Generated for quick understanding

India’s GCC ecosystem is accelerating, with ~50 new centers launched in early 2025 and strong growth across both mid-market and mega GCCs. MNCs setting up in India benefit from mature ecosystems, deep tech talent, and supportive policies-making the country the preferred destination to build & scale next-gen global capability centers.

|

|

When ~50 new Global Capability Centers (GCCs) opened in India in just the first two quarters of CY2025, it reaffirmed what the world had already accepted by 2024 year-end: “India had become the GCC Capital of the World.”

And honestly, you can feel that shift in every conversation we’re having with global leaders this year.

The “Why India?” question, the one we’ve been hearing for a decade, is gone. In its place is a new one: “What more can we do from India?”

Bengaluru and Hyderabad continue to dominate new setups, together accounting for the lion’s share of 2025’s activity. (As I write this, five new GCCs are being set up in Hyderabad alone.)

Pune and NCR are close behind, expanding fast, especially across digital, product, and engineering portfolios.

And it’s not just the numbers that tell the story, it’s the nature of what’s being built. The Mid-market segment gained speed, setting up transformation-led centers with product ownership, while a growing set of large enterprises scaled into the Mega GCC bracket, running entire portfolios from India.

That’s what makes 2025 different. The foundation was already there; this was the phase when the ecosystem began to act like what it had become, a global catalyst.

With over 1.9 Mn professionals powering global engineering, AI, and product mandates, India’s GCC ecosystem reached a level of maturity in 2025 that few countries can match. But the real change wasn’t just in where the talent sat, it was in what that talent now represented: accumulated experience, institutional knowledge, and leadership depth.

Zinnov’s 5-Year GCC Landscape Report shows that global leadership roles from India have grown at a ~40% CAGR over the past five years, reaching 6,500+ roles in 2024, including 1,050+ women leaders. At this trajectory, that leadership pool is projected to surpass 30,000 by 2030, evidence of a flywheel that’s firmly in motion.

Talent isn’t India’s advantage anymore, it’s the engine of its global influence.

Between early 2024 and late 2025, ~110 new GCCs were established in India. The interesting part is not just the volume, it’s where they’re coming from. While US-headquartered firms still dominate the numbers, the last two years have seen a clear broadening of participation.

Companies from the UK, Germany, Japan, Denmark, and others have deepened their India presence, choosing the country not for cost, but for capability and speed.

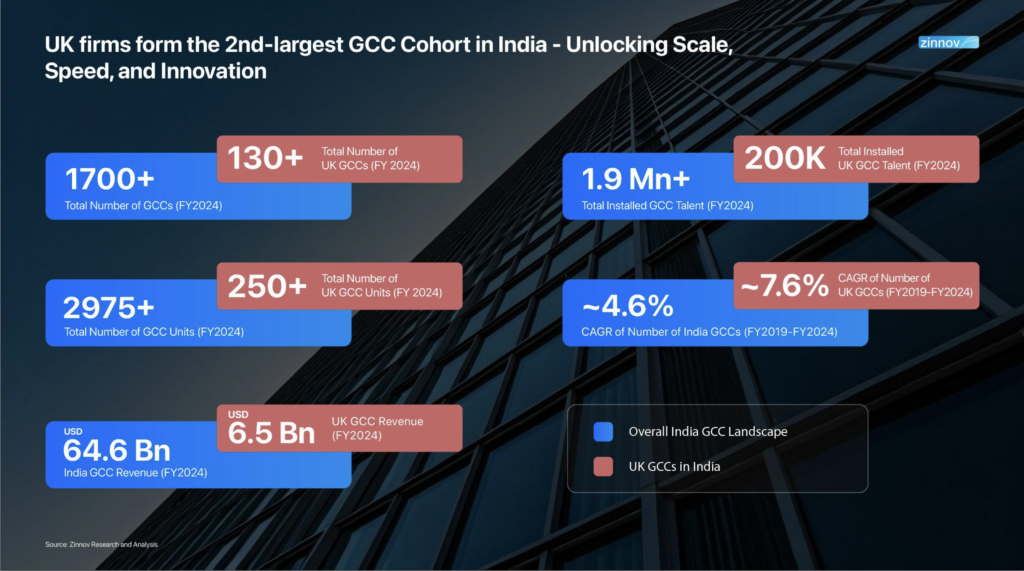

The UK–India corridor stands out as a model of maturity. According to Zinnov UK GCC Impact Report 2025, over 130 UK firms now operate 250+ GCCs across India, employing more than 200,000 professionals across digital, design, and AI. German enterprises followed a similar trajectory, setting up engineering-led centers that reflect their precision and product ethos.

By 2025, India had moved from being the GCC capital to becoming the global meeting ground for enterprise innovation.

According to Zinnov Tier-I City Analysis Report 2025, Bengaluru, with 880+ centers, remains the nucleus, home to one in three new GCCs added in FY24 and the country’s deepest ER&D and AI talent base. Hyderabad, with 355+ centers, has built strong momentum through government-backed initiatives like T-AIM (Telangana AI Mission) and a vibrant startup network of 940+ firms.

Mumbai and Pune complement each other with sectoral depth in BFSI and Automotive, while NCR and Chennai continue to diversify the mix, adding strength in Engineering, Healthcare, and Renewable Energy.

