corrected, the private companies’ valuations should follow in the next 2-4 quarters.

According to a report by Venture Intelligence, from 2018 to 2022 (till Oct), around 105 start-ups had attained the unicorn status in India, but this has now reduced to 84 active unicorns due to various reasons. This is not the fault of start-up founders nor investors. The root cause is deeper, and can be stretched back to the U.S Federal Reserve’s strategies.

In the last one or two years, we have seen that companies were valued very high . While there was Quantitative Easing taking place across the world, banks had taken an expansionary stance. In monetary infused world, especially post COVID, the US Federal balance sheet had expanded to USD 9 Trillion. Automatically, this would have eventually seeped into valuations of companies, leading to higher enterprise values.

However, banks have now started increasing interest rates to tame inflation. This automatically means the prices for other assets are falling. Higher interest rates lead to changed investor behavior – they now receive a higher return on a risk-free investment. Higher costs of capital for companies , is another consequence of higher interest rates.

Earnings are beginning to decline, which makes asset prices decline. This also causes the interest coverage ratio to decline, making the company appear riskier because it has less cash available to cover its interest payments. If this increased risk is sufficiently high, it might cause investors to demand an even bigger risk premium, lowering asset prices even more.

A correction in valuation might actually turn out for the better in the longer run – it keeps a check on run-away valuations and avoids bubble formation. The other reasons are:

Ultra-high valuations build unsustainable businesses rewarding highflying yet unproven strategies. This distorts rational markets and forces traditional companies to poor decision-making in order to compete

Traditional companies have struggled to attract and retain younger generations of tech-savvy managers and executives due to the exorbitant compensations being offered by VC-funded start-ups. In a cash-conscious world, this trend will stop, attracting better talent

While the unsustainable businesses exit, it will create space for incumbents to become disruptors themselves

While there has been a downgrade in most of the IT companies’ stocks, it is more of a valuation reset rather than growth reset. Though the brokerage houses have downgraded their target prices, none of them has downgraded their growth forecast for the upcoming years, denoting none of the medium to long-term drivers for IT growth have gone away – this is a relief.

While there is no doubt that the correction in the broader market is definitely on the cards, and there is change in funding sentiments but it is more of a correction driven by tightening liquidity and thus, won’t affect the valuations of good assets that are in their growth-stage and have low burn models.

Having said that, there is one major change that could occur. Buyers could however become more selective, and there won’t be a rush for every type of asset, like last year. Growth won’t be the only criteria for the upcoming investments; the companies, themselves pressured for margins, will also look for profitability in assets. PE and VCs will still be aggressive, but with limited capacity – the demand will be limited to quality assets.

Traditional companies and tech giants will still need to invest in infrastructure to be future-ready. Now is the time for the companies to prepare and build a foundation of digital business agility, so they can quickly and effectively adapt to the upcoming market turbulence. Digitization of IT processes, building digital platforms, upskilling workforces, and incorporating digital transformation into their strategies is the need of the hour.