With digital becoming the order of the day, several technologies are now coming of age and transforming businesses like never before. Blockchain is one such technology that is poised to revolutionize the way we operate today and has shifted from being experiment-centric to business case-centric. Blockchain’s financial use cases are probably the most mature, in terms of adoption and implementation. However, with technologies like IOT becoming more prevalent, the cost of end-point devices becoming cheaper, the rise of edge computing, and with the increasing proliferation of platformization, the viability of blockchain becoming a crucial component of end-to-end use cases and applications has increased. It’s safe to say that Blockchain is approaching its tipping point.

Often, blockchain technology is used synonymously with bitcoin and vice versa. But there’s more to blockchain than just bitcoins, and here are a few use cases that have gained ground recently:

Here, individuals generate their own renewable energy and then share the excesses with their local community. The energy is tokenized and traded in a community through a virtual microgrid, without any intermediary.

Timeshare is a business model where a property has divided ownership or usage rights. Blockchain is poised to disrupt this business model by enabling disintermediation, transparency, and security. Individual owners can swap, rent, and sell their properties without the need for middlemen or exchange agencies. A not-for-profit organization is already using blockchain and digitizing its real estate assets.

With the advent of FASTag/RFID readers, toll fee collection has the potential to become even more robust and secure. The multipartite BOOT (Build-Own-Operate-Transfer) model, if operated by combining camera analytics, IOT, and blockchain, can bring about operational excellence.

These are only a few of the blockchain use cases that are gaining traction, and the industry as a collective has only just started to scratch the surface. Enterprises are also increasingly partnering with blockchain experts to leverage the full potential of the technology.

A case in point is Migros, one of the major retailers in Switzerland. Migros, in association with TE-FOOD – a farm-to-table food traceability technology provider, launched the Blockchain-based Fresh-Food Track-Trace Project. The fundamental rationale behind the venture is to bring transparency, easier product recalls, and better supply chain control. Through the venture, Migros also wants to gain deeper insights into the end-to-end supply chain process for quick distribution as well as to reduce food wastage.