By 2025, these cities weren’t just clusters, they had evolved into a connected network of specialized ecosystems that together anchor India’s global capability story.

If one segment truly captured the momentum of the last two years, it’s the Mid-market cohort.

The Zinnov–nasscom Mid-market Global Capability Centers (GCCs) Report 2025 highlights that 480+ centers, employing over 210,000 professionals, now make up 27% of India’s GCC landscape.

And Karnataka sits at the heart of this wave. According to Zinnov-KDEM Karnataka Mid-market Report, nearly half of India’s Mid-market GCCs operate out of the state, supported by its forward-looking GCC policy and the Beyond Bengaluru initiative. The model, government as growth partner, is now being mirrored by Telangana, Maharashtra, and Tamil Nadu, all aligning their AI, Digital, and Semiconductor missions to similar intent.

By 2025, “mid-market” no longer meant mid-scale, it meant high-impact, powered by India’s most collaborative ecosystem yet.

At the other end of the spectrum are the Mega GCCs, centers with 5,000+ employees and parent companies earning over USD 1 billion annually. According to Zinnov Mega GCC Report 2025, they make up just 5% of India’s GCC count but employ nearly 50% of the total workforce.

Most of these centers have been in India for over two decades. They’ve matured from cost-driven operations into enterprise-critical transformation hubs. Nearly 9 in 10 now operate at the Portfolio or Transformation maturity stage, running global rollouts, compliance, and product mandates end-to-end.

Their workforce mix reflects that evolution, around 43% in ER&D, one-third in BPM, and leadership that’s increasingly global. Nearly two-thirds of Mega GCC heads today come from technical backgrounds, many managing dual mandates: running India operations while also leading global portfolios in Product, Engineering, or Cybersecurity.

With 88 Mega GCCs today and projections crossing 230 by 2030, this cohort represents scale meeting sophistication, the natural counterweight to the Mid-market wave that’s redefining speed.

By the end of 2025, India’s GCC network had crossed 1,760 centers. But the real story isn’t in the count, it’s in the confidence.

If 2024 made India the GCC Capital of the World, 2025 made it the “Global Catalyst of the Future.”

A Global Capability Center (GCC), commonly referred to as a Captive Center/Global In-house Center (GIC), is an offshore or nearshore entity fully owned and operated by a parent company. These centres typically operate a wide array of specialized services, ranging from Information Technology (IT) and Research and Development (R&D) to complex back-office functions. GCCs play a pivotal role in driving innovation, enhancing cost-efficiency, and accessing diverse talent pools.

India leads with over 1,760 Global Capability Centers (GCCs), driving innovation and strategic growth. India’s dominance in the GCC landscape is driven by its vast tech talent pool, cost efficiency, leadership arbitrage, robust digital infrastructure, and a business-friendly regulatory environment. GCCs in India also benefit from a mature ecosystem, and strong synergies with allied industries, including a thriving Start-up ecosystem and a dynamic Tech Services Sector. Cities like Bengaluru, Hyderabad, Mumbai, Pune and NCR have emerged as key innovation & transformation hubs, fostering a vibrant and collaborative environment for global Enterprises.

India’s Tier II cities—like Coimbatore, Ahmedabad, Jaipur, Indore, and Chandigarh—are fast becoming hotbeds for GCC expansion. These cities offer access to high-quality talent, lower real estate and operating costs, and rapidly improving infrastructure. By diversifying into these locations, companies can build resilient, distributed delivery models that reduce risk and enhance business continuity.

Adding momentum to this trend, state governments are proactively rolling out GCC-specific policies and incentives to attract global companies. For instance, Karnataka, Telangana, and Tamil Nadu have introduced targeted GCC policies offering plug-and-play infrastructure, tax incentives, streamlined approvals, and talent development partnerships with local universities. Gujarat and Andhra Pradesh are also stepping up with focused industry zones and single-window clearance systems to ease setup. These regional initiatives, coupled with central government support, are making Tier II cities not just viable but strategic for next-gen GCC growth.

Projections suggest that by 2030, a significant share of new GCCs will emerge from these high-potential, previously untapped cities, reshaping the geographic landscape of India’s global innovation economy.

Depending on the scale and complexity of the operation, it typically takes between 3 to 6 months to set up a fully functional GCC in India. With the help of a GCC consulting and setup expert and a robust setup playbook, companies can fast-track this process and achieve operational readiness in record time. Zinnov has successfully partnered with organizations like Agilon Health to establish their India GCC, helping them navigate talent strategy, legal and regulatory frameworks, infrastructure planning, and cultural integration. Leveraging such expertise not only reduces setup time but also ensures long-term scalability and strategic alignment with global business goals.

The Indian GCC ecosystem is set to grow into a $100+ billion market by 2030, reflecting its pivotal role in global enterprise transformation. With more than 1,700 GCCs already operational in Tier I cities like Hyderabad, Bangalore, Chennai, Mumbai, Pune, and NCR—and with newer cities like Coimbatore, Bhubaneswar, and Ahmedabad joining the fold—the ecosystem is rapidly expanding. By 2030, India is expected to house over 2,000–2,200 GCCs, marking a significant surge in both scale and strategic influence.