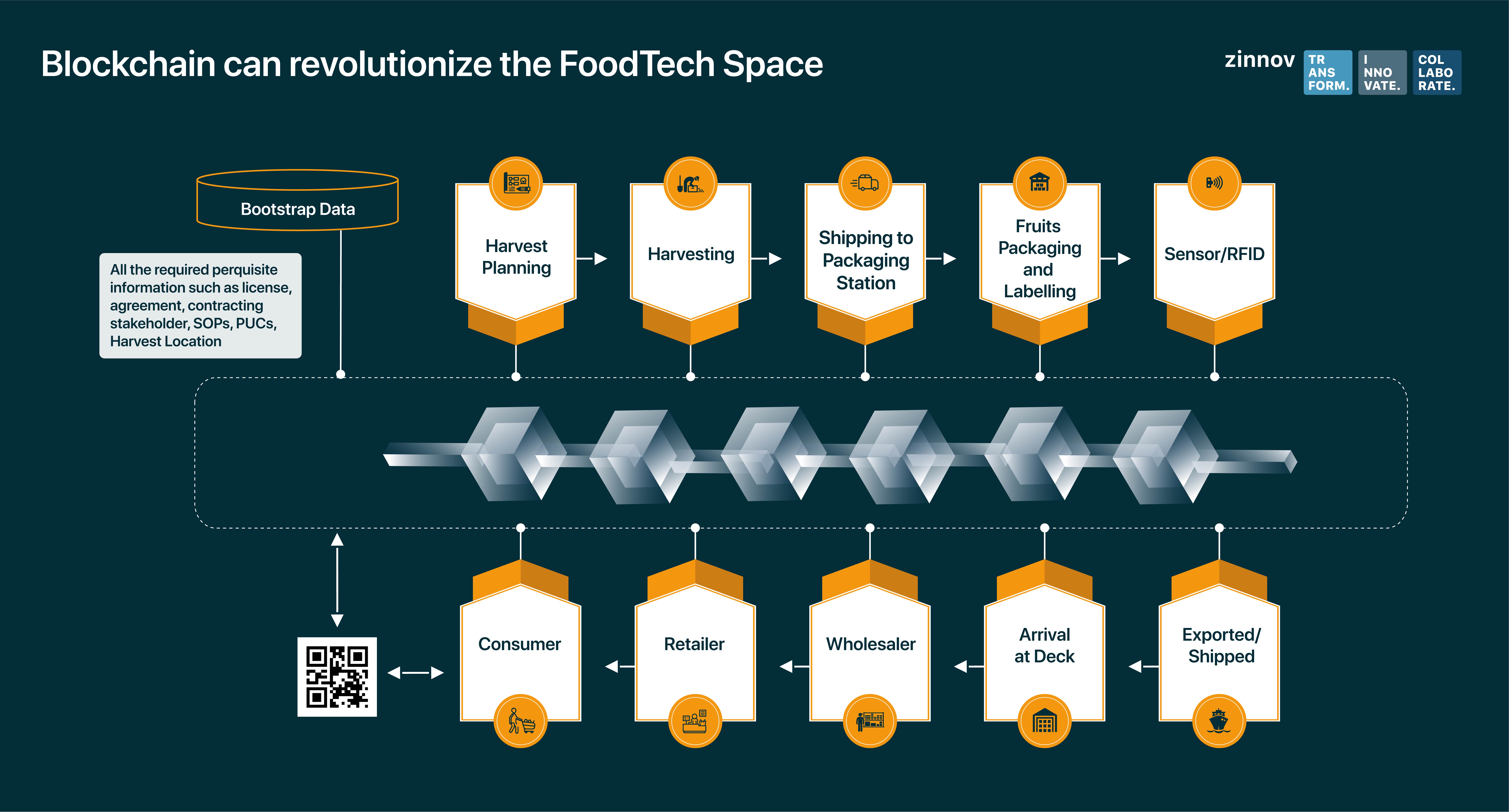

Let’s look at one of the foodtech/retail value chain use cases wherein Blockchain, along with IOT, has huge scope to make a much bigger impact on the entire value chain.

Consider an immutable digital platform connecting all the stakeholders in a fruit value chain, including Farmers, Logistics Service Providers, Produce Handlers, Brokers, Financial Institutions, Wholesalers, and Consumers. Each stakeholder, let’s say, has a node that allows them to enter information as and when they add value in the chain. When fruits are plucked and packed in a crate, information like the farmer code, fruit variety, and harvest date, along with details such as the use of fertilizers are captured against QR codes on the Blockchain. The logistics service provider picks up the crates, scans the QR code, and enters the shipment date, quantity, and destination, which is the fruit handling station.

At the handling stations, IoT devices such as temperature sensors, humidity sensors, penetrometers, etc., can record information on a real-time basis. Further, the product information can be recorded as it moves through the value chain and finally reaches the consumer through the wholesaler/retailer. Additionally, predefined costs based on quantity, storage time, destination, etc., can be recorded as the product moves forward in the value chain. Upon receiving the product, a consumer can scan the QR code that would take them to a webpage providing all the details about the product right from the orchard to the shelf.

What is clear from this use case, albeit, a utopian one, is that blockchain can enable a trust-based system that would not only boost consumers’ confidence but also benefit each and every cog across the value chain.

To reach this utopian scenario – which is not so far out – blockchain has to reach that tipping point. This can be accelerated when we find more use cases, build them from end-to-end, and deal with the impending challenges. For instance, in the above-mentioned use case, blockchain can be applied from the point of origin all the way to the point of sale. And in the process, it can compress costs for users, have a fairer price regime for producers, and eliminate wasteful practices in the value chain.

So, for a user, blockchain can enable better cost point, better quality, and increased trust. For a nation and governance bodies, it can enable sustainability and better health for people. For those within the value chain, blockchain can create more employment. However, while this recipe has all the ingredients ready from an emotional level, from an implementation aspect, there are some ground realities that don’t make this as viable as one would want. There are challenges like Internet connectivity, data and security, the concentration of workload in certain areas, orchestration of the process, ownership of the data, etc. Overcoming these challenges will be key in making an impact.

So, what is a tipping point? When a small input variable causes a significant output that is geometric in nature rather than arithmetic. With blockchain, even though there are things that are happening incrementally, we are heading towards a point when blockchain will be the new norm. It is safe to say that blockchain is on the threshold of becoming ubiquitous.